Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

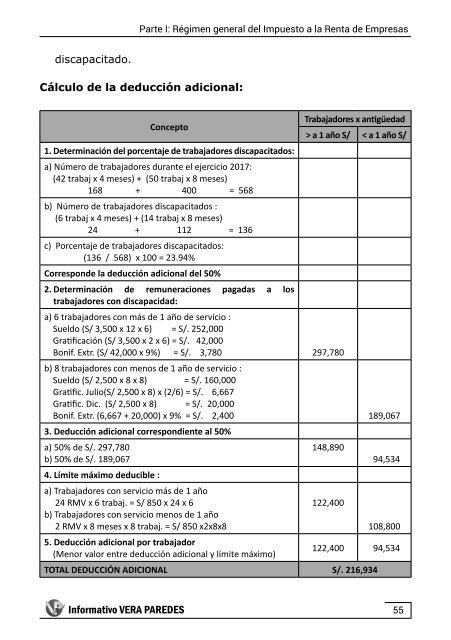

Parte I: Régimen general <strong><strong>de</strong>l</strong> <strong>Impuesto</strong> a <strong>la</strong> <strong>Renta</strong> <strong>de</strong> <strong>Empresas</strong><br />

discapacitado.<br />

Cálculo <strong>de</strong> <strong>la</strong> <strong>de</strong>ducción adicional:<br />

Concepto<br />

Trabajadores x antigüedad<br />

> a 1 año S/ < a 1 año S/<br />

1. Determinación <strong><strong>de</strong>l</strong> porcentaje <strong>de</strong> trabajadores discapacitados:<br />

a) Número <strong>de</strong> trabajadores durante el ejercicio <strong>2017</strong>:<br />

(42 trabaj x 4 meses) + (50 trabaj x 8 meses)<br />

168 + 400 = 568<br />

b) Número <strong>de</strong> trabajadores discapacitados :<br />

(6 trabaj x 4 meses) + (14 trabaj x 8 meses)<br />

24 + 112 = 136<br />

c) Porcentaje <strong>de</strong> trabajadores discapacitados:<br />

(136 / 568) x 100 = 23.94%<br />

Correspon<strong>de</strong> <strong>la</strong> <strong>de</strong>ducción adicional <strong><strong>de</strong>l</strong> 50%<br />

2. Determinación <strong>de</strong> remuneraciones pagadas a los<br />

trabajadores con discapacidad:<br />

a) 6 trabajadores con más <strong>de</strong> 1 año <strong>de</strong> servicio :<br />

Sueldo (S/ 3,500 x 12 x 6) = S/. 252,000<br />

Gratificación (S/ 3,500 x 2 x 6) = S/. 42,000<br />

Bonif. Extr. (S/ 42,000 x 9%) = S/. 3,780 297,780<br />

b) 8 trabajadores con menos <strong>de</strong> 1 año <strong>de</strong> servicio :<br />

Sueldo (S/ 2,500 x 8 x 8) = S/. 160,000<br />

Gratific. Julio(S/ 2,500 x 8) x (2/6) = S/. 6,667<br />

Gratific. Dic. (S/ 2,500 x 8) = S/. 20,000<br />

Bonif. Extr. (6,667 + 20,000) x 9% = S/. 2,400 189,067<br />

3. Deducción adicional correspondiente al 50%<br />

a) 50% <strong>de</strong> S/. 297,780<br />

148,890<br />

b) 50% <strong>de</strong> S/. 189,067<br />

94,534<br />

4. Límite máximo <strong>de</strong>ducible :<br />

a) Trabajadores con servicio más <strong>de</strong> 1 año<br />

24 RMV x 6 trabaj. = S/ 850 x 24 x 6<br />

122,400<br />

b) Trabajadores con servicio menos <strong>de</strong> 1 año<br />

2 RMV x 8 meses x 8 trabaj. = S/ 850 x2x8x8<br />

108,800<br />

5. Deducción adicional por trabajador<br />

(Menor valor entre <strong>de</strong>ducción adicional y límite máximo)<br />

122,400 94,534<br />

TOTAL DEDUCCIÓN ADICIONAL S/. 216,934<br />

Informativo VERA PAREDES<br />

55