beyond pt 0 23/1

beyond pt 0 23/1

beyond pt 0 23/1

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

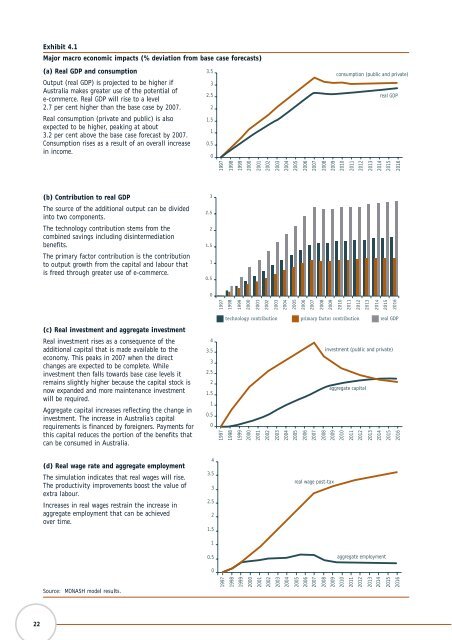

Exhibit 4.1<br />

Major macro economic impacts (% deviation from base case forecasts)<br />

(a) Real GDP and consum<strong>pt</strong>ion<br />

Output (real GDP) is projected to be higher if<br />

Australia makes greater use of the potential of<br />

e-commerce. Real GDP will rise to a level<br />

2.7 per cent higher than the base case by 2007.<br />

Real consum<strong>pt</strong>ion (private and public) is also<br />

expected to be higher, peaking at about<br />

3.2 per cent above the base case forecast by 2007.<br />

Consum<strong>pt</strong>ion rises as a result of an overall increase<br />

in income.<br />

3.5<br />

3<br />

2.5<br />

2<br />

1.5<br />

1<br />

0.5<br />

0<br />

consum<strong>pt</strong>ion (public and private)<br />

real GDP<br />

1997<br />

1998<br />

1999<br />

2000<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

2010<br />

2011<br />

2012<br />

2013<br />

2014<br />

2015<br />

2016<br />

(b) Contribution to real GDP<br />

The source of the additional output can be divided<br />

into two components.<br />

The technology contribution stems from the<br />

combined savings including disintermediation<br />

benefits.<br />

The primary factor contribution is the contribution<br />

to output growth from the capital and labour that<br />

is freed through greater use of e-commerce.<br />

(c) Real investment and aggregate investment<br />

Real investment rises as a consequence of the<br />

additional capital that is made available to the<br />

economy. This peaks in 2007 when the direct<br />

changes are expected to be complete. While<br />

investment then falls towards base case levels it<br />

remains slightly higher because the capital stock is<br />

now expanded and more maintenance investment<br />

will be required.<br />

Aggregate capital increases reflecting the change in<br />

investment. The increase in Australia’s capital<br />

requirements is financed by foreigners. Payments for<br />

this capital reduces the portion of the benefits that<br />

can be consumed in Australia.<br />

4<br />

3.5<br />

3<br />

2.5<br />

2<br />

1.5<br />

1<br />

0.5<br />

0<br />

1997<br />

1998<br />

1999<br />

2000<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

investment (public and private)<br />

aggregate capital<br />

2008<br />

2009<br />

2010<br />

2011<br />

2012<br />

2013<br />

2014<br />

2015<br />

2016<br />

(d) Real wage rate and aggregate employment<br />

The simulation indicates that real wages will rise.<br />

The productivity improvements boost the value of<br />

extra labour.<br />

Increases in real wages restrain the increase in<br />

aggregate employment that can be achieved<br />

over time.<br />

4<br />

3.5<br />

3<br />

2.5<br />

2<br />

1.5<br />

1<br />

real wage post-tax<br />

0.5<br />

aggregate employment<br />

0<br />

Source: MONASH model results.<br />

1997<br />

1998<br />

1999<br />

2000<br />

2001<br />

2002<br />

2003<br />

2004<br />

2005<br />

2006<br />

2007<br />

2008<br />

2009<br />

2010<br />

2011<br />

2012<br />

2013<br />

2014<br />

2015<br />

2016<br />

22