Climate change

Mercado_Nov2015

Mercado_Nov2015

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

ARGENTINA<br />

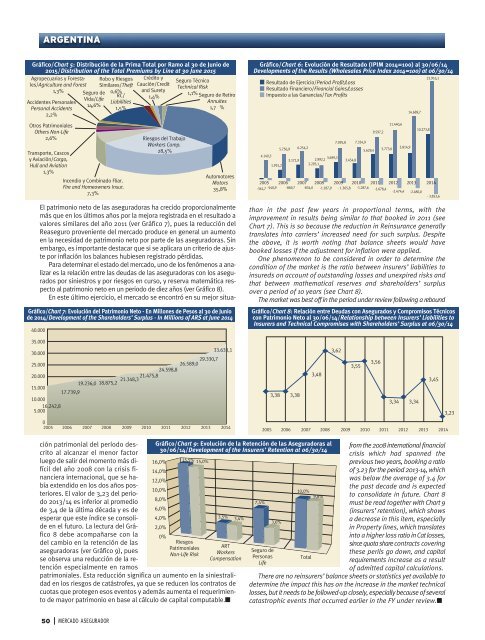

Gráfico/Chart 5: Distribución de la Prima Total por Ramo al 30 de Junio de<br />

2015/Distribution of the Total Premiums by Line at 30 June 2015<br />

Agropecuarios y Forestales/Agriculture<br />

Robo y Riesgos Crédito y<br />

and Forest Similares/Theft Caución/Credit<br />

1,3%<br />

0,6% and Surety<br />

1,4%<br />

Accidentes Personales<br />

Personal Accidents<br />

2,2%<br />

Otros Patrimoniales<br />

Others Non-Life<br />

2,6%<br />

Seguro de<br />

Vida/Life<br />

14,6%<br />

RC/<br />

Liabilities<br />

1,5%<br />

Transporte, Cascos<br />

y Aviación/Cargo,<br />

Hull and Aviation<br />

1,3%<br />

Incendio y Combinado Fliar.<br />

Fire and Homeowners Insur.<br />

7,3%<br />

Riesgos del Trabajo<br />

Workers Comp.<br />

28,5%<br />

Seguro Técnico<br />

Technical Risk<br />

1,1% Seguro de Retiro<br />

Annuites<br />

1,7 %<br />

Automotores<br />

Motors<br />

35,8%<br />

Gráfico/Chart 7: Evolución del Patrimonio Neto - En Millones de Pesos al 30 de Junio<br />

de 2014/Development of the Shareholders’ Surplus - In Millions of AR$ at June 2014<br />

40.000<br />

35.000<br />

33.633,1<br />

30.000<br />

25.000<br />

26.589,0 29.330,7<br />

24.598,8<br />

20.000<br />

19.236,0 18.875,2 21.348,3 21.475,8<br />

15.000<br />

17.739,9<br />

10.000<br />

16.242,8<br />

5.000<br />

0<br />

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014<br />

Gráfico/Chart 6: Evolución de Resultado (IPIM 2014=100) al 30/06/14<br />

Developments of the Results (Wholesales Price Index 2014=100) at 06/30/14<br />

Resultado de Ejercicio/Period Profit/Loss<br />

Resultado Financiero/Financial Gains/Losses<br />

Impuesto a las Ganancias/Tax Profits<br />

7.095,8 7.334,9<br />

5.756,9 6.254,2<br />

5.629,4 5.773,6<br />

5.814,9<br />

4.140,3<br />

3.171,9 2.992,1 3.699,3<br />

1.915,2<br />

2.293,1<br />

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014<br />

-361,7 -540,9 -869,7 -834,0 -1.187,9 - 1.365,8 -1.287,6 -1.678,4<br />

-2.474,4 -2.480,0<br />

- 3.853,6<br />

3.454,8<br />

9.597,2<br />

11.440,6<br />

14.689,7<br />

10.273,8<br />

23.916,1<br />

than in the past few years in proportional terms, with the<br />

improvement in results being similar to that booked in 2011 (see<br />

Chart 7). This is so because the reduction in Reinsurance generally<br />

translates into carriers’ increased need for such surplus. Despite<br />

the above, it is worth noting that balance sheets would have<br />

booked losses if the adjustment for inflation were applied.<br />

One phenomenon to be considered in order to determine the<br />

condition of the market is the ratio between insurers’ liabilities to<br />

insureds on account of outstanding losses and unexpired risks and<br />

that between mathematical reserves and shareholders’ surplus<br />

over a period of 10 years (see Chart 8).<br />

The market was best off in the period under review following a rebound<br />

Gráfico/Chart 8: Relación entre Deudas con Asegurados y Compromisos Técnicos<br />

con Patrimonio Neto al 30/06/14/Relationship between Insurers’ Liabilities to<br />

Insurers and Technical Compromises with Shareholders’ Surplus at 06/30/14<br />

3,38 3,38<br />

3,48<br />

3,62<br />

3,55<br />

3,56<br />

3,34 3,34<br />

3,45<br />

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014<br />

3,23<br />

El patrimonio neto de las aseguradoras ha crecido proporcionalmente<br />

más que en los últimos años por la mejora registrada en el resultado a<br />

valores similares del año 2011 (ver Gráfico 7), pues la reducción del<br />

Reaseguro proveniente del mercado produce en general un aumento<br />

en la necesidad de patrimonio neto por parte de las aseguradoras. Sin<br />

embargo, es importante destacar que si se aplicara un criterio de ajuste<br />

por inflación los balances hubiesen registrado pérdidas.<br />

Para determinar el estado del mercado, uno de los fenómenos a analizar<br />

es la relación entre las deudas de las aseguradoras con los asegurados<br />

por siniestros y por riesgos en curso, y reserva matemática respecto<br />

al patrimonio neto en un periodo de diez años (ver Gráfico 8).<br />

En este último ejercicio, el mercado se encontró en su mejor situación<br />

patrimonial del período descrito<br />

al alcanzar el menor factor<br />

luego de salir del momento más difícil<br />

del año 2008 con la crisis financiera<br />

internacional, que se había<br />

extendido en los dos años posteriores.<br />

El valor de 3,23 del periodo<br />

2013/14 es inferior al promedio<br />

de 3,4 de la última década y es de<br />

esperar que este índice se consolide<br />

en el futuro. La lectura del Gráfico<br />

8 debe acompañarse con la<br />

del cambio en la retención de las<br />

aseguradoras (ver Gráfico 9), pues<br />

se observa una reducción de la retención<br />

especialmente en ramos<br />

patrimoniales. Esta reducción significa un aumento en la siniestralidad<br />

en los riesgos de catástrofes, ya que se reducen los contratos de<br />

cuotas que protegen esos eventos y además aumenta el requerimiento<br />

de mayor patrimonio en base al cálculo de capital computable.■<br />

Gráfico/Chart 9: Evolución de la Retención de las Aseguradoras al<br />

30/06/14/Development of the Insurers’ Retention at 06/30/14<br />

16,0% 15,5% 15,0%<br />

14,0%<br />

12,0%<br />

10,0%<br />

10,0%<br />

9,8%<br />

8,0%<br />

7,4%<br />

6,0%<br />

4,0%<br />

3,5% 3,4%<br />

3,6%<br />

2,0%<br />

0%<br />

Riesgos<br />

Patrimoniales<br />

Non-Life Risk<br />

ART<br />

Workers<br />

Compensation<br />

Seguro de<br />

Personas<br />

Life<br />

Total<br />

from the 2008 international financial<br />

crisis which had spanned the<br />

previous two years, booking a ratio<br />

of 3.23 for the period 2013-14, which<br />

was below the average of 3.4 for<br />

the past decade and is expected<br />

to consolidate in future. Chart 8<br />

must be read together with Chart 9<br />

(insurers’ retention), which shows<br />

a decrease in this item, especially<br />

in Property lines, which translates<br />

into a higher loss ratio in Cat losses,<br />

since quota share contracts covering<br />

these perils go down, and capital<br />

requirements increase as a result<br />

of admitted capital calculations.<br />

There are no reinsurers’ balance sheets or statistics yet available to<br />

determine the impact this has on the increase in the market technical<br />

losses, but it needs to be followed-up closely, especially because of several<br />

catastrophic events that occurred earlier in the FY under review.■<br />

50<br />

MERCADO ASEGURADOR