You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Parte I: Régimen general <strong><strong>de</strong>l</strong> <strong>Impuesto</strong> a <strong>la</strong> <strong>Renta</strong> <strong>de</strong> <strong>Empresas</strong><br />

Respuesta:<br />

Respecto a los gastos por <strong>de</strong>preciación, <strong>la</strong> LIR en el inciso f)<br />

<strong><strong>de</strong>l</strong> artículo 37° seña<strong>la</strong> que <strong>la</strong>s <strong>de</strong>preciaciones por <strong>de</strong>sgaste<br />

u obsolescencia <strong>de</strong> los bienes <strong>de</strong> activo fijo y <strong>la</strong>s mermas y<br />

<strong>de</strong>smedros <strong>de</strong> existencias <strong>de</strong>bidamente acreditados son<br />

<strong>de</strong>ducibles.<br />

Asimismo, el artículo 38° <strong>de</strong> <strong>la</strong> misma ley establece que el<br />

<strong>de</strong>sgaste o agotamiento que sufran los bienes <strong><strong>de</strong>l</strong> activo fijo que<br />

los contribuyentes utilicen en negocios, industria, profesión u otras<br />

activida<strong>de</strong>s productoras <strong>de</strong> rentas gravadas <strong>de</strong> tercera categoría, se<br />

compensará mediante <strong>la</strong> <strong>de</strong>ducción por <strong>la</strong>s <strong>de</strong>preciaciones admitidas<br />

en esta ley.<br />

Asimismo el artículo 22° <strong><strong>de</strong>l</strong> RLIR explica que para el cálculo <strong>de</strong> <strong>la</strong><br />

<strong>de</strong>preciación se aplicará <strong>la</strong>s siguientes disposiciones:<br />

a) De conformidad con el Artículo 39º <strong>de</strong> <strong>la</strong> LIR, los edificios y<br />

construcciones sólo serán <strong>de</strong>preciados mediante el método <strong>de</strong> línea<br />

recta, a razón <strong>de</strong> 3% anual.<br />

b) Los <strong>de</strong>más bienes afectados a <strong>la</strong> producción <strong>de</strong> rentas gravadas<br />

<strong>de</strong> <strong>la</strong> tercera categoría, se <strong>de</strong>preciarán aplicando el porcentaje que<br />

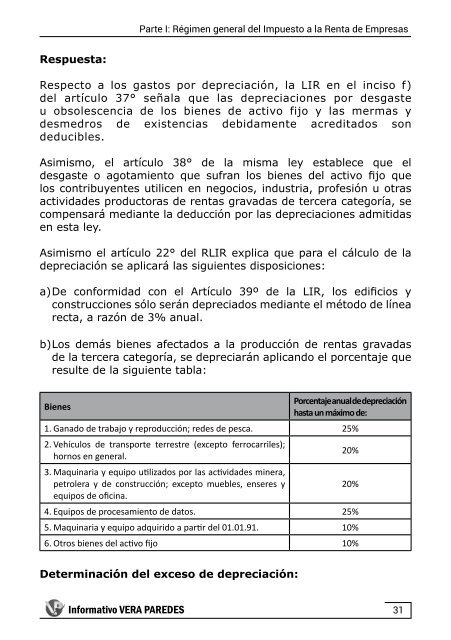

resulte <strong>de</strong> <strong>la</strong> siguiente tab<strong>la</strong>:<br />

Bienes<br />

Porcentaje anual <strong>de</strong> <strong>de</strong>preciación<br />

hasta un máximo <strong>de</strong>:<br />

1. Ganado <strong>de</strong> trabajo y reproducción; re<strong>de</strong>s <strong>de</strong> pesca. 25%<br />

2. Vehículos <strong>de</strong> transporte terrestre (excepto ferrocarriles);<br />

hornos en general.<br />

20%<br />

3. Maquinaria y equipo utilizados por <strong>la</strong>s activida<strong>de</strong>s minera,<br />

petrolera y <strong>de</strong> construcción; excepto muebles, enseres y<br />

20%<br />

equipos <strong>de</strong> oficina.<br />

4. Equipos <strong>de</strong> procesamiento <strong>de</strong> datos. 25%<br />

5. Maquinaria y equipo adquirido a partir <strong><strong>de</strong>l</strong> 01.01.91. 10%<br />

6. Otros bienes <strong><strong>de</strong>l</strong> activo fijo 10%<br />

Determinación <strong><strong>de</strong>l</strong> exceso <strong>de</strong> <strong>de</strong>preciación:<br />

Informativo VERA PAREDES<br />

31