Long Term Community Plan 2012-2022 - Hurunui District Council

Long Term Community Plan 2012-2022 - Hurunui District Council

Long Term Community Plan 2012-2022 - Hurunui District Council

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<strong>Hurunui</strong> <strong>Community</strong> <strong>Long</strong> <strong>Term</strong> <strong>Plan</strong> <strong>2012</strong> - <strong>2022</strong><br />

In general, Capital Expenditure is broken down to three key<br />

categories:<br />

1. Capital expenditure relating to meeting the existing<br />

levels of service. This will be principally replacement of<br />

the existing assets<br />

2. Capital expenditure aimed at improving the current<br />

levels of service<br />

3. Capital expenditure on assets required due to growth.<br />

Some items of Capital Expenditure may actually fall into more<br />

than one category. For example, the replacement of a length of<br />

water pipe is required to provide water to existing consumers,<br />

but the diameter of that length of pipe may be increased from<br />

its existing diameter to allow for greater capacity in the future.<br />

An assessment is carried out as to apportion the cost of each<br />

project to the category to which it relates and if that cannot<br />

be readily assessed, the category will be determine by the key<br />

reason for the work to be undertaken.<br />

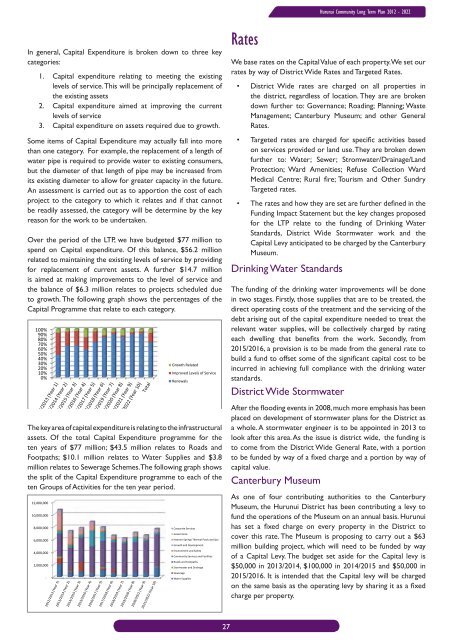

Over the period of the LTP, we have budgeted $77 million to<br />

spend on Capital expenditure. Of this balance, $56.2 million<br />

related to maintaining the existing levels of service by providing<br />

for replacement of current assets. A further $14.7 million<br />

is aimed at making improvements to the level of service and<br />

the balance of $6.3 million relates to projects scheduled due<br />

to growth. The following graph shows the percentages of the<br />

Capital Programme that relate to each category.<br />

100%<br />

90%<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

10%<br />

0%<br />

Growth Related<br />

Improved Levels of Service<br />

Renewals<br />

The key area of capital expenditure is relating to the infrastructural<br />

assets. Of the total Capital Expenditure programme for the<br />

ten years of $77 million; $43.5 million relates to Roads and<br />

Footpaths; $10.1 million relates to Water Supplies and $3.8<br />

million relates to Sewerage Schemes. The following graph shows<br />

the split of the Capital Expenditure programme to each of the<br />

ten Groups of Activities for the ten year period.<br />

12,000,000<br />

10,000,000<br />

8,000,000<br />

6,000,000<br />

4,000,000<br />

2,000,000<br />

-<br />

Corporate Services<br />

Governance<br />

Hanmer Springs Thermal Pools and Spa<br />

Growth and Development<br />

Environment and Safety<br />

<strong>Community</strong> Services and Facilities<br />

Roads and Footpaths<br />

Stormwater and Drainage<br />

Sewerage<br />

Water Supplies<br />

Rates<br />

We base rates on the Capital Value of each property. We set our<br />

rates by way of <strong>District</strong> Wide Rates and Targeted Rates.<br />

• <strong>District</strong> Wide rates are charged on all properties in<br />

the district, regardless of location. They are are broken<br />

down further to: Governance; Roading; <strong>Plan</strong>ning; Waste<br />

Management; Canterbury Museum; and other General<br />

Rates.<br />

• Targeted rates are charged for specific activities based<br />

on services provided or land use. They are broken down<br />

further to: Water; Sewer; Stromwater/Drainage/Land<br />

Protection; Ward Amenities; Refuse Collection Ward<br />

Medical Centre; Rural fire; Tourism and Other Sundry<br />

Targeted rates.<br />

• The rates and how they are set are further defined in the<br />

Funding Impact Statement but the key changes proposed<br />

for the LTP relate to the funding of Drinking Water<br />

Standards, <strong>District</strong> Wide Stormwater work and the<br />

Capital Levy anticipated to be charged by the Canterbury<br />

Museum.<br />

Drinking Water Standards<br />

The funding of the drinking water improvements will be done<br />

in two stages. Firstly, those supplies that are to be treated, the<br />

direct operating costs of the treatment and the servicing of the<br />

debt arising out of the capital expenditure needed to treat the<br />

relevant water supplies, will be collectively charged by rating<br />

each dwelling that benefits from the work. Secondly, from<br />

2015/2016, a provision is to be made from the general rate to<br />

build a fund to offset some of the significant capital cost to be<br />

incurred in achieving full compliance with the drinking water<br />

standards.<br />

<strong>District</strong> Wide Stormwater<br />

After the flooding events in 2008, much more emphasis has been<br />

placed on development of stormwater plans for the <strong>District</strong> as<br />

a whole. A stormwater engineer is to be appointed in 2013 to<br />

look after this area. As the issue is district wide, the funding is<br />

to come from the <strong>District</strong> Wide General Rate, with a portion<br />

to be funded by way of a fixed charge and a portion by way of<br />

capital value.<br />

Canterbury Museum<br />

As one of four contributing authorities to the Canterbury<br />

Museum, the <strong>Hurunui</strong> <strong>District</strong> has been contributing a levy to<br />

fund the operations of the Museum on an annual basis. <strong>Hurunui</strong><br />

has set a fixed charge on every property in the <strong>District</strong> to<br />

cover this rate. The Museum is proposing to carry out a $63<br />

million building project, which will need to be funded by way<br />

of a Capital Levy. The budget set aside for the Capital levy is<br />

$50,000 in 2013/2014, $100,000 in 2014/2015 and $50,000 in<br />

2015/2016. It is intended that the Capital levy will be charged<br />

on the same basis as the operating levy by sharing it as a fixed<br />

charge per property.<br />

27