NTRAC Final Study - Nebraska Department of Roads - State of ...

NTRAC Final Study - Nebraska Department of Roads - State of ...

NTRAC Final Study - Nebraska Department of Roads - State of ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

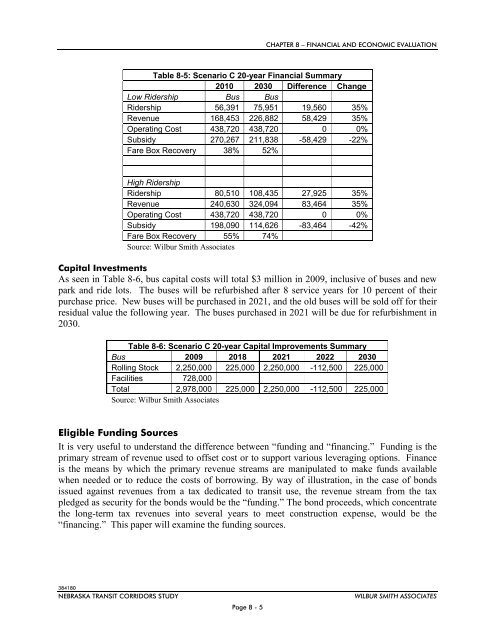

CHAPTER 8 – FINANCIAL AND ECONOMIC EVALUATION<br />

Table 8-5: Scenario C 20-year Financial Summary<br />

2010 2030 Difference Change<br />

Low Ridership Bus Bus<br />

Ridership 56,391 75,951 19,560 35%<br />

Revenue 168,453 226,882 58,429 35%<br />

Operating Cost 438,720 438,720 0 0%<br />

Subsidy 270,267 211,838 -58,429 -22%<br />

Fare Box Recovery 38% 52%<br />

High Ridership<br />

Ridership 80,510 108,435 27,925 35%<br />

Revenue 240,630 324,094 83,464 35%<br />

Operating Cost 438,720 438,720 0 0%<br />

Subsidy 198,090 114,626 -83,464 -42%<br />

Fare Box Recovery 55% 74%<br />

Source: Wilbur Smith Associates<br />

Capital Investments<br />

As seen in Table 8-6, bus capital costs will total $3 million in 2009, inclusive <strong>of</strong> buses and new<br />

park and ride lots. The buses will be refurbished after 8 service years for 10 percent <strong>of</strong> their<br />

purchase price. New buses will be purchased in 2021, and the old buses will be sold <strong>of</strong>f for their<br />

residual value the following year. The buses purchased in 2021 will be due for refurbishment in<br />

2030.<br />

Table 8-6: Scenario C 20-year Capital Improvements Summary<br />

Bus 2009 2018 2021 2022 2030<br />

Rolling Stock 2,250,000 225,000 2,250,000 -112,500 225,000<br />

Facilities 728,000<br />

Total 2,978,000 225,000 2,250,000 -112,500 225,000<br />

Source: Wilbur Smith Associates<br />

Eligible Funding Sources<br />

It is very useful to understand the difference between “funding and “financing.” Funding is the<br />

primary stream <strong>of</strong> revenue used to <strong>of</strong>fset cost or to support various leveraging options. Finance<br />

is the means by which the primary revenue streams are manipulated to make funds available<br />

when needed or to reduce the costs <strong>of</strong> borrowing. By way <strong>of</strong> illustration, in the case <strong>of</strong> bonds<br />

issued against revenues from a tax dedicated to transit use, the revenue stream from the tax<br />

pledged as security for the bonds would be the “funding.” The bond proceeds, which concentrate<br />

the long-term tax revenues into several years to meet construction expense, would be the<br />

“financing.” This paper will examine the funding sources.<br />

384180<br />

NEBRASKA TRANSIT CORRIDORS STUDY<br />

Page 8 - 5<br />

WILBUR SMITH ASSOCIATES