Climate change

Mercado_Nov2015

Mercado_Nov2015

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

URUGUAY<br />

Tabla/Table 2: Evolución de los Ramos en USD - Valores Corrientes de 2008 a 2014/Developement of Lines in USD - Current Values 2008-2014<br />

Ramos/Lines 2008 2009 2010 2011 2012 2013 2014 %^2013<br />

Incendio/Fire 22.648.770 29.816.669 27.866.897 35.718.397 48.307.350 49.784.728 53.732.082 7,9%<br />

Vehículos/Motors 131.522.114 205.011.597 235.282.044 277.172.106 327.935.936 336.119.742 350.200.558 4,2%<br />

Robo/Theft 13.556.016 17.927.827 16.068.074 15.563.055 15.300.593 14.658.800 16.231.328 10,7%<br />

RC/Liability 9.348.079 13.140.436 12.238.095 16.710.739 16.592.310 16.547.096 18.340.542 10,8%<br />

Caución/Surety 4.936.716 8.061.246 8.334.339 10.316.719 12.117.934 13.988.464 14.455.198 3,3%<br />

Transporte/Cargo 20.603.630 23.094.188 25.036.077 31.692.810 35.236.359 32.285.488 34.416.174 6,6%<br />

Otros/Others 20.158.370 30.183.661 28.849.464 36.113.443 37.413.507 33.798.881 46.022.089 36,2%<br />

Rurales/Rural 15.145.249 21.352.458 21.622.204 25.413.436 34.236.422 29.224.248 39.015.921 33,5%<br />

Ingeniería/Engineering 3.110.152 1.857.705 1.890.691 2.581.909 5.487.760 8.167.486 7.427.531 -9,1%<br />

Crédito/Credit 112.541 161.697 152.999 464.897 1.502.554 1.911.616 2.757.719 44,3%<br />

Subtotal Patrimoniales/Subtotal Non-Life 241.141.639 350.607.485 377.340.886 451.747.511 534.130.724 536.486.549 582.599.142 8,6%<br />

Vida/Life 57.726.526 86.726.562 93.853.346 112.931.014 147.848.514 158.514.892 171.281.601 8,1%<br />

Vida Previsional/Pension Life 32.848.551 51.712.473 78.852.377 101.133.753 145.108.575 172.911.741 196.016.815 13,4%<br />

Subtotal Vida/Subtotal Life 90.575.077 138.439.035 172.705.723 214.064.767 292.957.089 331.426.633 367.298.416 10,8%<br />

Accidentes/Accidents 110.994.669 157.337.601 175.247.413 220.341.590 284.376.533 287.267.336 294.706.176 2,6%<br />

Total 442.711.385 646.384.122 725.294.023 886.153.868 1.111.464.346 1.155.180.518 1.244.603.734 7,7%<br />

maduración del sistema previsional.<br />

El mercado de seguros en nuestro país se encuentra altamente<br />

concentrado. Desde el año 1995 el mercado opera en régimen de<br />

competencia, excepto por la rama Accidentes de Trabajo, que continúa<br />

en monopolio a favor del BSE. Considerando el mercado<br />

abierto a la competencia hasta el año 2012, se observa un proceso<br />

de desconcentración. Sin embargo en el año 2013 la concentración<br />

del mercado aumentó, y en el ejercicio 2014 no registró cambios.<br />

La concentración del mercado se explica fundamentalmente por<br />

los seguros de Accidentes de Trabajo, como decíamos, en régimen<br />

de monopolio legal a favor del<br />

BSE, y por los seguros de Vida<br />

Previsional, rama en la que<br />

el sector privado no participa<br />

debido a los problemas de diseño<br />

del sistema y, en especial,<br />

a la falta de calce de moneda<br />

entre los activos y pasivos<br />

que genera ese seguro.<br />

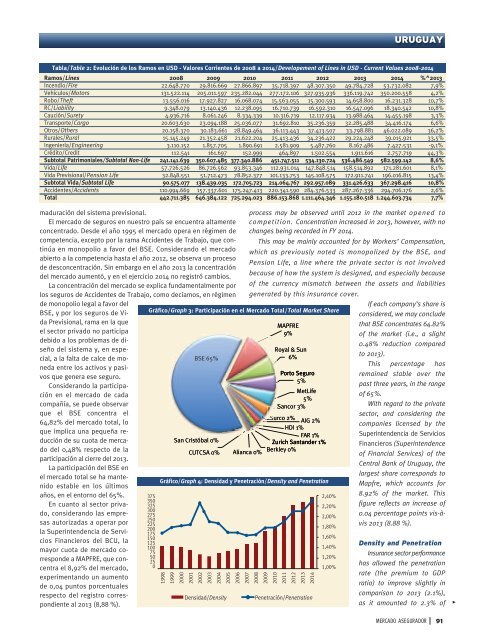

Considerando la participación<br />

en el mercado de cada<br />

compañía, se puede observar<br />

que el BSE concentra el<br />

64,82% del mercado total, lo<br />

que implica una pequeña reducción<br />

de su cuota de mercado<br />

del 0,48% respecto de la<br />

participación al cierre del 2013.<br />

La participación del BSE en<br />

el mercado total se ha mantenido<br />

estable en los últimos<br />

años, en el entorno del 65%.<br />

En cuanto al sector privado,<br />

considerando las empresas<br />

autorizadas a operar por<br />

la Superintendencia de Servicios<br />

Financieros del BCU, la<br />

mayor cuota de mercado corresponde<br />

a MAPFRE, que concentra<br />

el 8,92% del mercado,<br />

experimentando un aumento<br />

de 0,04 puntos porcentuales<br />

respecto del registro correspondiente<br />

al 2013 (8,88 %).<br />

Gráfico/Graph 3: Participación en el Mercado Total/Total Market Share<br />

375<br />

350<br />

325<br />

300<br />

275<br />

250<br />

225<br />

200<br />

175<br />

150<br />

125<br />

100<br />

75<br />

50<br />

25<br />

0<br />

BSE 65%<br />

San Cristóbal 0%<br />

CUTCSA 0% Alianca 0%<br />

Gráfico/Graph 4: Densidad y Penetración/Density and Penetration<br />

1998<br />

1999<br />

2000<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

2010<br />

2011<br />

2012<br />

2013<br />

2014<br />

Densidad/Density<br />

process may be observed until 2012 in the market opened to<br />

competition. Concentration increased in 2013, however, with no<br />

<strong>change</strong>s being recorded in FY 2014.<br />

This may be mainly accounted for by Workers’ Compensation,<br />

which as previously noted is monopolized by the BSE, and<br />

Pension Life, a line where the private sector is not involved<br />

because of how the system is designed, and especially because<br />

of the currency mismatch between the assets and liabilities<br />

generated by this insurance cover.<br />

If each company’s share is<br />

considered, we may conclude<br />

MAPFRE<br />

9%<br />

that BSE concentrates 64.82%<br />

of the market (i.e., a slight<br />

0.48% reduction compared<br />

Royal & Sun<br />

6%<br />

to 2013).<br />

This percentage has<br />

Porto Seguro<br />

5%<br />

remained stable over the<br />

past three years, in the range<br />

MetLife<br />

of 65%.<br />

5%<br />

Sancor 3%<br />

With regard to the private<br />

sector, and considering the<br />

Surco 2%<br />

AIG 2%<br />

companies licensed by the<br />

HDI 1%<br />

FAR 1%<br />

Superintendencia de Servicios<br />

Zurich Santander 1%<br />

Financieros (Superintendence<br />

Berkley 0%<br />

of Financial Services) of the<br />

Central Bank of Uruguay, the<br />

largest share corresponds to<br />

Mapfre, which accounts for<br />

2,40%<br />

2,20%<br />

2,00%<br />

1,80%<br />

8.92% of the market. This<br />

figure reflects an increase of<br />

0.04 percentage points vis-àvis<br />

2013 (8.88 %).<br />

Penetración/Penetration<br />

1,60%<br />

1,40%<br />

1,20%<br />

1,00%<br />

Density and Penetration<br />

Insurance sector performance<br />

has allowed the penetration<br />

rate (the premium to GDP<br />

ratio) to improve slightly in<br />

comparison to 2013 (2.1%),<br />

as it amounted to 2.3% of<br />

><br />

MERCADO ASEGURADOR<br />

91