Caderno Institucional do Governo da Sociedade e de ... - EDP

Caderno Institucional do Governo da Sociedade e de ... - EDP

Caderno Institucional do Governo da Sociedade e de ... - EDP

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

RELATÓRIO E CONTAS 2008<br />

CADERNO INSTITUCIONAL, DO GOVERNO<br />

DA SOCIEDADE E DE SUSTENTABILIDADE<br />

NEGÓCIOS DO GRUPO <strong>EDP</strong><br />

2. ENQUADRAMENTO DA ACTIVIDADE<br />

2.1. Enquadramento macro-económico<br />

Ao longo <strong>do</strong> ano <strong>de</strong> 2008 a economia mundial foi<br />

afecta<strong>da</strong> pela interacção <strong>de</strong> choques múltiplos <strong>de</strong>correntes<br />

<strong>do</strong> agravamento dramático <strong>da</strong>s condições financeiras,<br />

<strong>da</strong> ascensão e que<strong>da</strong> <strong>do</strong>s preços <strong>da</strong>s matérias-primas<br />

e <strong>do</strong> ajustamento <strong>de</strong>sor<strong>de</strong>na<strong>do</strong> e súbito <strong>de</strong> <strong>de</strong>sequilíbrios<br />

macroeconómicos mundiais. A quebra <strong>de</strong> activi<strong>da</strong><strong>de</strong> nas<br />

economias <strong>de</strong>senvolvi<strong>da</strong>s apresentou‐se substancial e,<br />

ao contrário <strong>da</strong> expectativa prevalecente no final <strong>de</strong> 2007,<br />

condicionou fortemente o <strong>de</strong>sempenho <strong>da</strong>s economias<br />

em <strong>de</strong>senvolvimento. Esta influência foi particularmente<br />

intensa no último trimestre <strong>do</strong> ano, na sequência <strong>da</strong> forte<br />

instabili<strong>da</strong><strong>de</strong> que se fez sentir nos merca<strong>do</strong>s financeiros,<br />

ten<strong>do</strong>-se reflecti<strong>do</strong> numa quase estagnação <strong>do</strong>s fluxos<br />

<strong>de</strong> comércio e <strong>de</strong> financiamento mundiais. Alguns esta<strong>do</strong>s<br />

europeus e <strong>do</strong> su<strong>de</strong>ste asiático, mais vulneráveis<br />

à reversão <strong>de</strong> fluxos <strong>de</strong> investimento <strong>de</strong> curto prazo,<br />

viram-se na contingência <strong>de</strong> recorrer à aju<strong>da</strong> externa e,<br />

em casos extremos, foram força<strong>do</strong>s a interromper<br />

a convertibili<strong>da</strong><strong>de</strong> <strong>da</strong>s suas moe<strong>da</strong>s e a limitar a liber<strong>da</strong><strong>de</strong><br />

<strong>de</strong> movimentos <strong>de</strong> capitais.<br />

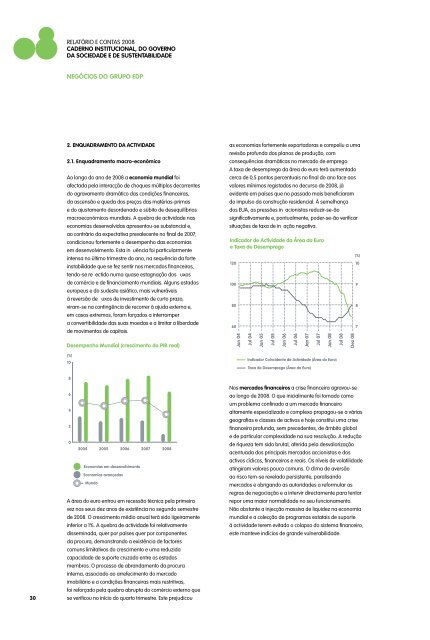

Desempenho Mundial (crescimento <strong>do</strong> PIB real)<br />

(%)<br />

10<br />

as economias fortemente exporta<strong>do</strong>ras e compeliu a uma<br />

revisão profun<strong>da</strong> <strong>do</strong>s planos <strong>de</strong> produção, com<br />

consequências dramáticas no merca<strong>do</strong> <strong>de</strong> emprego.<br />

A taxa <strong>de</strong> <strong>de</strong>semprego <strong>da</strong> área <strong>do</strong> euro terá aumenta<strong>do</strong><br />

cerca <strong>de</strong> 0,5 pontos percentuais no final <strong>do</strong> ano face aos<br />

valores mínimos regista<strong>do</strong>s no <strong>de</strong>curso <strong>de</strong> 2008, já<br />

evi<strong>de</strong>nte em países que no passa<strong>do</strong> mais beneficiaram<br />

<strong>do</strong> impulso <strong>da</strong> construção resi<strong>de</strong>ncial. À semelhança<br />

<strong>do</strong>s EUA, as pressões inflacionistas reduzir‐se-ão<br />

significativamente e, pontualmente, po<strong>de</strong>r‐se-ão verificar<br />

situações <strong>de</strong> taxa <strong>de</strong> inflação negativa.<br />

Indica<strong>do</strong>r <strong>de</strong> Activi<strong>da</strong><strong>de</strong> <strong>da</strong> Área <strong>do</strong> Euro<br />

e Taxa <strong>de</strong> Desemprego<br />

120<br />

100<br />

80<br />

60<br />

Jan 04<br />

Jul 04<br />

Jan 05<br />

Jul 05<br />

Jan 06<br />

Jul 06<br />

Jan 07<br />

Jul 07<br />

Jan 08<br />

Indica<strong>do</strong>r Coinci<strong>de</strong>nte <strong>de</strong> Activi<strong>da</strong><strong>de</strong> (Área <strong>do</strong> Euro)<br />

Taxa <strong>de</strong> Desemprego (Área <strong>do</strong> Euro)<br />

Jul 08<br />

Dez 08<br />

(%)<br />

10<br />

9<br />

8<br />

7<br />

30<br />

8<br />

6<br />

4<br />

2<br />

0<br />

2004 2005 2006 2007 2008<br />

Economias em <strong>de</strong>senvolvimento<br />

Economias avança<strong>da</strong>s<br />

Mun<strong>do</strong><br />

A área <strong>do</strong> euro entrou em recessão técnica pela primeira<br />

vez nos seus <strong>de</strong>z anos <strong>de</strong> existência no segun<strong>do</strong> semestre<br />

<strong>de</strong> 2008. O crescimento médio anual terá si<strong>do</strong> ligeiramente<br />

inferior a 1%. A quebra <strong>de</strong> activi<strong>da</strong><strong>de</strong> foi relativamente<br />

dissemina<strong>da</strong>, quer por países quer por componentes<br />

<strong>da</strong> procura, <strong>de</strong>monstran<strong>do</strong> a existência <strong>de</strong> factores<br />

comuns limitativos <strong>do</strong> crescimento e uma reduzi<strong>da</strong><br />

capaci<strong>da</strong><strong>de</strong> <strong>de</strong> suporte cruza<strong>do</strong> entre os esta<strong>do</strong>s<br />

membros. O processo <strong>de</strong> abran<strong>da</strong>mento <strong>da</strong> procura<br />

interna, associa<strong>do</strong> ao arrefecimento <strong>do</strong> merca<strong>do</strong><br />

imobiliário e a condições financeiras mais restritivas,<br />

foi reforça<strong>do</strong> pela quebra abrupta <strong>do</strong> comércio externo que<br />

se verificou no início <strong>do</strong> quarto trimestre. Este prejudicou<br />

Nos merca<strong>do</strong>s financeiros a crise financeira agravou‐se<br />

ao longo <strong>de</strong> 2008. O que inicialmente foi toma<strong>do</strong> como<br />

um problema confina<strong>do</strong> a um merca<strong>do</strong> financeiro<br />

altamente especializa<strong>do</strong> e complexo propagou-se a várias<br />

geografias e classes <strong>de</strong> activos e hoje constitui uma crise<br />

financeira profun<strong>da</strong>, sem prece<strong>de</strong>ntes, <strong>de</strong> âmbito global<br />

e <strong>de</strong> particular complexi<strong>da</strong><strong>de</strong> na sua resolução. A redução<br />

<strong>de</strong> riqueza tem si<strong>do</strong> brutal, aferi<strong>da</strong> pela <strong>de</strong>svalorização<br />

acentua<strong>da</strong> <strong>do</strong>s principais merca<strong>do</strong>s accionistas e <strong>do</strong>s<br />

activos cíclicos, financeiros e reais. Os níveis <strong>de</strong> volatili<strong>da</strong><strong>de</strong><br />

atingiram valores pouco comuns. O clima <strong>de</strong> aversão<br />

ao risco tem-se revela<strong>do</strong> persistente, paralisan<strong>do</strong><br />

merca<strong>do</strong>s e obrigan<strong>do</strong> as autori<strong>da</strong><strong>de</strong>s a reformular as<br />

regras <strong>de</strong> negociação e a intervir directamente para tentar<br />

repor uma maior normali<strong>da</strong><strong>de</strong> no seu funcionamento.<br />

Não obstante a injecção massiva <strong>de</strong> liqui<strong>de</strong>z na economia<br />

mundial e a colecção <strong>de</strong> programas estatais <strong>de</strong> suporte<br />

à activi<strong>da</strong><strong>de</strong> terem evita<strong>do</strong> o colapso <strong>do</strong> sistema financeiro,<br />

este manteve indícios <strong>de</strong> gran<strong>de</strong> vulnerabili<strong>da</strong><strong>de</strong>.