Climate change

Mercado_Nov2015

Mercado_Nov2015

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

ECUADOR<br />

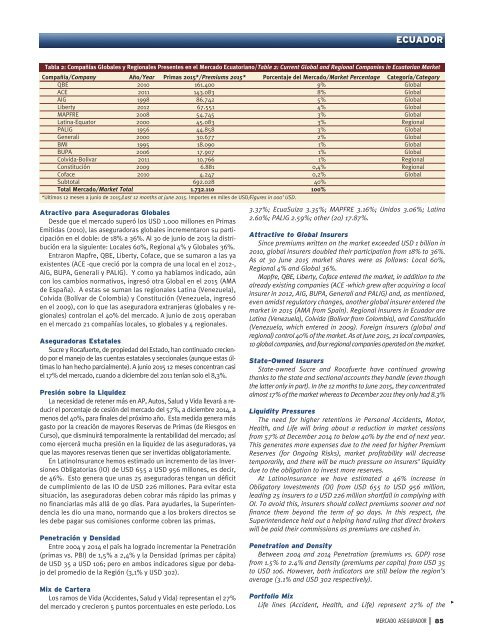

Tabla 2: Compañías Globales y Regionales Presentes en el Mercado Ecuatoriano/Table 2: Current Global and Regional Companies in Ecuatorian Market<br />

Compañía/Company Año/Year Primas 2015*/Premiums 2015* Porcentaje del Mercado/Market Percentage Categoría/Category<br />

QBE 2010 161.400 9% Global<br />

ACE 2011 143.083 8% Global<br />

AIG 1998 86.742 5% Global<br />

Liberty 2012 67.551 4% Global<br />

MAPFRE 2008 54.745 3% Global<br />

Latina-Equator 2000 45.083 3% Regional<br />

PALIG 1956 44.858 3% Global<br />

Generali 2000 30.677 2% Global<br />

BMI 1995 18.090 1% Global<br />

BUPA 2006 17.907 1% Global<br />

Colvida-Bolivar 2011 10.766 1% Regional<br />

Constitución 2009 6.881 0,4% Regional<br />

Coface 2010 4.247 0,2% Global<br />

Subtotal 692.028 40%<br />

Total Mercado/Market Total 1.732.110 100%<br />

*Ultimos 12 meses a junio de 2015/Last 12 months at june 2015. Importes en miles de USD/Figures in 000’ USD.<br />

Atractivo para Aseguradoras Globales<br />

Desde que el mercado superó los USD 1.000 millones en Primas<br />

Emitidas (2010), las aseguradoras globales incrementaron su participación<br />

en el doble: de 18% a 36%. Al 30 de junio de 2015 la distribución<br />

era la siguiente: Locales 60%, Regional 4% y Globales 36%.<br />

Entraron Mapfre, QBE, Liberty, Coface, que se sumaron a las ya<br />

existentes (ACE -que creció por la compra de una local en el 2012-,<br />

AIG, BUPA, Generali y PALIG). Y como ya habíamos indicado, aún<br />

con los cambios normativos, ingresó otra Global en el 2015 (AMA<br />

de España). A estas se suman las regionales Latina (Venezuela),<br />

Colvida (Bolívar de Colombia) y Constitución (Venezuela, ingresó<br />

en el 2009), con lo que las aseguradora extranjeras (globales y regionales)<br />

controlan el 40% del mercado. A junio de 2015 operaban<br />

en el mercado 21 compañías locales, 10 globales y 4 regionales.<br />

Aseguradoras Estatales<br />

Sucre y Rocafuerte, de propiedad del Estado, han continuado creciendo<br />

por el manejo de las cuentas estatales y seccionales (aunque estas últimas<br />

lo han hecho parcialmente). A junio 2015 12 meses concentran casi<br />

el 17% del mercado, cuando a diciembre del 2011 tenían solo el 8,3%.<br />

Presión sobre la Liquidez<br />

La necesidad de retener más en AP, Autos, Salud y Vida llevará a reducir<br />

el porcentaje de cesión del mercado del 57%, a diciembre 2014, a<br />

menos del 40%, para finales del próximo año. Esta medida genera más<br />

gasto por la creación de mayores Reservas de Primas (de Riesgos en<br />

Curso), que disminuirá temporalmente la rentabilidad del mercado; así<br />

como ejercerá mucha presión en la liquidez de las aseguradoras, ya<br />

que las mayores reservas tienen que ser invertidas obligatoriamente.<br />

En LatinoInsurance hemos estimado un incremento de las Inversiones<br />

Obligatorias (IO) de USD 655 a USD 956 millones, es decir,<br />

de 46%. Esto genera que unas 25 aseguradoras tengan un déficit<br />

de cumplimiento de las IO de USD 226 millones. Para evitar esta<br />

situación, las aseguradoras deben cobrar más rápido las primas y<br />

no financiarlas más allá de 90 días. Para ayudarles, la Superintendencia<br />

les dio una mano, normando que a los brokers directos se<br />

les debe pagar sus comisiones conforme cobren las primas.<br />

Penetración y Densidad<br />

Entre 2004 y 2014 el país ha logrado incrementar la Penetración<br />

(primas vs. PBI) de 1,5% a 2,4% y la Densidad (primas per cápita)<br />

de USD 35 a USD 106; pero en ambos indicadores sigue por debajo<br />

del promedio de la Región (3,1% y USD 302).<br />

Mix de Cartera<br />

Los ramos de Vida (Accidentes, Salud y Vida) representan el 27%<br />

del mercado y crecieron 5 puntos porcentuales en este período. Los<br />

3.37%; EcuaSuiza 3.35%; MAPFRE 3.16%; Unidos 3.06%; Latina<br />

2.60%; PALIG 2.59%; other (20) 17.87%.<br />

Attractive to Global Insurers<br />

Since premiums written on the market exceeded USD 1 billion in<br />

2010, global insurers doubled their participation from 18% to 36%.<br />

As at 30 June 2015 market shares were as follows: Local 60%,<br />

Regional 4% and Global 36%.<br />

Mapfre, QBE, Liberty, Coface entered the market, in addition to the<br />

already existing companies (ACE -which grew after acquiring a local<br />

insurer in 2012, AIG, BUPA, Generali and PALIG) and, as mentioned,<br />

even amidst regulatory <strong>change</strong>s, another global insurer entered the<br />

market in 2015 (AMA from Spain). Regional insurers in Ecuador are<br />

Latina (Venezuela), Colvida (Bolívar from Colombia), and Constitución<br />

(Venezuela, which entered in 2009). Foreign insurers (global and<br />

regional) control 40% of the market. As at June 2015, 21 local companies,<br />

10 global companies, and four regional companies operated on the market.<br />

State-Owned Insurers<br />

State-owned Sucre and Rocafuerte have continued growing<br />

thanks to the state and sectional accounts they handle (even though<br />

the latter only in part). In the 12 months to June 2015, they concentrated<br />

almost 17% of the market whereas to December 2011 they only had 8.3%<br />

Liquidity Pressures<br />

The need for higher retentions in Personal Accidents, Motor,<br />

Health, and Life will bring about a reduction in market cessions<br />

from 57% at December 2014 to below 40% by the end of next year.<br />

This generates more expenses due to the need for higher Premium<br />

Reserves (for Ongoing Risks), market profitability will decrease<br />

temporarily, and there will be much pressure on insurers’ liquidity<br />

due to the obligation to invest more reserves.<br />

At LatinoInsurance we have estimated a 46% increase in<br />

Obligatory Investments (OI) from USD 655 to USD 956 million,<br />

leading 25 insurers to a USD 226 million shortfall in complying with<br />

OI. To avoid this, insurers should collect premiums sooner and not<br />

finance them beyond the term of 90 days. In this respect, the<br />

Superintendence held out a helping hand ruling that direct brokers<br />

will be paid their commissions as premiums are cashed in.<br />

Penetration and Density<br />

Between 2004 and 2014 Penetration (premiums vs. GDP) rose<br />

from 1.5% to 2.4% and Density (premiums per capita) from USD 35<br />

to USD 106. However, both indicators are still below the region’s<br />

average (3.1% and USD 302 respectively).<br />

Portfolio Mix<br />

Life lines (Accident, Health, and Life) represent 27% of the<br />

><br />

MERCADO ASEGURADOR<br />

85