Climate change

Mercado_Nov2015

Mercado_Nov2015

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

MEXICO<br />

una alta participación de los hogares en la formación bruta de capital<br />

fijo. Esto implicaría que los hogares intermedien financieramente<br />

su ahorro de una manera más eficiente, en lugar de formar<br />

su propio capital fijo en hogares y negocios. Esto último limita sus<br />

posibilidades de ampliar el abanico de financiamiento, desarrollar<br />

horizontes de inversión, adoptar mejores tecnologías y asegurarse<br />

contra posibles siniestros. Una mayor masa salarial y una mayor<br />

penetración de los seguros en la economía (y, por ende, un mayor<br />

ahorro e inclusión financiera), tendría un doble efecto positivo:<br />

• Mayor capital disponible producto de un mayor ahorro.<br />

• Mejor canalización del capital al privilegiar inversiones en el<br />

sector moderno, donde presumiblemente hay mayor número de<br />

0,6%<br />

0,5%<br />

0,4%<br />

0,3%<br />

0,2%<br />

0,1%<br />

bienes públicos e infraestructura<br />

que potencia el uso del capital<br />

invertido y, por tanto, una<br />

mayor tasa de rendimiento del<br />

capital en promedio.<br />

Esto tiene como consecuencia<br />

una importante pérdida de<br />

competitividad; ya que el seguro<br />

no sólo influye en diversas<br />

áreas torales para que una región<br />

sea más competitiva (la infraestructura,<br />

la innovación, la<br />

sofisticación de los negocios o<br />

el bienestar), sino que es determinante<br />

para el estado de derecho.<br />

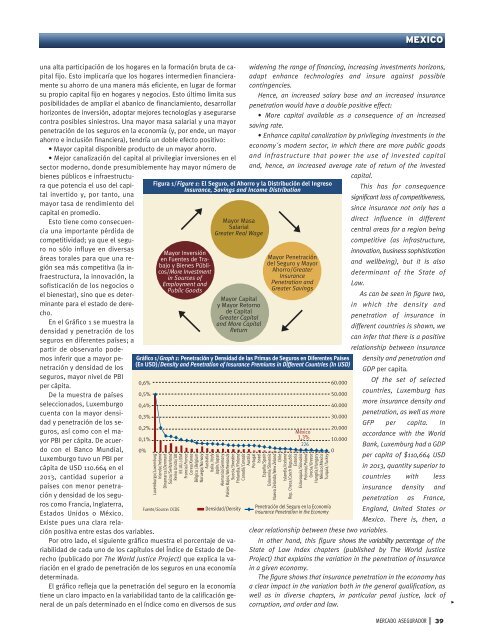

En el Gráfico 1 se muestra la<br />

densidad y penetración de los<br />

seguros en diferentes países; a<br />

partir de observarlo podemos<br />

inferir que a mayor penetración<br />

y densidad de los<br />

seguros, mayor nivel de PBI<br />

per cápita.<br />

De la muestra de países<br />

seleccionados, Luxemburgo<br />

cuenta con la mayor densidad<br />

y penetración de los seguros,<br />

así como con el mayor<br />

PBI per cápita. De acuerdo<br />

con el Banco Mundial,<br />

Luxemburgo tuvo un PBI per<br />

cápita de USD 110.664 en el<br />

2013, cantidad superior a<br />

países con menor penetración<br />

y densidad de los seguros<br />

como Francia, Inglaterra,<br />

Estados Unidos o México.<br />

Existe pues una clara relación<br />

positiva entre estas dos variables.<br />

Por otro lado, el siguiente gráfico muestra el porcentaje de variabilidad<br />

de cada uno de los capítulos del Índice de Estado de Derecho<br />

(publicado por The World Justice Project) que explica la variación<br />

en el grado de penetración de los seguros en una economía<br />

determinada.<br />

El gráfico refleja que la penetración del seguro en la economía<br />

tiene un claro impacto en la variabilidad tanto de la calificación general<br />

de un país determinado en el índice como en diversos de sus<br />

0%<br />

Figura 1/Figure 1: El Seguro, el Ahorro y la Distribución del Ingreso<br />

Insurance, Savings and Income Distribution<br />

Mayor Inversión<br />

en Fuentes de Trabajo<br />

y Bienes Públicos/More<br />

Investment<br />

in Sources of<br />

Employment and<br />

Public Goods<br />

Mayor Masa<br />

Salarial<br />

Greater Real Wage<br />

Mayor Capital<br />

y Mayor Retorno<br />

de Capital<br />

Greater Capital<br />

and More Capital<br />

Return<br />

Luxemburgo/Luxemburg<br />

Irlanda/Ireland<br />

Dinamarca/Denmark<br />

Suiza/Switzerland<br />

Reino Unido/UK<br />

EE.UU./USA<br />

Francia/France<br />

Corea/Korea<br />

Bélgica /Belgium<br />

Noruega/Norway<br />

Australia<br />

Italia /Italy<br />

Japón/Japan<br />

Alemania/Germany<br />

Países Bajos/Netherlands<br />

Suecia/Sweden<br />

Finlandia/Finland<br />

Canadá/Canada<br />

Austria<br />

Portugal<br />

Israel<br />

España/Spain<br />

Eslovenia/Slovenia<br />

Nueva Zelanda/New Zeland<br />

Chile<br />

Islandia/Iceland<br />

Rep. Checa/Czech Republic<br />

Estonia<br />

Eslovaquia/Slovakia<br />

Polonia/Poland<br />

Grecia/Greece<br />

Hungría/Hungary<br />

México/Mexico<br />

Turquía/Turkey<br />

widening the range of financing, increasing investments horizons,<br />

adapt enhance technologies and insure against possible<br />

contingencies.<br />

Hence, an increased salary base and an increased insurance<br />

penetration would have a double positive effect:<br />

• More capital available as a consequence of an increased<br />

saving rate.<br />

• Enhance capital canalization by privileging investments in the<br />

economy´s modern sector, in which there are more public goods<br />

and infrastructure that power the use of invested capital<br />

and, hence, an increased average rate of return of the invested<br />

capital.<br />

This has for consequence<br />

significant loss of competitiveness,<br />

since insurance not only has a<br />

direct influence in different<br />

central areas for a region being<br />

competitive (as infrastructure,<br />

innovation, business sophistication<br />

Mayor Penetración<br />

del Seguro y Mayor<br />

and wellbeing), but it is also<br />

Ahorro/Greater<br />

determinant of the State of<br />

Insurance<br />

Penetration and<br />

Law.<br />

Greater Savings<br />

As can be seen in figure two,<br />

in which the density and<br />

penetration of insurance in<br />

different countries is shown, we<br />

can infer that there is a positive<br />

relationship between insurance<br />

density and penetration and<br />

GDP per capita.<br />

60.000 Of the set of selected<br />

countries, Luxemburg has<br />

50.000<br />

more insurance density and<br />

40.000<br />

penetration, as well as more<br />

30.000<br />

GFP per capita. In<br />

20.000<br />

México<br />

accordance with the World<br />

1,3% 10.000<br />

226<br />

Bank, Luxemburg had a GDP<br />

0<br />

per capita of $110,664 USD<br />

in 2013, quantity superior to<br />

countries with less<br />

insurance density and<br />

penetration as France,<br />

England, United States or<br />

Mexico. There is, then, a<br />

clear relationship between these two variables.<br />

Gráfico 1/Graph 1: Penetración y Densidad de las Primas de Seguros en Diferentes Países<br />

(En USD)/Density and Penetration of Insurance Premiums in Different Countries (In USD)<br />

Fuente/Source: OCDE Densidad/Density Penetración del Seguro en la Economía<br />

Insurance Penetration in the Economy<br />

In other hand, this figure shows the variability percentage of the<br />

State of Law Index chapters (published by The World Justice<br />

Project) that explains the variation in the penetration of insurance<br />

in a given economy.<br />

The figure shows that insurance penetration in the economy has<br />

a clear impact in the variation both in the general qualification, as<br />

well as in diverse chapters, in particular penal justice, lack of<br />

corruption, and order and law.<br />

><br />

MERCADO ASEGURADOR<br />

39