You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Aplicación</strong> <strong>práctica</strong> <strong><strong>de</strong>l</strong> <strong>Impuesto</strong> a <strong>la</strong> <strong>Renta</strong> <strong>de</strong> <strong>Empresas</strong> <strong>2017</strong><br />

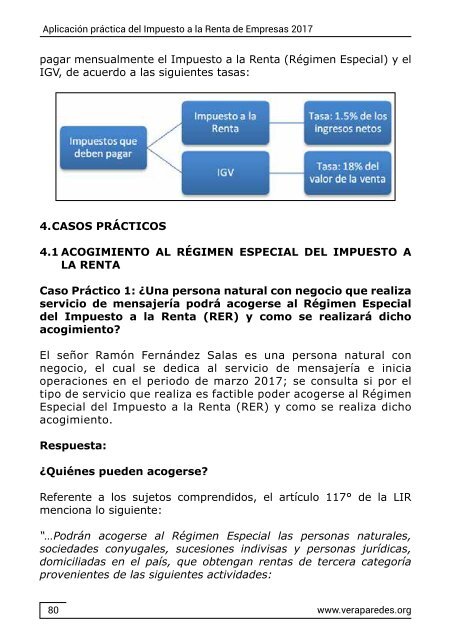

pagar mensualmente el <strong>Impuesto</strong> a <strong>la</strong> <strong>Renta</strong> (Régimen Especial) y el<br />

IGV, <strong>de</strong> acuerdo a <strong>la</strong>s siguientes tasas:<br />

4. CASOS PRÁCTICOS<br />

4.1 ACOGIMIENTO AL RÉGIMEN ESPECIAL DEL IMPUESTO A<br />

LA RENTA<br />

Caso Práctico 1: ¿Una persona natural con negocio que realiza<br />

servicio <strong>de</strong> mensajería podrá acogerse al Régimen Especial<br />

<strong><strong>de</strong>l</strong> <strong>Impuesto</strong> a <strong>la</strong> <strong>Renta</strong> (RER) y como se realizará dicho<br />

acogimiento?<br />

El señor Ramón Fernán<strong>de</strong>z Sa<strong>la</strong>s es una persona natural con<br />

negocio, el cual se <strong>de</strong>dica al servicio <strong>de</strong> mensajería e inicia<br />

operaciones en el periodo <strong>de</strong> marzo <strong>2017</strong>; se consulta si por el<br />

tipo <strong>de</strong> servicio que realiza es factible po<strong>de</strong>r acogerse al Régimen<br />

Especial <strong><strong>de</strong>l</strong> <strong>Impuesto</strong> a <strong>la</strong> <strong>Renta</strong> (RER) y como se realiza dicho<br />

acogimiento.<br />

Respuesta:<br />

¿Quiénes pue<strong>de</strong>n acogerse?<br />

Referente a los sujetos comprendidos, el artículo 117° <strong>de</strong> <strong>la</strong> LIR<br />

menciona lo siguiente:<br />

“…Podrán acogerse al Régimen Especial <strong>la</strong>s personas naturales,<br />

socieda<strong>de</strong>s conyugales, sucesiones indivisas y personas jurídicas,<br />

domiciliadas en el país, que obtengan rentas <strong>de</strong> tercera categoría<br />

provenientes <strong>de</strong> <strong>la</strong>s siguientes activida<strong>de</strong>s:<br />

80<br />

www.verapare<strong>de</strong>s.org