G20 china_web

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Growing the global economy<br />

Negative<br />

or low real<br />

interest rates<br />

have done all<br />

they can<br />

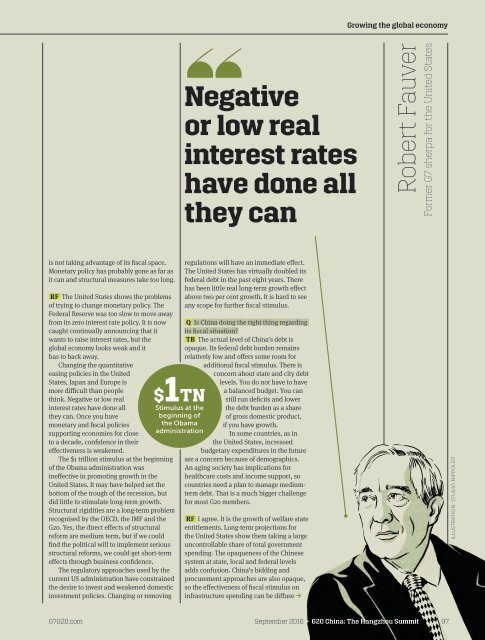

Robert Fauver<br />

Former G7 sherpa for the United States<br />

is not taking advantage of its fiscal space.<br />

Monetary policy has probably gone as far as<br />

it can and structural measures take too long.<br />

RF The United States shows the problems<br />

of trying to change monetary policy. The<br />

Federal Reserve was too slow to move away<br />

from its zero interest rate policy. It is now<br />

caught continually announcing that it<br />

wants to raise interest rates, but the<br />

global economy looks weak and it<br />

has to back away.<br />

Changing the quantitative<br />

easing policies in the United<br />

States, Japan and Europe is<br />

more difficult than people<br />

think. Negative or low real<br />

interest rates have done all<br />

they can. Once you have<br />

monetary and fiscal policies<br />

supporting economies for close<br />

to a decade, confidence in their<br />

effectiveness is weakened.<br />

The $1 trillion stimulus at the beginning<br />

of the Obama administration was<br />

ineffective in promoting growth in the<br />

United States. It may have helped set the<br />

bottom of the trough of the recession, but<br />

did little to stimulate long-term growth.<br />

Structural rigidities are a long-term problem<br />

recognised by the OECD, the IMF and the<br />

<strong>G20</strong>. Yes, the direct effects of structural<br />

reform are medium term, but if we could<br />

find the political will to implement serious<br />

structural reforms, we could get short-term<br />

effects through business confidence.<br />

The regulatory approaches used by the<br />

current US administration have constrained<br />

the desire to invest and weakened domestic<br />

investment policies. Changing or removing<br />

$1TN<br />

Stimulus at the<br />

beginning of<br />

the Obama<br />

administration<br />

regulations will have an immediate effect.<br />

The United States has virtually doubled its<br />

federal debt in the past eight years. There<br />

has been little real long-term growth effect<br />

above two per cent growth. It is hard to see<br />

any scope for further fiscal stimulus.<br />

Q Is China doing the right thing regarding<br />

its fiscal situation?<br />

TB The actual level of China’s debt is<br />

opaque. Its federal debt burden remains<br />

relatively low and offers some room for<br />

additional fiscal stimulus. There is<br />

concern about state and city debt<br />

levels. You do not have to have<br />

a balanced budget. You can<br />

still run deficits and lower<br />

the debt burden as a share<br />

of gross domestic product,<br />

if you have growth.<br />

In some countries, as in<br />

the United States, increased<br />

budgetary expenditures in the future<br />

are a concern because of demographics.<br />

An aging society has implications for<br />

healthcare costs and income support, so<br />

countries need a plan to manage mediumterm<br />

debt. That is a much bigger challenge<br />

for most <strong>G20</strong> members.<br />

RF I agree. It is the growth of welfare state<br />

entitlements. Long-term projections for<br />

the United States show them taking a large<br />

uncontrollable share of total government<br />

spending. The opaqueness of the Chinese<br />

system at state, local and federal levels<br />

adds confusion. China’s bidding and<br />

procurement approaches are also opaque,<br />

so the effectiveness of fiscal stimulus on<br />

infrastructure spending can be diffuse →<br />

ILLUSTRATION: STUDIO NIPPOLDT<br />

G7<strong>G20</strong>.com September 2016 • <strong>G20</strong> China: The Hangzhou Summit 97