Climate change

Mercado_Nov2015

Mercado_Nov2015

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

LATINOAMERICA - LATIN AMERICA<br />

ca de la actividad de M&A.<br />

En este segmento, las M&A<br />

cayeron después del deterioro<br />

financiero en Europa y en Estados<br />

Unidos. Sin embargo, la<br />

crisis indujo una necesidad por<br />

mejorar los balances y desencadenó<br />

algunas desinversiones<br />

estratégicas, lo que cambió<br />

la razón de ser de las transacciones.<br />

Por ejemplo, en Japón,<br />

las empresas decidieron<br />

ampliar su presencia en otros<br />

mercados de la región debido<br />

a las bajas perspectivas de crecimiento que se perfilaban domésticamente.<br />

Los mercados emergentes por otra parte, específicamente los<br />

latinoamericanos, se han visto sujetos a cambios en materia de regulación<br />

2 , lo que ha fomentado la concentración en la industria. La adaptación<br />

de nuevos esquemas de capital basado en riesgo conlleva nuevos<br />

requerimientos cuantitativos que exponen a aquellas empresas que no<br />

disponen de la capacidad de diversificar operaciones o lograr economías<br />

de escala. Esto, sumado a los altos crecimientos potenciales, ha servido<br />

para atraer compradores de mercados avanzados.<br />

Brasil y Chile son los dos países latinoamericanos que han visto<br />

mayor actividad en este sentido. La tendencia ha sido marcada por<br />

compradores extranjeros que intentan aprovechar el crecimiento de<br />

la clase media de Latinoamérica y las oportunidades para el sector<br />

privado en materia de jubilación en países como Chile. En el período<br />

2001-2007, el valor de las operaciones de M&A en el sector Vida de<br />

Latinoamérica y el Caribe representaban 2,4% del total global, mientras<br />

que en 2008-2014 crecieron a 6,8% (ver Figura 2).<br />

El Desafío de las Sinergias<br />

Desde el punto de vista de un accionista, una adquisición es exitosa<br />

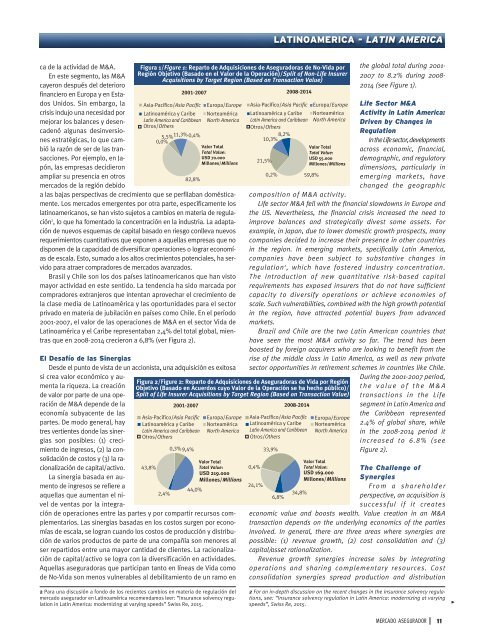

Figura 1/Figure 1: Reparto de Adquisiciones de Aseguradoras de No-Vida por<br />

Región Objetivo (Basado en el Valor de la Operación)/Split of Non-Life Insurer<br />

Acquisitions by Target Region (Based on Transaction Value)<br />

2001-2007<br />

Asia-Pacífico/Asia Pacific<br />

Latinoamérica y Caribe<br />

Latin America and Caribbean<br />

Otros/Others<br />

5,5% 11,3% 0,4%<br />

0,0%<br />

43,8%<br />

2,4%<br />

82,8%<br />

2001-2007<br />

Asia-Pacífico/Asia Pacific<br />

Latinoamérica y Caribe<br />

Latin America and Caribbean<br />

Otros/Others<br />

0,3% 9,4%<br />

Europa/Europe<br />

Norteamérica<br />

North America<br />

Valor Total<br />

Total Value:<br />

USD 70.000<br />

Millones/Millions<br />

Europa/Europe<br />

Norteamérica<br />

North America<br />

si crea valor económico y aumenta<br />

la riqueza. La creación<br />

de valor por parte de una operación<br />

de M&A depende de la<br />

economía subyacente de las<br />

partes. De modo general, hay<br />

tres vertientes donde las sinergias<br />

son posibles: (1) crecimiento<br />

de ingresos, (2) la consolidación<br />

de costos y (3) la racionalización<br />

de capital/activo.<br />

La sinergia basada en aumento<br />

de ingresos se refiere a<br />

aquellas que aumentan el nivel<br />

de ventas por la integración<br />

de operaciones entre las partes y por compartir recursos complementarios.<br />

Las sinergias basadas en los costos surgen por economías<br />

de escala, se logran cuando los costos de producción y distribución<br />

de varios productos de parte de una compañía son menores al<br />

ser repartidos entre una mayor cantidad de clientes. La racionalización<br />

de capital/activo se logra con la diversificación en actividades.<br />

Aquellas aseguradoras que participan tanto en líneas de Vida como<br />

de No-Vida son menos vulnerables al debilitamiento de un ramo en<br />

2008-2014<br />

Asia-Pacífico/Asia Pacific<br />

Latinoamérica y Caribe<br />

Latin America and Caribbean<br />

Otros/Others<br />

Europa/Europe<br />

Norteamérica<br />

North America<br />

10,3% 8,2% Valor Total<br />

Total Value:<br />

USD 55.000<br />

21,5%<br />

Millones/Millions<br />

0,2%<br />

59,8%<br />

the global total during 2001-<br />

2007 to 8.2% during 2008-<br />

2014 (see Figure 1).<br />

Life Sector M&A<br />

Activity in Latin America:<br />

Driven by Changes in<br />

Regulation<br />

In the Life sector, developments<br />

across economic, financial,<br />

demographic, and regulatory<br />

dimensions, particularly in<br />

emerging markets, have<br />

<strong>change</strong>d the geographic<br />

composition of M&A activity.<br />

Life sector M&A fell with the financial slowdowns in Europe and<br />

the US. Nevertheless, the financial crisis increased the need to<br />

improve balances and strategically divest some assets. For<br />

example, in Japan, due to lower domestic growth prospects, many<br />

companies decided to increase their presence in other countries<br />

in the region. In emerging markets, specifically Latin America,<br />

companies have been subject to substantive <strong>change</strong>s in<br />

regulation 2 , which have fostered industry concentration.<br />

The introduction of new quantitative risk-based capital<br />

requirements has exposed insurers that do not have sufficient<br />

capacity to diversify operations or achieve economies of<br />

scale. Such vulnerabilities, combined with the high growth potential<br />

in the region, have attracted potential buyers from advanced<br />

markets.<br />

Brazil and Chile are the two Latin American countries that<br />

have seen the most M&A activity so far. The trend has been<br />

boosted by foreign acquirers who are looking to benefit from the<br />

rise of the middle class in Latin America, as well as new private<br />

sector opportunities in retirement schemes in countries like Chile.<br />

Figura 2/Figure 2: Reparto de Adquisiciones de Aseguradoras de Vida por Región<br />

Objetivo (Basado en Acuerdos cuyo Valor de la Operación se ha hecho público)/<br />

Split of Life Insurer Acquisitions by Target Region (Based on Transaction Value)<br />

Valor Total<br />

Total Value:<br />

0,4%<br />

USD 219.000<br />

Millones/Millions<br />

24,1%<br />

44,0%<br />

33,9%<br />

6,8%<br />

2008-2014<br />

Asia-Pacífico/Asia Pacific<br />

Latinoamérica y Caribe<br />

Latin America and Caribbean<br />

Otros/Others<br />

34,8%<br />

Europa/Europe<br />

Norteamérica<br />

North America<br />

Valor Total<br />

Total Value:<br />

USD 169.000<br />

Millones/Millions<br />

During the 2001-2007 period,<br />

t h e v a l u e o f t h e M & A<br />

transactions in the Life<br />

segment in Latin America and<br />

the Caribbean represented<br />

2.4% of global share, while<br />

in the 2008-2014 period it<br />

increased to 6.8% (see<br />

Figure 2).<br />

The Challenge of<br />

Synergies<br />

F r o m a s h a r e h o l d e r<br />

perspective, an acquisition is<br />

successful if it creates<br />

economic value and boosts wealth. Value creation in an M&A<br />

transaction depends on the underlying economics of the parties<br />

involved. In general, there are three areas where synergies are<br />

possible: (1) revenue growth, (2) cost consolidation and (3)<br />

capital/asset rationalization.<br />

Revenue growth synergies increase sales by integrating<br />

operations and sharing complementary resources. Cost<br />

consolidation synergies spread production and distribution<br />

2 Para una discusión a fondo de los recientes cambios en materia de regulación del<br />

mercado asegurador en Latinoamérica recomendamos leer: “Insurance solvency regulation<br />

in Latin America: modernizing at varying speeds” Swiss Re, 2015.<br />

2 For an in-depth discussion on the recent <strong>change</strong>s in the insurance solvency regulations,<br />

see: “Insurance solvency regulation in Latin America: modernizing at varying<br />

speeds”, Swiss Re, 2015. ><br />

MERCADO ASEGURADOR<br />

11