Méthodes de Monte Carlo appliquées au pricing d ... - Maths-fi.com

Méthodes de Monte Carlo appliquées au pricing d ... - Maths-fi.com

Méthodes de Monte Carlo appliquées au pricing d ... - Maths-fi.com

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

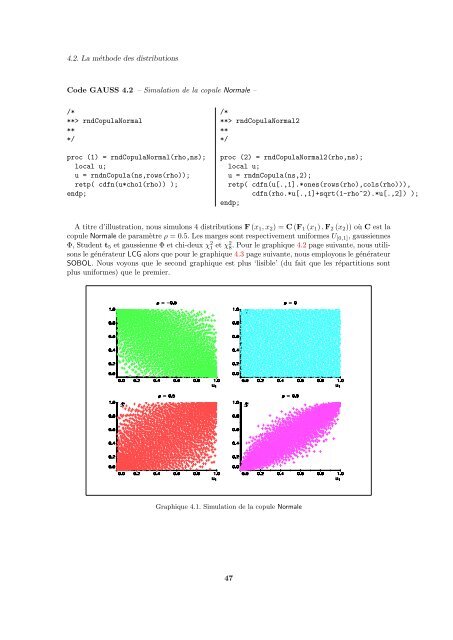

4.2. La métho<strong>de</strong> <strong>de</strong>s distributionsCo<strong>de</strong> GAUSS 4.2 – Simulation <strong>de</strong> la copule Normale –/***> rndCopulaNormal***/proc (1) = rndCopulaNormal(rho,ns);local u;u = rndnCopula(ns,rows(rho));retp( cdfn(u*chol(rho)) );endp;/***> rndCopulaNormal2***/proc (2) = rndCopulaNormal2(rho,ns);local u;u = rndnCopula(ns,2);retp( cdfn(u[.,1].*ones(rows(rho),cols(rho))),cdfn(rho.*u[.,1]+sqrt(1-rho^2).*u[.,2]) );endp;A titre d’illustration, nous simulons 4 distributions F (x 1 , x 2 ) = C (F 1 (x 1 ) , F 2 (x 2 )) où C est lacopule Normale <strong>de</strong> paramètre ρ = 0.5. Les marges sont respectivement uniformes U [0,1] , g<strong>au</strong>ssiennesΦ, Stu<strong>de</strong>nt t 5 et g<strong>au</strong>ssienne Φ et chi-<strong>de</strong>ux χ 2 1 et χ 2 8. Pour le graphique 4.2 page suivante, nous utilisonsle générateur LCG alors que pour le graphique 4.3 page suivante, nous employons le générateurSOBOL. Nous voyons que le second graphique est plus ‘lisible’ (du fait que les répartitions sontplus uniformes) que le premier.Graphique 4.1. Simulation <strong>de</strong> la copule Normale47