Climate change

Mercado_Nov2015

Mercado_Nov2015

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

82><br />

ECUADOR<br />

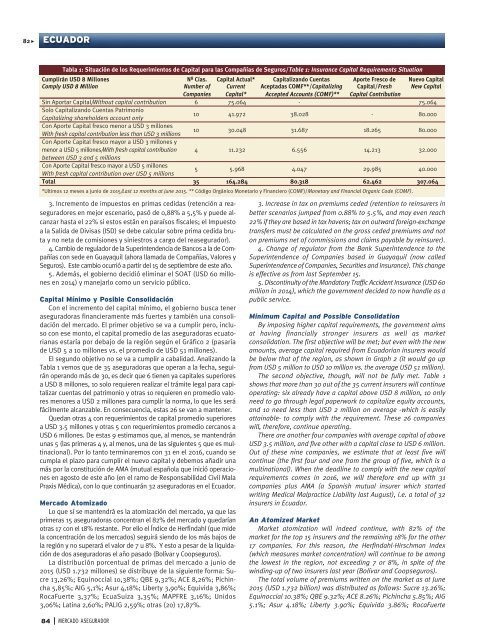

Tabla 1: Situación de los Requerimientos de Capital para las Compañías de Seguros/Table 1: Insurance Capital Requirements Situation<br />

Cumplirán USD 8 Millones Nº Cías. Capital Actual* Capitalizando Cuentas Aporte Fresco de Nuevo Capital<br />

Comply USD 8 Million Number of Current Aceptadas COMF**/Capitalizing Capital/Fresh New Capital<br />

Companies Capital* Accepted Accounts (COMF)** Capital Contribution<br />

Sin Aportar Capital/Without capital contribution 6 75.064 - 75.064<br />

Solo Capitalizando Cuentas Patrimonio<br />

Capitalizing shareholders account only<br />

10 41.972 38.028 - 80.000<br />

Con Aporte Capital fresco menor a USD 3 millones<br />

With fresh capital contribution less than USD 3 millions<br />

10 30.048 31.687 18.265 80.000<br />

Con Aporte Capital fresco mayor a USD 3 millones y<br />

menor a USD 5 millones/With fresh capital contribution 4 11.232 6.556 14.213 32.000<br />

between USD 3 and 5 millions<br />

Con Aporte Capital fresco mayor a USD 5 millones<br />

With fresh capital contribution over USD 5 millions<br />

5 5.968 4.047 29.985 40.000<br />

Total 35 164.284 80.318 62.462 307.064<br />

*Ultimos 12 meses a junio de 2015/Last 12 months at june 2015. ** Código Orgánico Monetario y Financiero (COMF)/Monetary and Financial Organic Code (COMF).<br />

3. Incremento de impuestos en primas cedidas (retención a reaseguradores<br />

en mejor escenario, pasó de 0,88% a 5,5% y puede alcanzar<br />

hasta el 22% si estos están en paraísos fiscales; el Impuesto<br />

a la Salida de Divisas (ISD) se debe calcular sobre prima cedida bruta<br />

y no neta de comisiones y siniestros a cargo del reasegurador).<br />

4. Cambio de regulador de la Superintendencia de Bancos a la de Compañías<br />

con sede en Guayaquil (ahora llamada de Compañías, Valores y<br />

Seguros). Este cambio ocurrió a partir del 15 de septiembre de este año.<br />

5. Además, el gobierno decidió eliminar el SOAT (USD 60 millones<br />

en 2014) y manejarlo como un servicio público.<br />

Capital Mínimo y Posible Consolidación<br />

Con el incremento del capital mínimo, el gobierno busca tener<br />

aseguradoras financieramente más fuertes y también una consolidación<br />

del mercado. El primer objetivo se va a cumplir pero, incluso<br />

con ese monto, el capital promedio de las aseguradoras ecuatorianas<br />

estaría por debajo de la región según el Gráfico 2 (pasaría<br />

de USD 5 a 10 millones vs. el promedio de USD 51 millones).<br />

El segundo objetivo no se va a cumplir a cabalidad. Analizando la<br />

Tabla 1 vemos que de 35 aseguradoras que operan a la fecha, seguirán<br />

operando más de 30, es decir que 6 tienen ya capitales superiores<br />

a USD 8 millones, 10 solo requieren realizar el trámite legal para capitalizar<br />

cuentas del patrimonio y otras 10 requieren en promedio valores<br />

menores a USD 2 millones para cumplir la norma, lo que les será<br />

fácilmente alcanzable. En consecuencia, estas 26 se van a mantener.<br />

Quedan otras 4 con requerimientos de capital promedio superiores<br />

a USD 3.5 millones y otras 5 con requerimientos promedio cercanos a<br />

USD 6 millones. De estas 9 estimamos que, al menos, se mantendrán<br />

unas 5 (las primeras 4 y, al menos, una de las siguientes 5 que es multinacional).<br />

Por lo tanto terminaremos con 31 en el 2016, cuando se<br />

cumpla el plazo para cumplir el nuevo capital y debemos añadir una<br />

más por la constitución de AMA (mutual española que inició operaciones<br />

en agosto de este año (en el ramo de Responsabilidad Civil Mala<br />

Praxis Médica), con lo que continuarán 32 aseguradoras en el Ecuador.<br />

Mercado Atomizado<br />

Lo que sí se mantendrá es la atomización del mercado, ya que las<br />

primeras 15 aseguradoras concentran el 82% del mercado y quedarían<br />

otras 17 con el 18% restante. Por ello el Índice de Herfindahl (que mide<br />

la concentración de los mercados) seguirá siendo de los más bajos de<br />

la región y no superará el valor de 7 u 8%. Y esto a pesar de la liquidación<br />

de dos aseguradoras el año pasado (Bolívar y Coopseguros).<br />

La distribución porcentual de primas del mercado a junio de<br />

2015 (USD 1.732 millones) se distribuye de la siguiente forma: Sucre<br />

13,26%; Equinoccial 10,38%; QBE 9,32%; ACE 8,26%; Pichincha<br />

5,85%; AIG 5,1%; Asur 4,18%; Liberty 3,90%; Equivida 3,86%;<br />

RocaFuerte 3,37%; EcuaSuiza 3,35%; MAPFRE 3,16%; Unidos<br />

3,06%; Latina 2,60%; PALIG 2,59%; otras (20) 17,87%.<br />

3. Increase in tax on premiums ceded (retention to reinsurers in<br />

better scenarios jumped from 0.88% to 5.5%, and may even reach<br />

22% if they are based in tax havens; tax on outward foreign-ex<strong>change</strong><br />

transfers must be calculated on the gross ceded premiums and not<br />

on premiums net of commissions and claims payable by reinsurer).<br />

4. Change of regulator from the Bank Superintendence to the<br />

Superintendence of Companies based in Guayaquil (now called<br />

Superintendence of Companies, Securities and Insurance). This <strong>change</strong><br />

is effective as from last September 15.<br />

5. Discontinuity of the Mandatory Traffic Accident Insurance (USD 60<br />

million in 2014), which the government decided to now handle as a<br />

public service.<br />

Minimum Capital and Possible Consolidation<br />

By imposing higher capital requirements, the government aims<br />

at having financially stronger insurers as well as market<br />

consolidation. The first objective will be met; but even with the new<br />

amounts, average capital required from Ecuadorian insurers would<br />

be below that of the region, as shown in Graph 2 (it would go up<br />

from USD 5 million to USD 10 million vs. the average USD 51 million).<br />

The second objective, though, will not be fully met. Table 1<br />

shows that more than 30 out of the 35 current insurers will continue<br />

operating: six already have a capital above USD 8 million, 10 only<br />

need to go through legal paperwork to capitalize equity accounts,<br />

and 10 need less than USD 2 million on average -which is easily<br />

attainable- to comply with the requirement. These 26 companies<br />

will, therefore, continue operating.<br />

There are another four companies with average capital of above<br />

USD 3.5 million, and five other with a capital close to USD 6 million.<br />

Out of these nine companies, we estimate that at least five will<br />

continue (the first four and one from the group of five, which is a<br />

multinational). When the deadline to comply with the new capital<br />

requirements comes in 2016, we will therefore end up with 31<br />

companies plus AMA (a Spanish mutual insurer which started<br />

writing Medical Malpractice Liability last August), i.e. a total of 32<br />

insurers in Ecuador.<br />

An Atomized Market<br />

Market atomization will indeed continue, with 82% of the<br />

market for the top 15 insurers and the remaining 18% for the other<br />

17 companies. For this reason, the Herfindahl-Hirschman Index<br />

(which measures market concentration) will continue to be among<br />

the lowest in the region, not exceeding 7 or 8%, in spite of the<br />

winding-up of two insurers last year (Bolívar and Coopseguros).<br />

The total volume of premiums written on the market as at June<br />

2015 (USD 1.732 billion) was distributed as follows: Sucre 13.26%;<br />

Equinoccial 10.38%; QBE 9.32%; ACE 8.26%; Pichincha 5.85%; AIG<br />

5.1%; Asur 4.18%; Liberty 3.90%; Equivida 3.86%; RocaFuerte<br />

84<br />

MERCADO ASEGURADOR