El-BAHITH REVIEW Number 03 _ University Of Ouargla Algeria

Annual refereed journal of applied reserch in economic, commercial and managment sciences

Annual refereed journal of applied reserch in economic, commercial and managment sciences

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

______________________________________________________________________________________________________<br />

مجلة الباحث / عدد 2004/<strong>03</strong><br />

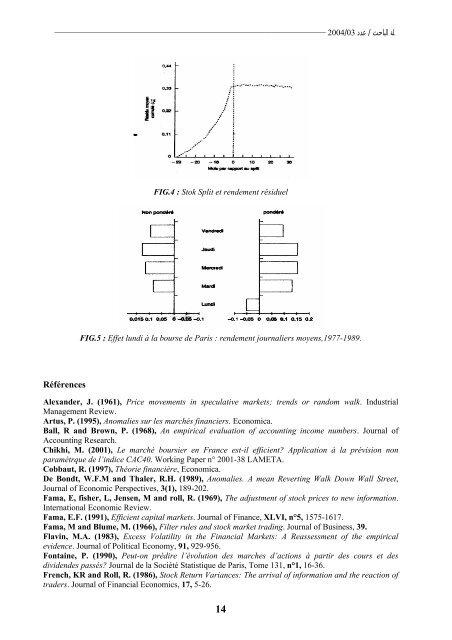

FIG.4 : Stok Split et rendement résiduel<br />

FIG.5 : Effet lundi à la bourse de Paris : rendement journaliers moyens,1977-1989.<br />

Références<br />

Alexander, J. (1961), Price movements in speculative markets; trends or random walk. Industrial<br />

Management Review.<br />

Artus, P. (1995), Anomalies sur les marchés financiers. Economica.<br />

Ball, R and Brown, P. (1968), An empirical evaluation of accounting income numbers. Journal of<br />

Accounting Research.<br />

Chikhi, M. (2001), Le marché boursier en France est-il efficient? Application à la prévision non<br />

paramétrque de l’indice CAC40. Working Paper n° 2001-38 LAMETA.<br />

Cobbaut, R. (1997), Théorie financière, Economica.<br />

De Bondt, W.F.M and Thaler, R.H. (1989), Anomalies. A mean Reverting Walk Down Wall Street,<br />

Journal of Economic Perspectives, 3(1), 189-202.<br />

Fama, E, fisher, L, Jensen, M and roll, R. (1969), The adjustment of stock prices to new information.<br />

International Economic Review.<br />

Fama, E.F. (1991), Efficient capital markets. Journal of Finance, XLVI, n°5, 1575-1617.<br />

Fama, M and Blume, M. (1966), Filter rules and stock market trading. Journal of Business, 39.<br />

Flavin, M.A. (1983), Excess Volatility in the Financial Markets: A Reassessment of the empirical<br />

evidence. Journal of Political Economy, 91, 929-956.<br />

Fontaine, P. (1990), Peut-on prédire l’évolution des marches d’actions à partir des cours et des<br />

dividendes passés? Journal de la Société Statistique de Paris, Tome 131, n°1, 16-36.<br />

French, KR and Roll, R. (1986), Stock Return Variances: The arrival of information and the reaction of<br />

traders. Journal of Financial Economics, 17, 5-26.<br />

14