Climate change

Mercado_Nov2015

Mercado_Nov2015

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

CHILE<br />

Regulación<br />

En la actualidad la industria aseguradora<br />

está sujeta a una fuerte<br />

regulación, la que ha sido modernizada<br />

en los últimos años para responder<br />

a las solicitudes del mercado<br />

y proteger a los consumidores.<br />

El regulador de la industria es<br />

la Superintendencia de Valores y<br />

Seguros, que siguiendo las tendencias<br />

internacionales, está en<br />

proceso de modificar el enfoque<br />

de supervisión con dos focos<br />

principales: la solvencia de las<br />

compañías para enfrentar sus<br />

compromisos y la conducta de<br />

mercado, que hace referencia a la forma como las compañías enfrentan<br />

sus negocios y adoptan sus decisiones. Los principales<br />

ejemplos son la actualización del Código de Comercio que incluyó<br />

la reforma de los Contratos de Seguros, la modificación del Reglamento<br />

de Auxiliares de Comercio que renovó el proceso de ajuste y<br />

liquidación de siniestros y por otra parte, uno de los mayores cambios<br />

para el sector asegurador desde el año 1981, como es el proyecto<br />

de ley que modifica el DFL N°251, introduciendo la exigencia<br />

de capital basado en los riesgos que cada compañía asume.<br />

Por otro lado, la industria aseguradora en Chile también ha fijado<br />

metas propias de competencia y solvencia, para lo cual ha creado<br />

el Código de Autorregulación y el Compendio de Buenas Prácticas<br />

Corporativas, el Consejo de Autorregulación y la figura del Defensor<br />

del Asegurado.<br />

Perspectivas<br />

El año 2014, la AACH definió las proyecciones para la industria<br />

en 2015 que establecen aumentos esperados de la prima directa<br />

de 3,5% real para el total de la industria, lo que se divide en un aumento<br />

de 3,2% para los seguros Generales y 3,7% para los de Vida.<br />

Analizado datos del primer semestre de 2015, se observa que<br />

la prima directa ha aumentado en un 11,4% real respecto a igual<br />

período en el año anterior, es decir, un crecimiento sobre nuestras<br />

proyecciones originales. Por lo tanto, cabe esperar que durante este<br />

año el crecimiento de la industria se sitúe en el rango proyectado<br />

y para 2016 se puede prever un escenario similar, debido a que<br />

las proyecciones de crecimiento de la economía en general no deberían<br />

presentar variaciones importantes respecto a 2014 y 2015.<br />

Treinta años de crecimiento sostenido han generado cambios<br />

en la conducta de los chilenos en cuanto consumidores, y actualmente<br />

exigen mayor información, mayor transparencia y el cabal<br />

cumplimiento de promesas.<br />

Un significativo desafío de la industria es la adaptación a los cambios<br />

demográficos. Un elemento que presiona la reforma previsional<br />

tiene relación con el envejecimiento poblacional y la variación de la<br />

estructura etaria, la industria aseguradora debe ser capaz de incorporar<br />

estos cambios en el diseño de los seguros y el cálculo de las<br />

primas, al mismo tiempo que desarrollar productos para las nuevas<br />

necesidades de la población, especialmente los de mayor edad.<br />

Finalmente, la industria aseguradora tiene un rol principal ante<br />

desastres naturales. En 2010 demostró gran capacidad de respuesta<br />

luego del terremoto y ganó confianza de los consumidores, pero es<br />

necesario que continúe ampliando la base de clientes y que sea capaz<br />

de adaptarse a los riesgos que presenta el cambio climático.■<br />

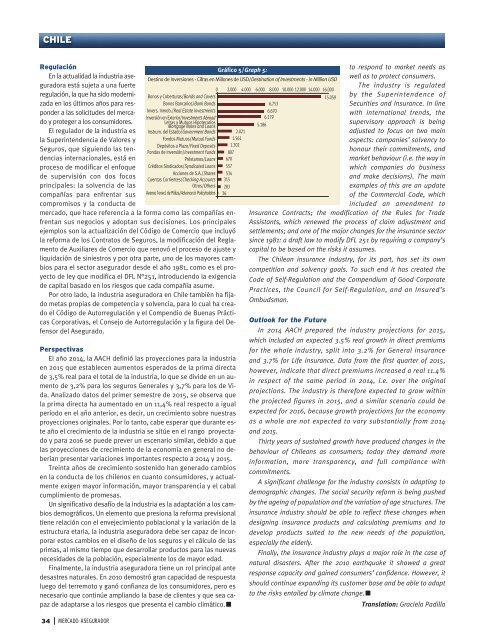

Gráfico 5/Graph 5:<br />

Destino de Inversiones - Cifras en Millones de USD/Destination of Investments - in Million USD<br />

Bonos y Coberturas/Bonds and Covers<br />

Bonos Bancarios/Bank Bonds<br />

Invers. Inmob./Real Estate Investments<br />

Inversión en Exterior/Investments Abroad<br />

Letras y Mutuos Hipotecarios<br />

Mortgage Notes and Loans<br />

Instrum. del Estado/Government Bonds<br />

Fondos Mutuos/Mutual Funds<br />

Depósitos a Plazo/Fixed Deposits<br />

Fondos de Inversión/Investment Funds<br />

Préstamos/Loans<br />

Créditos Sindicados/Syndicated Loans<br />

Acciones de S.A./Shares<br />

Cuentas Corrientes/Checking Accounts<br />

Otros/Others<br />

Avance Tened. de Póliza/Advance to Policyholders<br />

0 2.000 4.000 6.000 8.000 10.000 12.000 14.000 16.000<br />

15.059<br />

6.753<br />

6.670<br />

6.179<br />

5.186<br />

2.021<br />

1.561<br />

1.302<br />

807<br />

670<br />

557<br />

534<br />

315<br />

283<br />

36<br />

to respond to market needs as<br />

well as to protect consumers.<br />

The industry is regulated<br />

by the Superintendence of<br />

Securities and Insurance. In line<br />

with international trends, the<br />

supervisory approach is being<br />

adjusted to focus on two main<br />

aspects: companies’ solvency to<br />

honour their commitments, and<br />

market behaviour (i.e. the way in<br />

which companies do business<br />

and make decisions). The main<br />

examples of this are an update<br />

of the Commercial Code, which<br />

included an amendment to<br />

Insurance Contracts; the modification of the Rules for Trade<br />

Assistants, which renewed the process of claim adjustment and<br />

settlements; and one of the major <strong>change</strong>s for the insurance sector<br />

since 1981: a draft law to modify DFL 251 by requiring a company’s<br />

capital to be based on the risks it assumes.<br />

The Chilean insurance industry, for its part, has set its own<br />

competition and solvency goals. To such end it has created the<br />

Code of Self-Regulation and the Compendium of Good Corporate<br />

Practices, the Council for Self-Regulation, and an Insured’s<br />

Ombudsman.<br />

Outlook for the Future<br />

In 2014 AACH prepared the industry projections for 2015,<br />

which included an expected 3.5% real growth in direct premiums<br />

for the whole industry, split into 3.2% for General insurance<br />

and 3.7% for Life insurance. Data from the first quarter of 2015,<br />

however, indicate that direct premiums increased a real 11.4%<br />

in respect of the same period in 2014, i.e. over the original<br />

projections. The industry is therefore expected to grow within<br />

the projected figures in 2015, and a similar scenario could be<br />

expected for 2016, because growth projections for the economy<br />

as a whole are not expected to vary substantially from 2014<br />

and 2015.<br />

Thirty years of sustained growth have produced <strong>change</strong>s in the<br />

behaviour of Chileans as consumers; today they demand more<br />

information, more transparency, and full compliance with<br />

commitments.<br />

A significant challenge for the industry consists in adapting to<br />

demographic <strong>change</strong>s. The social security reform is being pushed<br />

by the ageing of population and the variation of age structures. The<br />

insurance industry should be able to reflect these <strong>change</strong>s when<br />

designing insurance products and calculating premiums and to<br />

develop products suited to the new needs of the population,<br />

especially the elderly.<br />

Finally, the insurance industry plays a major role in the case of<br />

natural disasters. After the 2010 earthquake it showed a great<br />

response capacity and gained consumers’ confidence. However, it<br />

should continue expanding its customer base and be able to adapt<br />

to the risks entailed by climate <strong>change</strong>.■<br />

Translation: Graciela Padilla<br />

34<br />

MERCADO ASEGURADOR