Market Economics | Interest Rate Strategy - BNP PARIBAS ...

Market Economics | Interest Rate Strategy - BNP PARIBAS ...

Market Economics | Interest Rate Strategy - BNP PARIBAS ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

US: TSY Switches for Yield/Duration Pick-Up<br />

• Many are envisioning a range-trading<br />

summer, setting the market up for a yield-grab<br />

as investors look to extend duration. We focus<br />

on specific switches that have cheapened<br />

recently.<br />

• A Z-score approach to ASWs helps identify<br />

RV opportunities between neighbouring Tsy<br />

issues in various sectors of the curve.<br />

• STRATEGY: Look to switch between<br />

relatively rich and cheap issues (or consider<br />

RV spread trades) as per the recommendations<br />

below.<br />

`<br />

We first examine 30, 60, and 90 day asset swap<br />

spread Z-scores, which represent the number of<br />

standard deviations from the mean. Rather than<br />

drawing broad conclusions about a particular sector’s<br />

rich/cheapness, we look for relative rich/cheapness<br />

between neighbouring issues. We also keep in mind<br />

that the goal is to generally extend duration and seek<br />

yield pick-up (although this isn’t always the case),<br />

while also limiting the directional/curve exposure.<br />

The resulting trades are spread across the maturity<br />

spectrum, as shown in Table 1. None of the issues<br />

listed in the Table appear to be trading special in<br />

repo, which would have partially explained their<br />

richness.<br />

4.375% Aug-12s vs 4.125% Aug-12s (Chart 1)<br />

This is a switch from an old 10yr to an old 5yr note,<br />

and with 15 days of curve. We estimate the fair value<br />

of the curve to be around 1.5bp in this sector, making<br />

the yield pick-up of 4.5bp look compelling (the Z-<br />

score methodology suggests this is 2.8bp too high).<br />

Chart 1 shows that the spread is also near the top<br />

end of its range.<br />

2.5% Mar-13s vs 1.75% Apr-13s (Chart 2)<br />

This is a switch from an old 5yr to an old 3yr note,<br />

and with 15 days of curve. Again we estimate the fair<br />

value of the curve to be around 1.5bp in this sector,<br />

and the yield pick-up of around 10bp is the highest<br />

amongst the various switches we show (although in<br />

this case there is no duration pick-up). Chart 2 shows<br />

that the spread is also near the top end of its range.<br />

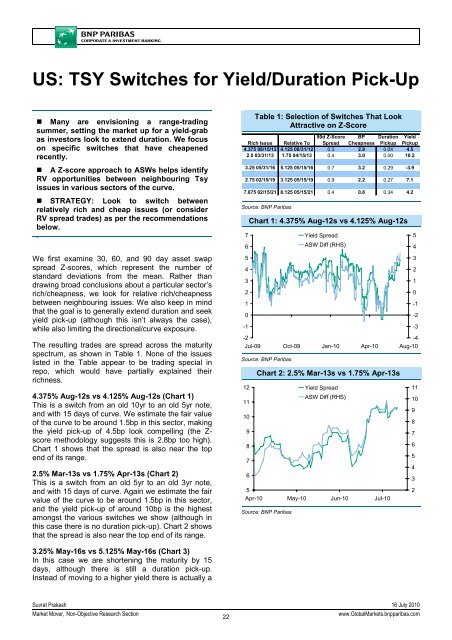

Table 1: Selection of Switches That Look<br />

Attractive on Z-Score<br />

Rich Issue Relative To<br />

90d Z-Score<br />

Spread<br />

BP<br />

Cheapness<br />

Duration<br />

Pickup<br />

Yield<br />

Pickup<br />

4.375 08/15/12 4.125 08/31/12 0.3 2.8 0.04 4.5<br />

2.5 03/31/13 1.75 04/15/13 0.4 3.0 0.00 10.2<br />

3.25 05/31/16 5.125 05/15/16 0.7 3.2 0.29 -3.9<br />

2.75 02/15/19 3.125 05/15/19 0.9 2.2 0.27 7.1<br />

7.875 02/15/21 8.125 05/15/21 0.4 0.8 0.34 4.2<br />

Source: <strong>BNP</strong> Paribas<br />

7<br />

6<br />

5<br />

4<br />

3<br />

2<br />

1<br />

0<br />

-1<br />

Chart 1: 4.375% Aug-12s vs 4.125% Aug-12s<br />

-2<br />

-4<br />

Jul-09 Oct-09 Jan-10 Apr-10 Aug-10<br />

Source: <strong>BNP</strong> Paribas<br />

12<br />

11<br />

10<br />

9<br />

8<br />

7<br />

6<br />

Yield Spread<br />

Chart 2: 2.5% Mar-13s vs 1.75% Apr-13s<br />

5<br />

Apr-10 May-10 Jun-10 Jul-10<br />

Source: <strong>BNP</strong> Paribas<br />

ASW Diff (RHS)<br />

Yield Spread<br />

ASW Diff (RHS)<br />

5<br />

4<br />

3<br />

2<br />

1<br />

0<br />

-1<br />

-2<br />

-3<br />

11<br />

10<br />

9<br />

8<br />

7<br />

6<br />

5<br />

4<br />

3<br />

2<br />

3.25% May-16s vs 5.125% May-16s (Chart 3)<br />

In this case we are shortening the maturity by 15<br />

days, although there is still a duration pick-up.<br />

Instead of moving to a higher yield there is actually a<br />

Suvrat Prakash 16 July 2010<br />

<strong>Market</strong> Mover, Non-Objective Research Section<br />

22<br />

www.Global<strong>Market</strong>s.bnpparibas.com