Conceptos de Administracion Estrategica

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

330 PARTE 3 • IMPLEMENTACIÓN DE LA ESTRATEGIA<br />

14. ¿Hasta qué punto ha estado usted expuesto a temas<br />

ecológicos en sus cursos <strong>de</strong> negocios? ¿Qué curso es<br />

el que ha tenido la mayor cobertura? ¿Qué porcentaje<br />

<strong>de</strong> sus cursos <strong>de</strong> negocios no han tratado esos<br />

temas? Comente.<br />

15. Complete los siguientes análisis EPS/EBIT para una<br />

compañía cuyo precio accionario es <strong>de</strong> $20, su tasa<br />

<strong>de</strong> interés en fondos es <strong>de</strong>l 5%, su tasa fiscal es <strong>de</strong>l<br />

20%, su número <strong>de</strong> acciones en circulación es <strong>de</strong> 500<br />

millones, y su rango <strong>de</strong> EBIT es <strong>de</strong> $100 millones a<br />

$300 millones. La empresa necesita recaudar $200<br />

millones <strong>de</strong> capital. Utilice la tabla que se presenta al<br />

final <strong>de</strong> esta sección para completar el trabajo.<br />

16. ¿En qué condiciones las ganancias retenidas en el<br />

balance general disminuirán <strong>de</strong> un año para el otro?<br />

17. Con sus propias palabras, haga una lista <strong>de</strong> todos los<br />

pasos para el <strong>de</strong>sarrollo <strong>de</strong> estados financieros<br />

proyectados.<br />

18. Con base en los estados financieros <strong>de</strong> Google, ¿cuántos<br />

divi<strong>de</strong>ndos en dólares pagó Google en el año 2004?<br />

19. Con base en los estados financieros <strong>de</strong> Litten Company<br />

presentados en este capítulo, calcule el valor <strong>de</strong><br />

esa compañía, tomando en cuenta que el valor<br />

<strong>de</strong> cada acción es <strong>de</strong> $20 y que tiene un millón <strong>de</strong><br />

acciones en circulación. Calcule cuatro formas<br />

diferentes y promedie.<br />

20. ¿Por qué se <strong>de</strong>bería tener cuidado <strong>de</strong> no utilizar a<br />

ciegas los porcentajes históricos en el <strong>de</strong>sarrollo <strong>de</strong><br />

estados financieros proyectados?<br />

21. En el <strong>de</strong>sarrollo <strong>de</strong> estados financieros proyectados,<br />

¿qué es lo que se <strong>de</strong>be hacer si la cantidad <strong>de</strong> dinero<br />

que se <strong>de</strong>be tener en la cuenta corriente (para hacer<br />

el balance general) es mucho mayor (o menor) <strong>de</strong> lo<br />

esperado?<br />

22. ¿Por qué es importante y necesario segmentar los<br />

mercados y dirigirse a un grupo específico <strong>de</strong><br />

clientes, en vez <strong>de</strong> tratar <strong>de</strong> ven<strong>de</strong>r productos a<br />

todos los posibles consumidores?<br />

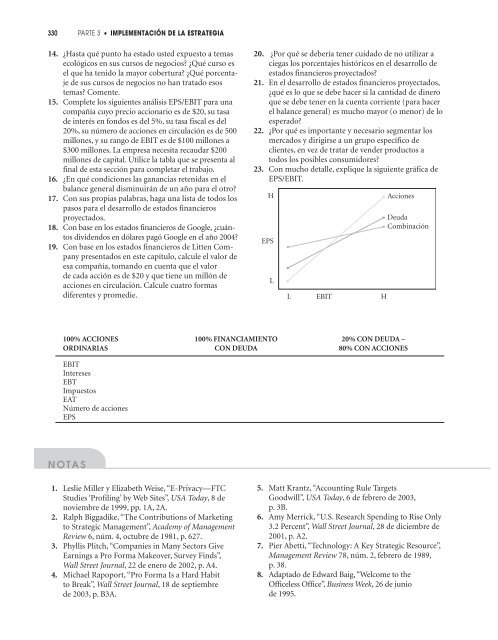

23. Con mucho <strong>de</strong>talle, explique la siguiente gráfica <strong>de</strong><br />

EPS/EBIT.<br />

H<br />

EPS<br />

L<br />

L<br />

EBIT<br />

H<br />

Acciones<br />

Deuda<br />

Combinación<br />

100% ACCIONES 100% FINANCIAMIENTO 20% CON DEUDA –<br />

ORDINARIAS CON DEUDA 80% CON ACCIONES<br />

EBIT<br />

Intereses<br />

EBT<br />

Impuestos<br />

EAT<br />

Número <strong>de</strong> acciones<br />

EPS<br />

NOTAS<br />

1. Leslie Miller y Elizabeth Weise, “E-Privacy—FTC<br />

Studies ‘Profiling’ by Web Sites”, USA Today,8 <strong>de</strong><br />

noviembre <strong>de</strong> 1999, pp. 1A, 2A.<br />

2. Ralph Biggadike, “The Contributions of Marketing<br />

to Strategic Management”, Aca<strong>de</strong>my of Management<br />

Review 6, núm. 4, octubre <strong>de</strong> 1981, p. 627.<br />

3. Phyllis Plitch, “Companies in Many Sectors Give<br />

Earnings a Pro Forma Makeover, Survey Finds”,<br />

Wall Street Journal, 22 <strong>de</strong> enero <strong>de</strong> 2002, p. A4.<br />

4. Michael Rapoport,“Pro Forma Is a Hard Habit<br />

to Break”, Wall Street Journal, 18 <strong>de</strong> septiembre<br />

<strong>de</strong> 2003, p. B3A.<br />

5. Matt Krantz, “Accounting Rule Targets<br />

Goodwill”, USA Today,6 <strong>de</strong> febrero <strong>de</strong> 2003,<br />

p. 3B.<br />

6. Amy Merrick, “U.S. Research Spending to Rise Only<br />

3.2 Percent”, Wall Street Journal, 28 <strong>de</strong> diciembre <strong>de</strong><br />

2001, p. A2.<br />

7. Pier Abetti, “Technology: A Key Strategic Resource”,<br />

Management Review 78, núm. 2, febrero <strong>de</strong> 1989,<br />

p. 38.<br />

8. Adaptado <strong>de</strong> Edward Baig, “Welcome to the<br />

Officeless Office”, Business Week, 26 <strong>de</strong> junio<br />

<strong>de</strong> 1995.