Climate change

Mercado_Nov2015

Mercado_Nov2015

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

PARAGUAY<br />

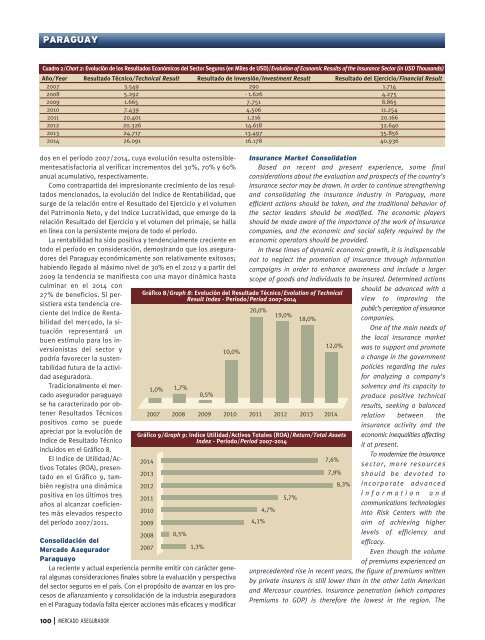

Cuadro 2/Chart 2: Evolución de los Resultados Económicos del Sector Seguros (en Miles de USD)/Evolution of Economic Results of the Insurance Sector (in USD Thousands)<br />

Año/Year Resultado Técnico/Technical Result Resultado de Inversión/Investment Result Resultado del Ejercicio/Financial Result<br />

2007 3.549 290 1.714<br />

2008 5.292 - 1.626 4.275<br />

2009 1.665 7.751 8.865<br />

2010 7.439 4.506 11.254<br />

2011 20.401 1.216 20.166<br />

2012 20.326 14.618 32.640<br />

2013 24.717 13.497 35.856<br />

2014 26.091 16.178 40.936<br />

dos en el período 2007/2014, cuya evolución resulta ostensiblementesatisfactoria<br />

al verificar incrementos del 30%, 70% y 60%<br />

anual acumulativo, respectivamente.<br />

Como contrapartida del impresionante crecimiento de los resultados<br />

mencionados, la evolución del Indice de Rentabilidad, que<br />

surge de la relación entre el Resultado del Ejercicio y el volumen<br />

del Patrimonio Neto, y del Indice Lucratividad, que emerge de la<br />

relación Resultado del Ejercicio y el volumen del primaje, se halla<br />

en línea con la persistente mejora de todo el período.<br />

La rentabilidad ha sido positiva y tendencialmente creciente en<br />

todo el período en consideración, demostrando que los aseguradores<br />

del Paraguay económicamente son relativamente exitosos;<br />

habiendo llegado al máximo nivel de 30% en el 2012 y a partir del<br />

2009 la tendencia se manifiesta con una mayor dinámica hasta<br />

culminar en el 2014 con<br />

27% de beneficios. Si persistiera<br />

esta tendencia creciente<br />

del Indice de Rentabilidad<br />

del mercado, la situación<br />

representará un<br />

buen estímulo para los inversionistas<br />

del sector y<br />

podría favorecer la sustentabilidad<br />

futura de la actividad<br />

aseguradora.<br />

Tradicionalmente el mercado<br />

asegurador paraguayo<br />

se ha caracterizado por obtener<br />

Resultados Técnicos<br />

positivos como se puede<br />

apreciar por la evolución de<br />

Indice de Resultado Técnico<br />

incluidos en el Gráfico 8.<br />

El Indice de Utilidad/Activos<br />

Totales (ROA), presentado<br />

en el Gráfico 9, también<br />

registra una dinámica<br />

positiva en los últimos tres<br />

años al alcanzar coeficientes<br />

más elevados respecto<br />

del período 2007/2011.<br />

2008 0,5%<br />

Consolidación del<br />

Mercado Asegurador 2007<br />

1,3%<br />

Paraguayo<br />

La reciente y actual experiencia permite emitir con carácter general<br />

algunas consideraciones finales sobre la evaluación y perspectiva<br />

del sector seguros en el país. Con el propósito de avanzar en los procesos<br />

de afianzamiento y consolidación de la industria aseguradora<br />

en el Paraguay todavía falta ejercer acciones más eficaces y modificar<br />

Gráfico 8/Graph 8: Evolución del Resultado Técnico/Evolution of Technical<br />

Result Index - Período/Period 2007-2014<br />

20,0% 19,0% 18,0%<br />

12,0%<br />

1,0% 1,7%<br />

0,5%<br />

10,0%<br />

2007 2008 2009 2010 2011 2012 2013 2014<br />

Gráfico 9/Graph 9: Indice Utilidad/Activos Totales (ROA)/Return/Total Assets<br />

Index - Período/Period 2007-2014<br />

2014<br />

2013<br />

2012<br />

2011<br />

2010<br />

2009<br />

Insurance Market Consolidation<br />

Based on recent and present experience, some final<br />

considerations about the evaluation and prospects of the country’s<br />

insurance sector may be drawn. In order to continue strengthening<br />

and consolidating the insurance industry in Paraguay, more<br />

efficient actions should be taken, and the traditional behavior of<br />

the sector leaders should be modified. The economic players<br />

should be made aware of the importance of the work of insurance<br />

companies, and the economic and social safety required by the<br />

economic operators should be provided.<br />

In these times of dynamic economic growth, it is indispensable<br />

not to neglect the promotion of insurance through information<br />

campaigns in order to enhance awareness and include a larger<br />

scope of goods and individuals to be insured. Determined actions<br />

4,7%<br />

4,1%<br />

5,7%<br />

7,6%<br />

7,9%<br />

8,3%<br />

should be advanced with a<br />

view to improving the<br />

public’s perception of insurance<br />

companies.<br />

One of the main needs of<br />

the local insurance market<br />

was to support and promote<br />

a <strong>change</strong> in the government<br />

policies regarding the rules<br />

for analyzing a company’s<br />

solvency and its capacity to<br />

produce positive technical<br />

results, seeking a balanced<br />

relation between the<br />

insurance activity and the<br />

economic inequalities affecting<br />

it at present.<br />

To modernize the insurance<br />

s e c t o r , m o r e r e s o u r c e s<br />

should be devoted to<br />

i n c o r p o r a t e a d v a n c e d<br />

i n f o r m a t i o n a n d<br />

communications technologies<br />

into Risk Centers with the<br />

aim of achieving higher<br />

levels of efficiency and<br />

efficacy.<br />

Even though the volume<br />

of premiums experienced an<br />

unprecedented rise in recent years, the figure of premiums written<br />

by private insurers is still lower than in the other Latin American<br />

and Mercosur countries. Insurance penetration (which compares<br />

Premiums to GDP) is therefore the lowest in the region. The<br />

100<br />

MERCADO ASEGURADOR