Climate change

Mercado_Nov2015

Mercado_Nov2015

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

COLOMBIA<br />

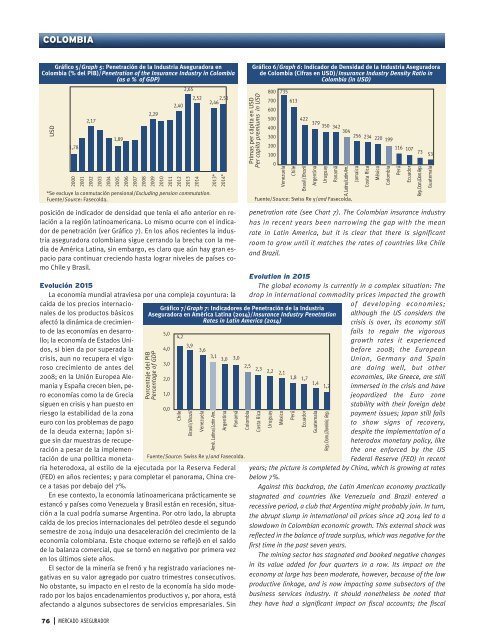

Gráfico 5/Graph 5: Penetración de la Industria Aseguradora en<br />

Colombia (% del PIB)/Penetration of the Insurance Industry in Colombia<br />

(as a % of GDP)<br />

2,65<br />

2,52<br />

2,46 2,51<br />

2,40<br />

2,29<br />

2,17<br />

USD<br />

1,78<br />

1,89<br />

2000<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

2010<br />

2011<br />

2012<br />

2013<br />

2014<br />

*Se excluye la conmutación pensional/Excluding pension commutation.<br />

Fuente/Source: Fasecolda.<br />

2013*<br />

2014*<br />

Gráfico 6/Graph 6: Indicador de Densidad de la Industria Aseguradora<br />

de Colombia (Cifras en USD)/Insurance Industry Density Ratio in<br />

Colombia (in USD)<br />

Primas per cápita en USD<br />

Per capita premiums in USD<br />

800 735<br />

700 613<br />

600<br />

500 422 379<br />

400<br />

350 342<br />

304<br />

300<br />

256 234 220 199<br />

200<br />

116 107 73<br />

100<br />

53<br />

0<br />

Venezuela<br />

Chile<br />

Brasil/Brazil<br />

Argentina<br />

Uruguay<br />

Panamá<br />

A. Latina/Latin Am.<br />

Fuente/Source: Swiss Re y/and Fasecolda.<br />

Jamaica<br />

Costa Rica<br />

México<br />

Colombia<br />

Perú<br />

Ecuador<br />

Rep. Dom./Dom. Rep.<br />

Guatemala<br />

posición de indicador de densidad que tenía el año anterior en relación<br />

a la región latinoamericana. Lo mismo ocurre con el indicador<br />

de penetración (ver Gráfico 7). En los años recientes la industria<br />

aseguradora colombiana sigue cerrando la brecha con la media<br />

de América Latina, sin embargo, es claro que aún hay gran espacio<br />

para continuar creciendo hasta lograr niveles de países como<br />

Chile y Brasil.<br />

Evolución 2015<br />

La economía mundial atraviesa por una compleja coyuntura: la<br />

caída de los precios internacionales<br />

de los productos básicos<br />

afectó la dinámica de crecimiento<br />

de las economías en desarrollo;<br />

la economía de Estados Unidos,<br />

si bien da por superada la<br />

crisis, aun no recupera el vigoroso<br />

crecimiento de antes del<br />

2008; en la Unión Europea Alemania<br />

y España crecen bien, pero<br />

economías como la de Grecia<br />

siguen en crisis y han puesto en<br />

riesgo la estabilidad de la zona<br />

euro con los problemas de pago<br />

de la deuda externa; Japón sigue<br />

sin dar muestras de recuperación<br />

a pesar de la implementación<br />

de una política monetaria<br />

heterodoxa, al estilo de la ejecutada por la Reserva Federal<br />

(FED) en años recientes; y para completar el panorama, China crece<br />

a tasas por debajo del 7%.<br />

En ese contexto, la economía latinoamericana prácticamente se<br />

estancó y países como Venezuela y Brasil están en recesión, situación<br />

a la cual podría sumarse Argentina. Por otro lado, la abrupta<br />

caída de los precios internacionales del petróleo desde el segundo<br />

semestre de 2014 indujo una desaceleración del crecimiento de la<br />

economía colombiana. Este choque externo se reflejó en el saldo<br />

de la balanza comercial, que se tornó en negativo por primera vez<br />

en los últimos siete años.<br />

El sector de la minería se frenó y ha registrado variaciones negativas<br />

en su valor agregado por cuatro trimestres consecutivos.<br />

No obstante, su impacto en el resto de la economía ha sido moderado<br />

por los bajos encadenamientos productivos y, por ahora, está<br />

afectando a algunos subsectores de servicios empresariales. Sin<br />

Gráfico 7/Graph 7: Indicadores de Penetración de la Industria<br />

Aseguradora en América Latina (2014)/Insurance Industry Penetration<br />

Rates in Latin America (2014)<br />

Porcentaje del PIB<br />

Percentage of GDP<br />

5,0<br />

4,0<br />

3,0<br />

2,0<br />

1,0<br />

0,0<br />

4,2<br />

3,9<br />

Chile<br />

Brasil/Brazil<br />

3,6<br />

Venezuela<br />

3,1 3,0 3,0<br />

Amé. Latina/Latin Am.<br />

Argentina<br />

Panamá<br />

Fuente/Source: Swiss Re y/and Fasecolda.<br />

Colombia<br />

penetration rate (see Chart 7). The Colombian insurance industry<br />

has in recent years been narrowing the gap with the mean<br />

rate in Latin America, but it is clear that there is significant<br />

room to grow until it matches the rates of countries like Chile<br />

and Brazil.<br />

Evolution in 2015<br />

The global economy is currently in a complex situation: The<br />

drop in international commodity prices impacted the growth<br />

2,5 2,3 2,2 2,1<br />

1,8 1,7<br />

1,4<br />

1,2<br />

Costa Rica<br />

Uruguay<br />

México<br />

Perú<br />

Ecuador<br />

Guatemala<br />

Rep. Dom./Dominic. Rep.<br />

of developing economies;<br />

although the US considers the<br />

crisis is over, its economy still<br />

fails to regain the vigorous<br />

growth rates it experienced<br />

before 2008; the European<br />

Union, Germany and Spain<br />

are doing well, but other<br />

economies, like Greece, are still<br />

immersed in the crisis and have<br />

jeopardized the Euro zone<br />

stability with their foreign debt<br />

payment issues; Japan still fails<br />

to show signs of recovery,<br />

despite the implementation of a<br />

heterodox monetary policy, like<br />

the one enforced by the US<br />

Federal Reserve (FED) in recent<br />

years; the picture is completed by China, which is growing at rates<br />

below 7%.<br />

Against this backdrop, the Latin American economy practically<br />

stagnated and countries like Venezuela and Brazil entered a<br />

recessive period, a club that Argentina might probably join. In turn,<br />

the abrupt slump in international oil prices since 2Q 2014 led to a<br />

slowdown in Colombian economic growth. This external shock was<br />

reflected in the balance of trade surplus, which was negative for the<br />

first time in the past seven years.<br />

The mining sector has stagnated and booked negative <strong>change</strong>s<br />

in its value added for four quarters in a row. Its impact on the<br />

economy at large has been moderate, however, because of the low<br />

productive linkage, and is now impacting some subsectors of the<br />

business services industry. It should nonetheless be noted that<br />

they have had a significant impact on fiscal accounts; the fiscal<br />

76<br />

MERCADO ASEGURADOR