Gigabit January 2019

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Tipping the scale<br />

on mobile payments<br />

By Mark Elliott, Division President, Mastercard Southern Africa<br />

The app economy has changed the way we live. We depend<br />

on our smartphone apps for everything from entertainment<br />

to photography, to messaging, personal productivity and<br />

ordering transport or accommodation. In South Africa, we’re<br />

increasingly using our smartphones for in-app, in-store and<br />

online payments.<br />

“The promise of mobile payment<br />

services lies in creating safer,<br />

richer experiences for consumers<br />

and merchants.”<br />

We’re also seeing merchants use apps that turn their<br />

smartphones into point of sale devices or use QR codes to<br />

accept mobile payments from their customers. The mobile<br />

device brings the convenience, safety and customer choice<br />

associated with cashless transactions to spaza shops, flea<br />

market stalls, trades people like plumbers and electricians,<br />

and other sectors where traditional card terminals are not a<br />

practical or affordable solution.<br />

Mobile innovations need to<br />

improve the consumer experience<br />

As we think about the rapid adoption of mobile payments,<br />

the promise of mobile payment services lies in creating safer,<br />

richer experiences for consumers and merchants. The key<br />

is not to simply recreate what you could do before, but to<br />

make paying for things simpler, safer and faster. That’s why<br />

connecting with consumers wherever they are and whenever<br />

they want is critical.<br />

Imagine, for example, a world where people don’t need to<br />

queue for hours to send money to their families in the rural<br />

areas or where no one needs to withdraw cash from an ATM<br />

and then stand in a long queue at a retailer on a Saturday<br />

to pay a rates bill. They don’t even need to log in to online<br />

banking and input a lot of payment information. Instead,<br />

they’ll be able to scan a QR code on the statement and pay<br />

from an app. This is a world where merchants don’t need<br />

to keep large amounts of cash on their premises. It’s one<br />

where consumers demand convenience and control, and<br />

expect payment experiences to make their lives better.<br />

We are not talking about a distant future, either. In South Africa,<br />

more than 900,000 ratepayers in the City of Ekurhuleni<br />

can pay their municipal bills online with their smartphones,<br />

using Masterpass, our global digital payment service. Masterpass<br />

is also accepted online by a growing list of merchants<br />

of all sizes as well as in-app for convenient air and<br />

data mobile top-up.<br />

Partnerships key to drive<br />

mass digital payment adoption<br />

The consumer experience is simple, but there is a lot of<br />

complexity in the background. Without collaboration across<br />

industries to ensure that digital payments systems are<br />

secure and interoperable, it will be impossible to deliver the<br />

experiences consumers demand or to scale mobile payments.<br />

That’s why we are collaborating with key players to develop<br />

and deliver new consumer propositions that span multiple<br />

industries across multiple channels – in-store, in-app and<br />

online.<br />

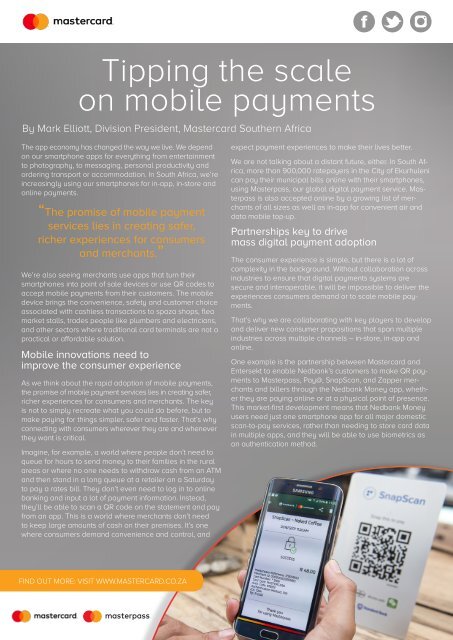

One example is the partnership between Mastercard and<br />

Entersekt to enable Nedbank’s customers to make QR payments<br />

to Masterpass, Pay@, SnapScan, and Zapper merchants<br />

and billers through the Nedbank Money app, whether<br />

they are paying online or at a physical point of presence.<br />

This market-first development means that Nedbank Money<br />

users need just one smartphone app for all major domestic<br />

scan-to-pay services, rather than needing to store card data<br />

in multiple apps, and they will be able to use biometrics as<br />

an authentication method.<br />

FIND OUT MORE: VISIT WWW.MASTERCARD.CO.ZA