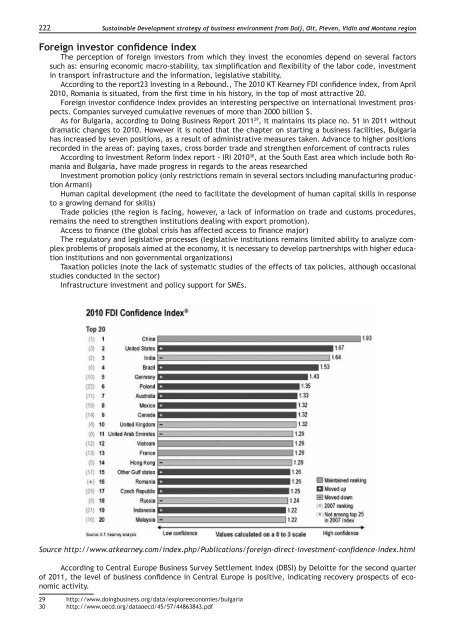

222Sustainable Development strategy of business envi<strong>ro</strong>nment f<strong>ro</strong>m Dolj, Olt, Pleven, Vidin and Montana regionForeign investor confi<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>nce in<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>xThe perception of foreign investors f<strong>ro</strong>m which they invest the economies <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>pend on several factorssuch as: ensuring economic mac<strong>ro</strong>-stability, tax simplification and flexibility of the labor co<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>, investmentin transport infrastructure and the information, legislative stability.According to the report23 Investing in a Rebound., The 2010 KT Kearney FDI confi<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>nce in<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>x, f<strong>ro</strong>m April2010, Romania is situated, f<strong>ro</strong>m the first time in his history, in the top of most attractive 20.Foreign investor confi<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>nce in<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>x p<strong>ro</strong>vi<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>s an interesting perspective on international investment p<strong>ro</strong>spects.Companies surveyed cumulative revenues of more than 2000 billion $.As for Bulgaria, according to Doing Business Report 2011 29 , it maintains its place no. 51 in 2011 withoutdramatic changes to 2010. However it is noted that the chapter on starting a business facilities, Bulgariahas increased by seven positions, as a result of administrative measures taken. Advance to higher positionsrecor<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>d in the areas of: paying taxes, c<strong>ro</strong>ss bor<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>r tra<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng> and strengthen enforcement of contracts rulesAccording to Investment Reform In<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>x report - IRI 2010 30 , at the South East area which inclu<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng> both Romaniaand Bulgaria, have ma<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng> p<strong>ro</strong>gress in regards to the areas researchedInvestment p<strong>ro</strong>motion policy (only restrictions remain in several sectors including manufacturing p<strong>ro</strong>ductionArmani)Human capital <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>velopment (the need to facilitate the <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>velopment of human capital skills in responseto a g<strong>ro</strong>wing <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>mand for skills)Tra<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng> policies (the region is facing, however, a lack of information on tra<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng> and customs p<strong>ro</strong>cedures,remains the need to strengthen institutions <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>aling with export p<strong>ro</strong>motion).Access to finance (the global crisis has affected access to finance major)The regulatory and legislative p<strong>ro</strong>cesses (legislative institutions remains limited ability to analyze complexp<strong>ro</strong>blems of p<strong>ro</strong>posals aimed at the economy, it is necessary to <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>velop partnerships with higher educationinstitutions and non governmental organizations)Taxation policies (note the lack of systematic studies of the effects of tax policies, although occasionalstudies conducted in the sector)Infrastructure investment and policy support for SMEs.Source http://www.atkearney.com/in<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>x.php/Publications/foreign-direct-investment-confi<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>nce-in<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>x.htmlAccording to Central Eu<strong>ro</strong>pe Business Survey Settlement In<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>x (DBSI) by Deloitte for the second quarte<strong>ro</strong>f 2011, the level of business confi<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>nce in Central Eu<strong>ro</strong>pe is positive, indicating recovery p<strong>ro</strong>spects of economicactivity.29 http://www.doingbusiness.org/data/exploreeconomies/bulgaria30 http://www.oecd.org/dataoecd/45/57/44863843.pdf

Sustainable Development strategy of business envi<strong>ro</strong>nment f<strong>ro</strong>m Dolj, Olt, Pleven, Vidin and Montana region 223Regarding Romania, we note the following relevant aspects:• survey results compared to f<strong>ro</strong>m the 3rd quarter of 2010, business people in lea<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>rship positions continueto consi<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>r imp<strong>ro</strong>vements in the business. Precierile negative in this regard have fallen by 20%compared to 2010;• Romanian executives shown pessimistic about the financial p<strong>ro</strong>spects of the companies they run. Positiveresponses <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>creased f<strong>ro</strong>m 63% in October 2010 to 48% in June 2011;• Romanian businessmen are still optimistic about safety limits payments to employees, the number ofpositive responses increased by 14% compared to 2010.• Number of businessmen surveyed expected to increase sales revenue over the next 12 months <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>creasedby 3% f<strong>ro</strong>m Q3 of yer 2010, and are more optimistic about the launch of new p<strong>ro</strong>ducts and / orservices.Since the end of 2010, was adopted national strategy for imp<strong>ro</strong>ving government and business <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>velopment,p<strong>ro</strong>ject implemented by the Ministry of Economy, Tra<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng> and Business Envi<strong>ro</strong>nment (METBE) 31 .Strategy aims and measures for 2010-2014 focuses on three main pillars:1. encouraging p<strong>ro</strong>ductive investment (foreign and Romanian);2. support and stimulate private initiative;3. support p<strong>ro</strong>fessions.The strategy was <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>veloped within a larger p<strong>ro</strong>ject that has p<strong>ro</strong>posed the implementation of activitiesto imp<strong>ro</strong>ve the business envi<strong>ro</strong>nment in Romania and imp<strong>ro</strong>ving the capacity of the Ministry of Economy, Tra<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>and Business of strategic planning, analysis, evaluation and monitoring.Analysis of regional economic concentration and specializationAnalysis of the types of specialties and types of economy reveals the competitive advantages it may have atone time. Type of p<strong>ro</strong>ducts that specialize in one region may <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>termine its economic competitiveness <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>gree.Technology-intensive p<strong>ro</strong>ducts (high-tech) have a bigger <strong>ro</strong>le in world tra<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng> due to the benefits theyoffer: obtain temporary monopoly advantages (arising f<strong>ro</strong>m barriers to entry of these p<strong>ro</strong>ducts competition),generating a p<strong>ro</strong>cess of accumulation of specialization, technology-intensive sectors more attractive for multinationalcompanies, <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>mand for these p<strong>ro</strong>ducts.At Eu<strong>ro</strong>pean level, new entrants in the EU states are usually a specialization in p<strong>ro</strong>ducts with a low technologicallevel, intensive in natural resource and workforce 32 .According to the study I<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>ntifying clusters emerging in Romania conducted by Applied Economics G<strong>ro</strong>up,to the 2006 level had been i<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>ntified emerging regional clusters. Thus, for the Central Region were i<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>ntifiedpotential areas of specialization in woodworking, construction and steel metal p<strong>ro</strong>ducts. North Eastern Regionwith the potential for specialization was the fabric. In the western region emerging clusters and softwareaimed at textile sectors, and in the North West and Bucharest - Ilfov the potential creation of clusters was the<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>dicated software.For the South East, South Muntenia and South West Oltenia was not i<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>ntified any potential cluster atthe time of research - year 2006.In the framework of p<strong>ro</strong>moting Romanian-Bulgarian C<strong>ro</strong>ss-bor<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>r Network of Multipliers for envi<strong>ro</strong>nmentalinformation was i<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>ntified lack of compact <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>velopment strategies of the industry (cluster) in the c<strong>ro</strong>ssbor<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>r area as a serious impediment to the visibility of local economies.Clusters are geographic concentrations of interconnected companies, specialized suppliers, service p<strong>ro</strong>vi<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>rs,firms in related industries and associated institutions (eg universities, research entities, <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>velopmentand innovation, standardization bodies, p<strong>ro</strong>fessional associations, chambers of commerce etc.), f<strong>ro</strong>m a particularfield, who work and remaining in the competition.Competitiveness poles are geographic concentrations of public and private companies, research centersand educational institutions, working in partnership un<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>r a common <st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>velopment strategy in or<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>r to generatesinergiişi cooperation in innovative p<strong>ro</strong>jects in the interests of one or more markets.Advantages of cluster:• Imp<strong>ro</strong>ving the competitiveness of companies to meet new economic challenges;• P<strong>ro</strong>ductivităţiişi g<strong>ro</strong>wth rate of labor employment in the region, by linking people, skills, competenciesand knowledge;• Increase economic efficiency (it is easy to work in a network with customers and suppliers);• Stimulating innovation: customer interaction creates new i<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>as and great pressure on innovation;• Reduce constraint for SMEs f<strong>ro</strong>m large companies;• Increase chances of success for “start-ups” and “spin-off”;31 http://www.wall-street.<strong>ro</strong>/articol/Economie/79467/Strategia-pentru-<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>zvoltarea-<st<strong>ro</strong>ng>mediului</st<strong>ro</strong>ng>-<st<strong>ro</strong>ng>de</st<strong>ro</strong>ng>-<st<strong>ro</strong>ng>afaceri</st<strong>ro</strong>ng>-costa-3-mil-lei.html32 Technological specialization of p<strong>ro</strong>duction and exports in Eu<strong>ro</strong>pe in terms of real convergence, 2008