Namibia PDNA 2009 - GFDRR

Namibia PDNA 2009 - GFDRR

Namibia PDNA 2009 - GFDRR

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

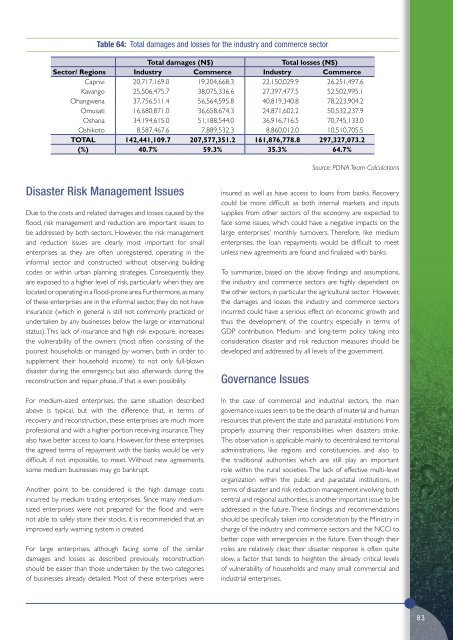

Table 64: Total damages and losses for the industry and commerce sector<br />

Total damages (N$)<br />

Total losses (N$)<br />

Sector/ Regions Industry Commerce Industry Commerce<br />

Caprivi 20,717,169.0 19,204,668.3 22,150,029.9 26,251,497.6<br />

Kavango 25,506,475.7 38,075,336.6 27,397,477.5 52,502,995.1<br />

Ohangwena 37,756,511.4 56,564,595.8 40,819,340.8 78,223,904.2<br />

Omusati 16,680,871.0 36,658,674.3 24,871,602.2 50,532,237.9<br />

Oshana 34,194,615.0 51,188,544.0 36,916,716.5 70,745,133.0<br />

Oshikoto 8,587,467.6 7,889,532.3 8,860,012.0 10,510,705.5<br />

TOTAL 142,441,109.7 207,577,351.2 161,876,778.8 297,327,073.2<br />

(%) 40.7% 59.3% 35.3% 64.7%<br />

Source: <strong>PDNA</strong> Team Calculations<br />

Disaster Risk Management Issues<br />

Due to the costs and related damages and losses caused by the<br />

flood, risk management and reduction are important issues to<br />

be addressed by both sectors. However, the risk management<br />

and reduction issues are clearly most important for small<br />

enterprises as they are often unregistered, operating in the<br />

informal sector and constructed without observing building<br />

codes or within urban planning strategies. Consequently, they<br />

are exposed to a higher level of risk, particularly when they are<br />

located or operating in a flood-prone area. Furthermore, as many<br />

of these enterprises are in the informal sector, they do not have<br />

insurance (which in general is still not commonly practiced or<br />

undertaken by any businesses below the large or international<br />

status). This lack of insurance and high risk exposure, increases<br />

the vulnerability of the owners (most often consisting of the<br />

poorest households or managed by women, both in order to<br />

supplement their household income) to not only full-blown<br />

disaster during the emergency, but also afterwards during the<br />

reconstruction and repair phase, if that is even possibility.<br />

For medium-sized enterprises, the same situation described<br />

above is typical, but with the difference that, in terms of<br />

recovery and reconstruction, these enterprises are much more<br />

professional and with a higher portion receiving insurance. They<br />

also have better access to loans. However, for these enterprises,<br />

the agreed terms of repayment with the banks would be very<br />

difficult, if not impossible, to meet. Without new agreements,<br />

some medium businesses may go bankrupt.<br />

Another point to be considered is the high damage costs<br />

incurred by medium trading enterprises. Since many mediumsized<br />

enterprises were not prepared for the flood and were<br />

not able to safely store their stocks, it is recommended that an<br />

improved early warning system is created.<br />

For large enterprises, although facing some of the similar<br />

damages and losses as described previously, reconstruction<br />

should be easier than those undertaken by the two categories<br />

of businesses already detailed. Most of these enterprises were<br />

insured as well as have access to loans from banks. Recovery<br />

could be more difficult as both internal markets and inputs<br />

supplies from other sectors of the economy are expected to<br />

face some issues, which could have a negative impacts on the<br />

large enterprises’ monthly turnovers. Therefore, like medium<br />

enterprises, the loan repayments would be difficult to meet<br />

unless new agreements are found and finalized with banks.<br />

To summarize, based on the above findings and assumptions,<br />

the industry and commerce sectors are highly dependent on<br />

the other sectors, in particular the agricultural sector. However,<br />

the damages and losses the industry and commerce sectors<br />

incurred could have a serious effect on economic growth and<br />

thus the development of the country, especially in terms of<br />

GDP contribution. Medium- and long-term policy taking into<br />

consideration disaster and risk reduction measures should be<br />

developed and addressed by all levels of the government.<br />

Governance Issues<br />

In the case of commercial and industrial sectors, the main<br />

governance issues seem to be the dearth of material and human<br />

resources that prevent the state and parastatal institutions from<br />

properly assuming their responsibilities when disasters strike.<br />

This observation is applicable mainly to decentralized territorial<br />

administrations, like regions and constituencies, and also to<br />

the traditional authorities which are still play an important<br />

role within the rural societies. The lack of effective multi-level<br />

organization within the public and parastatal institutions, in<br />

terms of disaster and risk reduction management involving both<br />

central and regional authorities, is another important issue to be<br />

addressed in the future. These findings and recommendations<br />

should be specifically taken into consideration by the Ministry in<br />

charge of the industry and commerce sectors and the NCCI to<br />

better cope with emergencies in the future. Even though their<br />

roles are relatively clear, their disaster response is often quite<br />

slow, a factor that tends to heighten the already critical levels<br />

of vulnerability of households and many small commercial and<br />

industrial enterprises.<br />

83