Sustainable Microfinance - Balanced Scorecard's added value for ...

Sustainable Microfinance - Balanced Scorecard's added value for ...

Sustainable Microfinance - Balanced Scorecard's added value for ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

3.3.2 Per<strong>for</strong>mance Management Beyond the Private Sector<br />

According to Kaplan and Norton (2001), the BSC needs some adjustments in order<br />

to fit to the modus operandi of not-<strong>for</strong>-profit organizations, because their main<br />

objectives are not finance-related. They suggest putting the customer at the top of<br />

the strategic map. However, even this small modification could be a complicated one.<br />

Kaplan and Norton (2001, p. 98), argue that ‘in a non-profit organization, donors<br />

provide the financial resources; they pay <strong>for</strong> the service, while another group, the<br />

constituents, receives the service. Who is the customer, the one paying or the one<br />

receiving?’ In order to address this strategic problem, they suggest that:<br />

‘Rather than have to make such a Solomonic decision, organizations place<br />

both the donor perspective and the recipient perspective, in parallel, at the top<br />

of their <strong>Balanced</strong> Scorecards. They develop objectives <strong>for</strong> both donors and<br />

recipients, and then identify the internal processes that deliver desired <strong>value</strong><br />

propositions <strong>for</strong> both groups of ‘customers’’ (Kaplan & Norton, 2001, p. 98).<br />

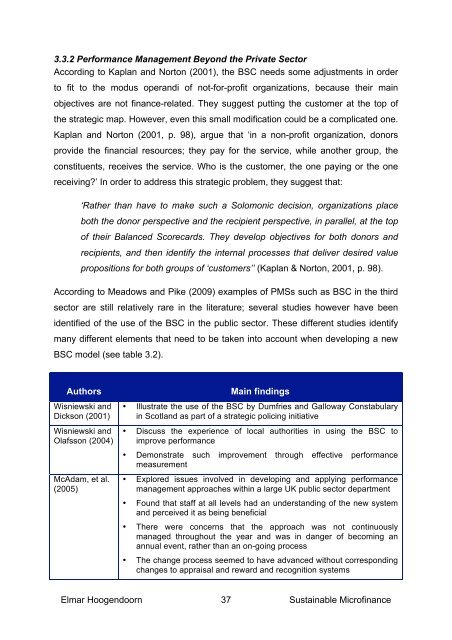

According to Meadows and Pike (2009) examples of PMSs such as BSC in the third<br />

sector are still relatively rare in the literature; several studies however have been<br />

identified of the use of the BSC in the public sector. These different studies identify<br />

many different elements that need to be taken into account when developing a new<br />

BSC model (see table 3.2).<br />

Authors Main findings<br />

Wisniewski and<br />

Dickson (2001)<br />

Wisniewski and<br />

Olafsson (2004)<br />

McAdam, et al.<br />

(2005)<br />

• Illustrate the use of the BSC by Dumfries and Galloway Constabulary<br />

in Scotland as part of a strategic policing initiative<br />

• Discuss the experience of local authorities in using the BSC to<br />

improve per<strong>for</strong>mance<br />

• Demonstrate such improvement through effective per<strong>for</strong>mance<br />

measurement<br />

• Explored issues involved in developing and applying per<strong>for</strong>mance<br />

management approaches within a large UK public sector department<br />

• Found that staff at all levels had an understanding of the new system<br />

and perceived it as being beneficial<br />

• There were concerns that the approach was not continuously<br />

managed throughout the year and was in danger of becoming an<br />

annual event, rather than an on-going process<br />

• The change process seemed to have advanced without corresponding<br />

changes to appraisal and reward and recognition systems<br />

Elmar Hoogendoorn 37<br />

<strong>Sustainable</strong> <strong>Microfinance</strong>

![Joint Report on Social Protection and Social Inclusion [2005]](https://img.yumpu.com/19580638/1/190x132/joint-report-on-social-protection-and-social-inclusion-2005.jpg?quality=85)