beyond pt 0 23/1

beyond pt 0 23/1

beyond pt 0 23/1

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

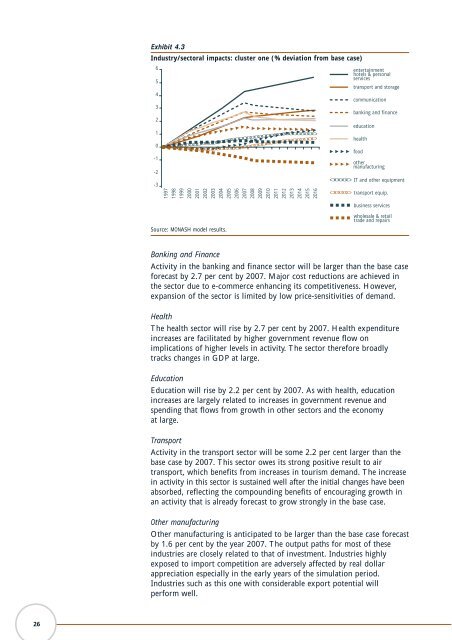

Exhibit 4.3<br />

Industry/sectoral impacts: cluster one (% deviation from base case)<br />

6 entertainment<br />

hotels & personal<br />

services<br />

5<br />

transport and storage<br />

4<br />

communication<br />

3<br />

banking and finance<br />

2<br />

education<br />

1<br />

health<br />

0<br />

food<br />

-1<br />

other<br />

manufacturing<br />

-2<br />

-3<br />

1997<br />

1998<br />

1999<br />

2000<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

2010<br />

2011<br />

2012<br />

2013<br />

2014<br />

2015<br />

2016<br />

IT and other equipment<br />

transport equip.<br />

business services<br />

Source: MONASH model results.<br />

wholesale & retail<br />

trade and repairs<br />

Banking and Finance<br />

Activity in the banking and finance sector will be larger than the base case<br />

forecast by 2.7 per cent by 2007. Major cost reductions are achieved in<br />

the sector due to e-commerce enhancing its competitiveness. However,<br />

expansion of the sector is limited by low price-sensitivities of demand.<br />

Health<br />

The health sector will rise by 2.7 per cent by 2007. Health expenditure<br />

increases are facilitated by higher government revenue flow on<br />

implications of higher levels in activity. The sector therefore broadly<br />

tracks changes in GDP at large.<br />

Education<br />

Education will rise by 2.2 per cent by 2007. As with health, education<br />

increases are largely related to increases in government revenue and<br />

spending that flows from growth in other sectors and the economy<br />

at large.<br />

Transport<br />

Activity in the transport sector will be some 2.2 per cent larger than the<br />

base case by 2007. This sector owes its strong positive result to air<br />

transport, which benefits from increases in tourism demand. The increase<br />

in activity in this sector is sustained well after the initial changes have been<br />

absorbed, reflecting the compounding benefits of encouraging growth in<br />

an activity that is already forecast to grow strongly in the base case.<br />

Other manufacturing<br />

Other manufacturing is anticipated to be larger than the base case forecast<br />

by 1.6 per cent by the year 2007. The output paths for most of these<br />

industries are closely related to that of investment. Industries highly<br />

exposed to import competition are adversely affected by real dollar<br />

appreciation especially in the early years of the simulation period.<br />

Industries such as this one with considerable export potential will<br />

perform well.<br />

26