Climate change

Mercado_Nov2015

Mercado_Nov2015

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

30><br />

CHILE<br />

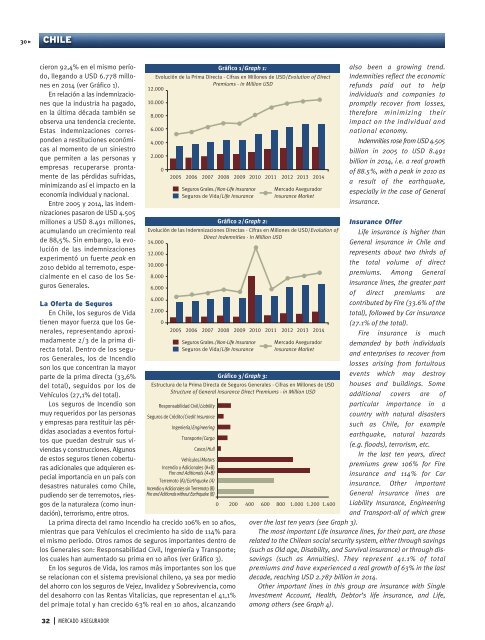

cieron 92,4% en el mismo período,<br />

llegando a USD 6.778 millones<br />

en 2014 (ver Gráfico 1).<br />

En relación a las indemnizaciones<br />

que la industria ha pagado,<br />

en la última década también se<br />

observa una tendencia creciente.<br />

Estas indemnizaciones corresponden<br />

a restituciones económicas<br />

al momento de un siniestro<br />

que permiten a las personas y<br />

empresas recuperarse prontamente<br />

de las pérdidas sufridas,<br />

minimizando así el impacto en la<br />

economía individual y nacional.<br />

Entre 2005 y 2014, las indemnizaciones<br />

pasaron de USD 4.505<br />

millones a USD 8.491 millones,<br />

acumulando un crecimiento real<br />

de 88,5%. Sin embargo, la evolución<br />

de las indemnizaciones<br />

experimentó un fuerte peak en<br />

2010 debido al terremoto, especialmente<br />

en el caso de los Seguros<br />

Generales.<br />

La Oferta de Seguros<br />

En Chile, los seguros de Vida<br />

tienen mayor fuerza que los Generales,<br />

representando aproximadamente<br />

2/3 de la prima directa<br />

total. Dentro de los seguros<br />

Generales, los de Incendio<br />

son los que concentran la mayor<br />

parte de la prima directa (33,6%<br />

del total), seguidos por los de<br />

Vehículos (27,1% del total).<br />

Los seguros de Incendio son<br />

muy requeridos por las personas<br />

y empresas para restituir las pérdidas<br />

asociadas a eventos fortuitos<br />

que puedan destruir sus viviendas<br />

y construcciones. Algunos<br />

de estos seguros tienen coberturas<br />

adicionales que adquieren especial<br />

importancia en un país con<br />

desastres naturales como Chile,<br />

pudiendo ser de terremotos, riesgos<br />

de la naturaleza (como inundación),<br />

terrorismo, entre otros.<br />

La prima directa del ramo Incendio ha crecido 106% en 10 años,<br />

mientras que para Vehículos el crecimiento ha sido de 114% para<br />

el mismo período. Otros ramos de seguros importantes dentro de<br />

los Generales son: Responsabilidad Civil, Ingeniería y Transporte;<br />

los cuales han aumentado su prima en 10 años (ver Gráfico 3).<br />

En los seguros de Vida, los ramos más importantes son los que<br />

se relacionan con el sistema previsional chileno, ya sea por medio<br />

del ahorro con los seguros de Vejez, Invalidez y Sobrevivencia, como<br />

del desahorro con las Rentas Vitalicias, que representan el 41,1%<br />

del primaje total y han crecido 63% real en 10 años, alcanzando<br />

Gráfico 1/Graph 1:<br />

Evolución de la Prima Directa - Cifras en Millones de USD/Evolution of Direct<br />

Premiums - In Million USD<br />

12.000<br />

10.000<br />

8.000<br />

6.000<br />

4.000<br />

2.000<br />

0<br />

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014<br />

Seguros Grales./Non-Life Insurance<br />

Seguros de Vida/Life Insurance<br />

Mercado Asegurador<br />

Insurance Market<br />

Gráfico 2/Graph 2:<br />

Evolución de las Indemnizaciones Directas - Cifras en Millones de USD/Evolution of<br />

Direct Indemnities - In Million USD<br />

14.000<br />

12.000<br />

10.000<br />

8.000<br />

6.000<br />

4.000<br />

2.000<br />

0<br />

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014<br />

Seguros Grales./Non-Life Insurance<br />

Seguros de Vida/Life Insurance<br />

Mercado Asegurador<br />

Insurance Market<br />

Gráfico 3/Graph 3:<br />

Estructura de la Prima Directa de Seguros Generales - Cifras en Millones de USD<br />

Structure of General Insurance Direct Premiums - in Million USD<br />

Responsabilidad Civil/Liability<br />

Seguros de Crédito/Credit Insurance<br />

Ingeniería/Engineering<br />

Transporte/Cargo<br />

Casco/Hull<br />

Vehículos/Motors<br />

Incendio y Adicionales (A+B)<br />

Fire and Aditionals (A+B)<br />

Terremoto (A)/Earthquake (A)<br />

Incendio y Adicionales sin Terremoto (B)<br />

Fire and Aditionals without Earthquake (B)<br />

0 200 400 600 800 1.000 1.200 1.400<br />

also been a growing trend.<br />

Indemnities reflect the economic<br />

refunds paid out to help<br />

individuals and companies to<br />

promptly recover from losses,<br />

therefore minimizing their<br />

impact on the individual and<br />

national economy.<br />

Indemnities rose from USD 4.505<br />

billion in 2005 to USD 8.491<br />

billion in 2014, i.e. a real growth<br />

of 88.5%, with a peak in 2010 as<br />

a result of the earthquake,<br />

especially in the case of General<br />

insurance.<br />

Insurance Offer<br />

Life insurance is higher than<br />

General insurance in Chile and<br />

represents about two thirds of<br />

the total volume of direct<br />

premiums. Among General<br />

insurance lines, the greater part<br />

of direct premiums are<br />

contributed by Fire (33.6% of the<br />

total), followed by Car insurance<br />

(27.1% of the total).<br />

Fire insurance is much<br />

demanded by both individuals<br />

and enterprises to recover from<br />

losses arising from fortuitous<br />

events which may destroy<br />

houses and buildings. Some<br />

additional covers are of<br />

particular importance in a<br />

country with natural disasters<br />

such as Chile, for example<br />

earthquake, natural hazards<br />

(e.g. floods), terrorism, etc.<br />

In the last ten years, direct<br />

premiums grew 106% for Fire<br />

insurance and 114% for Car<br />

insurance. Other important<br />

General insurance lines are<br />

Liability Insurance, Engineering<br />

and Transport-all of which grew<br />

over the last ten years (see Graph 3).<br />

The most important Life insurance lines, for their part, are those<br />

related to the Chilean social security system, either through savings<br />

(such as Old age, Disability, and Survival insurance) or through dissavings<br />

(such as Annuities). They represent 41.1% of total<br />

premiums and have experienced a real growth of 63% in the last<br />

decade, reaching USD 2.787 billion in 2014.<br />

Other important lines in this group are insurance with Single<br />

Investment Account, Health, Debtor’s life insurance, and Life,<br />

among others (see Graph 4).<br />

32<br />

MERCADO ASEGURADOR