coast guard morale, welfare, recreation manual - DOT On-Line ...

coast guard morale, welfare, recreation manual - DOT On-Line ...

coast guard morale, welfare, recreation manual - DOT On-Line ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

,/-- .<br />

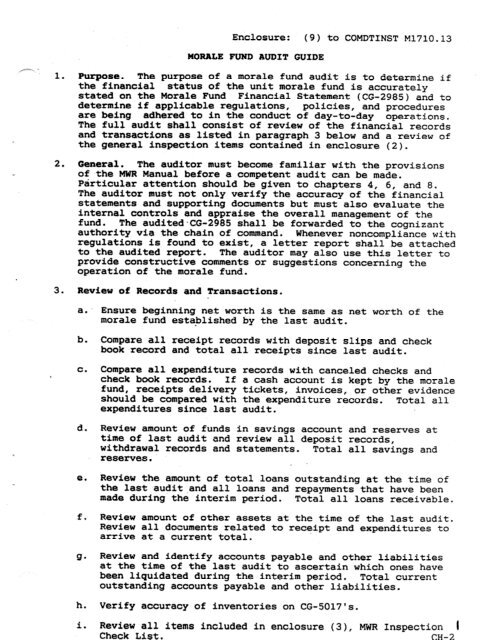

Enclosure: (9) to COMDTINST M1710.13<br />

MORALE FUND AUDIT GUIDE<br />

1. Purpose. The purpose of a <strong>morale</strong> fund audit is to determine if<br />

the financial status of the unit <strong>morale</strong> fund is accurately<br />

stated on the Morale Fund Financial Statement (CG-2985) and to<br />

determine if applicable regulations, policies, and procedures<br />

are being adhered to in the conduct of day-to-day operations.<br />

The full audit shall consist of review of the financial records<br />

and transactions as listed in paragraph 3 below and a review of<br />

the general inspection items contained in enclosure (2).<br />

2. General. The auditor must become familiar with the provisions<br />

of ,the MWR Manual before a competent audit can be made.<br />

Particular attention should be given to chapters 4, 6, and 8.<br />

The auditor must not only verify the accuracy of the financial<br />

statements and supporting documents but must also evaluate the<br />

internal controls and appraise the overall management of the<br />

fund. The audited.CG-2985 shall be forwarded to the cognizant<br />

authority via the chain of command, Whenever noncompliance with<br />

regulations is found to exist,<br />

a letter report shall be attached<br />

to the audited report. The auditor may also use this letter to<br />

provide constructive comments or suggestions concerning the<br />

operation of the <strong>morale</strong> fund.<br />

3. Review of Records and Transactions.<br />

a.<br />

b.<br />

c.<br />

d.<br />

e.<br />

f.<br />

h.<br />

i.<br />

Ensure beginning net worth is the same as net worth of the<br />

<strong>morale</strong> fund esta-blished by the last audit.<br />

Compare all receipt records with deposit slips and check<br />

book record and total all receipts since last audit.<br />

Compare all expenditure records with canceled checks and<br />

check book records. If a cash account is kept by the <strong>morale</strong><br />

fund, receipts delivery tickets, invoices, or other evidence<br />

should be compared with the expenditure records. Total all<br />

expenditures since last audit.<br />

Review amount of funds in savings account and reserves at<br />

time of last audit<br />

withdrawal records<br />

reserves.<br />

and review all deposit<br />

and statements. Total<br />

,<br />

records,<br />

all savings and<br />

Review the amount of total loans outstanding at the time of<br />

the last audit,and all loans and repayments that have been<br />

made during the interim period. Total all loans receivable.<br />

Review amount of other assets at the time of the last audit.<br />

Review all documents related to receipt and expenditures to<br />

arrive at a current total.<br />

Review and identify accounts payable and other liabilities<br />

at the time of the last audit to ascertain which ones have<br />

been liquidated during the interim period. Total current<br />

outstanding accounts payable and other liabilities.<br />

Verify accuracy of inventories on CG-5017's.<br />

Review all items included in enclosure (3), MWR Inspection 1<br />

Check List. CH-2