Méthodes de Monte Carlo appliquées au pricing d ... - Maths-fi.com

Méthodes de Monte Carlo appliquées au pricing d ... - Maths-fi.com

Méthodes de Monte Carlo appliquées au pricing d ... - Maths-fi.com

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

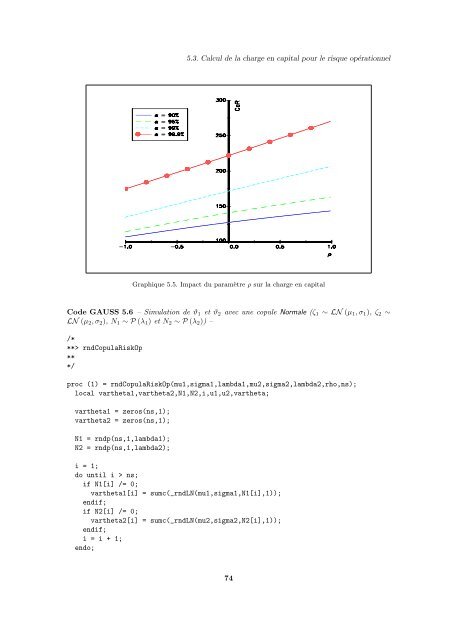

5.3. Calcul <strong>de</strong> la charge en capital pour le risque opérationnelGraphique 5.5. Impact du paramètre ρ sur la charge en capitalCo<strong>de</strong> GAUSS 5.6 – Simulation <strong>de</strong> ϑ 1 et ϑ 2 avec une copule Normale (ζ 1 ∼ LN (µ 1 , σ 1 ), ζ 2 ∼LN (µ 2 , σ 2 ), N 1 ∼ P (λ 1 ) et N 2 ∼ P (λ 2 )) –/***> rndCopulaRiskOp***/proc (1) = rndCopulaRiskOp(mu1,sigma1,lambda1,mu2,sigma2,lambda2,rho,ns);local vartheta1,vartheta2,N1,N2,i,u1,u2,vartheta;vartheta1 = zeros(ns,1);vartheta2 = zeros(ns,1);N1 = rndp(ns,1,lambda1);N2 = rndp(ns,1,lambda2);i = 1;do until i > ns;if N1[i] /= 0;vartheta1[i] = sumc(_rndLN(mu1,sigma1,N1[i],1));endif;if N2[i] /= 0;vartheta2[i] = sumc(_rndLN(mu2,sigma2,N2[i],1));endif;i = i + 1;endo;74