beyond pt 0 23/1

beyond pt 0 23/1

beyond pt 0 23/1

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Section Three<br />

Information Technology (IT) industries and<br />

e-commerce<br />

Computing power has been<br />

doubling every 18 months for<br />

the past 30 years. At the same<br />

time, the average price of a<br />

transistor has fallen by six<br />

orders of magnitude, due to<br />

microprocessor development.<br />

In just six years (1991 to<br />

1997), the cost of<br />

microprocessor computing<br />

power decreased from $<strong>23</strong>0<br />

to $3.42 per MIPS. No other<br />

manufactured item has<br />

decreased in cost so far,<br />

so fast.<br />

Henry D, Cooke S, Montes, 1998,<br />

The Emerging Digital Economy,<br />

US Department of Commerce 1998<br />

The IT industries are relatively new and dynamic in nature. The<br />

IT industries have a number of unusual characteristics. They are<br />

among the fastest growing industries. Technological change is rapid<br />

and product life cycles are short. Most product and service prices are<br />

falling rather than rising. Convergence in the industries is leading to<br />

the increasing inter-relation and interdependence of computing,<br />

communications and the media. This is also profoundly changing the<br />

structure and dynamics of the IT industries. 12 Change in the<br />

IT industries and their capacity is driving change in the use of<br />

e-commerce while the IT industries are also being driven by changes in<br />

e-commerce usage.<br />

3.1 The IT industries<br />

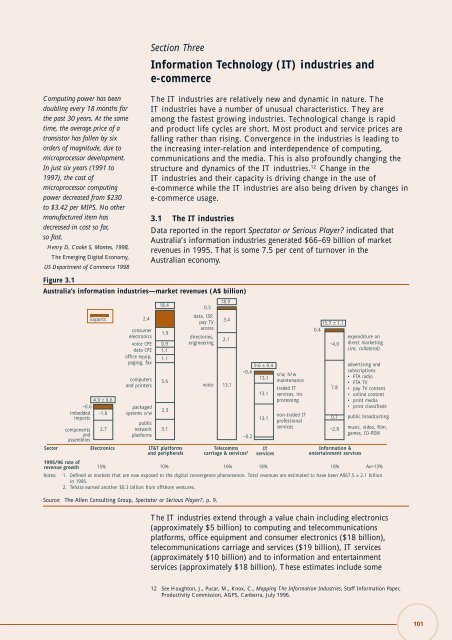

Data reported in the report Spectator or Serious Player? indicated that<br />

Australia’s information industries generated $66–69 billion of market<br />

revenues in 1995. That is some 7.5 per cent of turnover in the<br />

Australian economy.<br />

Figure 3.1<br />

Australia’s information industries—market revenues (A$ billion)<br />

Notes:<br />

4.9 ± 0.6<br />

~0.6<br />

imbedded -1.6<br />

imports<br />

components<br />

and<br />

assemblies<br />

Exports<br />

2.7<br />

public<br />

network<br />

platforms<br />

18.4<br />

voice<br />

Source: The Allen Consulting Group, Spectator or Serious Player?, p. 9.<br />

2.4<br />

consumer<br />

electronics<br />

voice CPE<br />

data CPE<br />

office equip,<br />

paging, fax<br />

computers<br />

and printers<br />

packaged<br />

systems s/w<br />

1.9<br />

0.9<br />

1.1<br />

1.1<br />

Sector Electronics IT&T platforms<br />

and peripherals<br />

5.6<br />

2.3<br />

3.1<br />

0.3<br />

data, ISP,<br />

pay TV<br />

access<br />

directories,<br />

engineering<br />

18.9<br />

3.4<br />

2.1<br />

13.1<br />

9.6 ± 0.4<br />

~0.4<br />

13.1<br />

~0.2<br />

Telecomms<br />

carriage & services 2<br />

13.1<br />

13.1<br />

IT<br />

services<br />

s/w, h/w<br />

maintenance<br />

traded IT<br />

services, inc<br />

processing<br />

non-traded IT<br />

professional<br />

services<br />

15.7 ± 1.1<br />

0.4<br />

1. Defined as markets that are now exposed to the digital convergence phenomenon. Total revenues are estimated to have been A$67.5 ± 2.1 billion<br />

in 1995.<br />

2. Telstra earned another $0.3 billion from offshore ventures.<br />

The IT industries extend through a value chain including electronics<br />

(approximately $5 billion) to computing and telecommunications<br />

platforms, office equipment and consumer electronics ($18 billion),<br />

telecommunications carriage and services ($19 billion), IT services<br />

(approximately $10 billion) and to information and entertainment<br />

services (approximately $18 billion). These estimates include some<br />

~4.0<br />

7.8<br />

0.7<br />

~2.8<br />

Information &<br />

entertainment services<br />

expenditure on<br />

direct marketing<br />

(inc. collateral)<br />

advertising and<br />

subscri<strong>pt</strong>ions<br />

• FTA radio<br />

• FTA TV<br />

• pay TV content<br />

• online content<br />

• print media<br />

• print classifieds<br />

public broadcasting<br />

music, video, film,<br />

games, CD-ROM<br />

1995/96 rate of<br />

revenue growth 15% 10% 16% 18% 10% Av=13%<br />

12 See Houghton, J., Pucar, M., Knox, C., Mapping The Information Industries, Staff Information Paper,<br />

Productivity Commission, AGPS, Canberra, July 1996.<br />

101