Climate change

Mercado_Nov2015

Mercado_Nov2015

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

PARAGUAY<br />

tividades estratégicas del<br />

sector seguros. En efecto,<br />

los cinco productos principales<br />

del mercado asegurador<br />

de Paraguay están constituidos<br />

por los seguros de Automóviles,<br />

Vida Colectivo, Incendios,<br />

Riesgos Varios y<br />

Agropecuarios. Juntos conforman<br />

el 78% del total de la<br />

cartera del mercado local en<br />

ese período. Al respecto, cabe<br />

destacar que la diversificación<br />

relativa ha mejorado<br />

respecto al período<br />

2003/2008, en que los cinco<br />

principales productos acumulaban<br />

el 94% del portafolio<br />

del mercado (Ver Gráfico<br />

2).<br />

Evolución Primas de<br />

Reaseguros<br />

Se aprecia una evolución de<br />

las primas cedidas al reaseguro<br />

en el período 2007/2014, notándose<br />

una aceleración de crecimiento<br />

en el período de<br />

análisis con una tasa anual<br />

acumulativa del 32%; con<br />

una trayectoria con bastante<br />

regularidad hasta el año 2010<br />

y adquiriendo, luego, una mayor<br />

dinámica de expansión.<br />

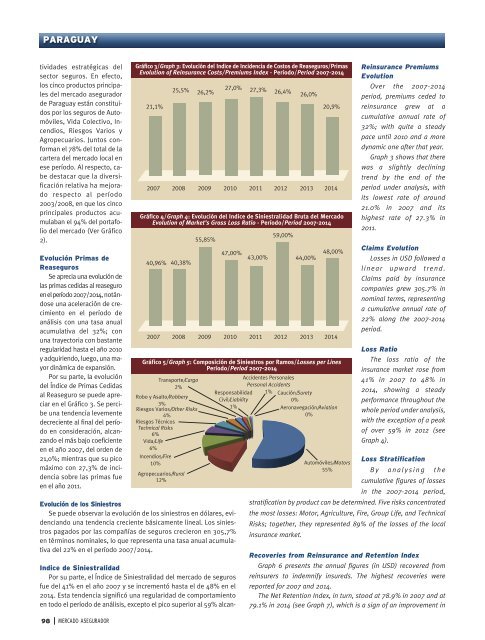

Por su parte, la evolución<br />

del Índice de Primas Cedidas<br />

al Reaseguro se puede apreciar<br />

en el Gráfico 3. Se percibe<br />

una tendencia levemente<br />

decreciente al final del período<br />

en consideración, alcanzando<br />

el más bajo coeficiente<br />

en el año 2007, del orden de<br />

21,0%; mientras que su pico<br />

máximo con 27,3% de incidencia<br />

sobre las primas fue<br />

en el año 2011.<br />

Gráfico 3/Graph 3: Evolución del Indice de Incidencia de Costos de Reaseguros/Primas<br />

Evolution of Reinsurance Costs/Premiums Index - Período/Period 2007-2014<br />

21,1%<br />

Evolución de los Siniestros<br />

Se puede observar la evolución de los siniestros en dólares, evidenciando<br />

una tendencia creciente básicamente lineal. Los siniestros<br />

pagados por las compañías de seguros crecieron en 305,7%<br />

en términos nominales, lo que representa una tasa anual acumulativa<br />

del 22% en el período 2007/2014.<br />

Indice de Siniestralidad<br />

Por su parte, el Índice de Siniestralidad del mercado de seguros<br />

fue del 41% en el año 2007 y se incrementó hasta el de 48% en el<br />

2014. Esta tendencia significó una regularidad de comportamiento<br />

en todo el período de análisis, excepto el pico superior al 59% alcan-<br />

Gráfico 4/Graph 4: Evolución del Indice de Siniestralidad Bruta del Mercado<br />

Evolution of Market’s Gross Loss Ratio - Período/Period 2007-2014<br />

40,96% 40,38%<br />

55,85%<br />

47,00% 43,00%<br />

59,00%<br />

44,00%<br />

48,00%<br />

2007 2008 2009 2010 2011 2012 2013 2014<br />

Gráfico 5/Graph 5: Composición de Siniestros por Ramos/Losses per Lines<br />

Período/Period 2007-2014<br />

Transporte/Cargo<br />

2%<br />

Robo y Asalto/Robbery<br />

3%<br />

Riesgos Varios/Other Risks<br />

4%<br />

Riesgos Técnicos<br />

Technical Risks<br />

6%<br />

Vida/Life<br />

6%<br />

Incendios/Fire<br />

10%<br />

Agropecuarios/Rural<br />

12%<br />

25,5% 26,2%<br />

27,0% 27,3% 26,4% 26,0%<br />

20,9%<br />

2007 2008 2009 2010 2011 2012 2013 2014<br />

Responsabilidad<br />

Civil/Liability<br />

1%<br />

Accidentes Personales<br />

Personal Accidents<br />

1%<br />

Caución/Surety<br />

0%<br />

Aeronavegación/Aviation<br />

0%<br />

Reinsurance Premiums<br />

Evolution<br />

Over the 2007-2014<br />

period, premiums ceded to<br />

reinsurance grew at a<br />

cumulative annual rate of<br />

32%; with quite a steady<br />

pace until 2010 and a more<br />

dynamic one after that year.<br />

Graph 3 shows that there<br />

was a slightly declining<br />

trend by the end of the<br />

period under analysis, with<br />

its lowest rate of around<br />

21.0% in 2007 and its<br />

highest rate of 27.3% in<br />

2011.<br />

Claims Evolution<br />

Losses in USD followed a<br />

l i n e a r u p w a r d t r e n d .<br />

Claims paid by insurance<br />

companies grew 305.7% in<br />

nominal terms, representing<br />

a cumulative annual rate of<br />

22% along the 2007-2014<br />

period.<br />

Loss Ratio<br />

The loss ratio of the<br />

insurance market rose from<br />

41% in 2007 to 48% in<br />

2014, showing a steady<br />

performance throughout the<br />

whole period under analysis,<br />

with the exception of a peak<br />

of over 59% in 2012 (see<br />

Graph 4).<br />

Loss Stratification<br />

Automóviles/Motors<br />

55%<br />

B y a n a l y s i n g t h e<br />

cumulative figures of losses<br />

in the 2007-2014 period,<br />

stratification by product can be determined. Five risks concentrated<br />

the most losses: Motor, Agriculture, Fire, Group Life, and Technical<br />

Risks; together, they represented 89% of the losses of the local<br />

insurance market.<br />

Recoveries from Reinsurance and Retention Index<br />

Graph 6 presents the annual figures (in USD) recovered from<br />

reinsurers to indemnify insureds. The highest recoveries were<br />

reported for 2007 and 2014.<br />

The Net Retention Index, in turn, stood at 78.9% in 2007 and at<br />

79.1% in 2014 (see Graph 7), which is a sign of an improvement in<br />

98<br />

MERCADO ASEGURADOR