Development Plan - City of Playford - SA.Gov.au

Development Plan - City of Playford - SA.Gov.au

Development Plan - City of Playford - SA.Gov.au

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

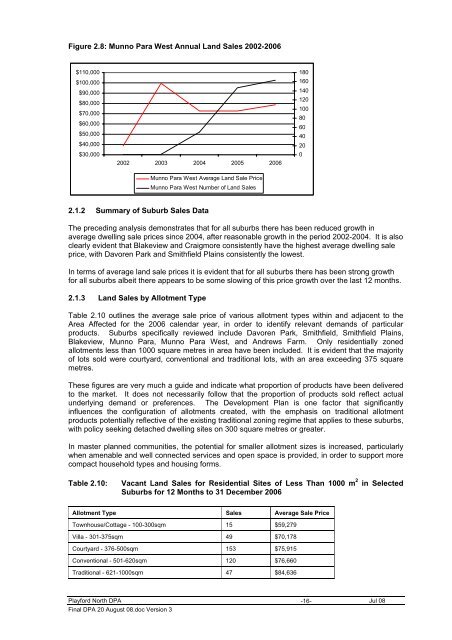

Figure 2.8: Munno Para West Annual Land Sales 2002-2006<br />

$110,000<br />

$100,000<br />

$90,000<br />

$80,000<br />

$70,000<br />

$60,000<br />

$50,000<br />

$40,000<br />

$30,000<br />

2002 2003 2004 2005 2006<br />

Munno Para West Average Land Sale Price<br />

Munno Para West Number <strong>of</strong> Land Sales<br />

180<br />

160<br />

140<br />

120<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

2.1.2 Summary <strong>of</strong> Suburb Sales Data<br />

The preceding analysis demonstrates that for all suburbs there has been reduced growth in<br />

average dwelling sale prices since 2004, after reasonable growth in the period 2002-2004. It is also<br />

clearly evident that Blakeview and Craigmore consistently have the highest average dwelling sale<br />

price, with Davoren Park and Smithfield Plains consistently the lowest.<br />

In terms <strong>of</strong> average land sale prices it is evident that for all suburbs there has been strong growth<br />

for all suburbs albeit there appears to be some slowing <strong>of</strong> this price growth over the last 12 months.<br />

2.1.3 Land Sales by Allotment Type<br />

Table 2.10 outlines the average sale price <strong>of</strong> various allotment types within and adjacent to the<br />

Area Affected for the 2006 calendar year, in order to identify relevant demands <strong>of</strong> particular<br />

products. Suburbs specifically reviewed include Davoren Park, Smithfield, Smithfield Plains,<br />

Blakeview, Munno Para, Munno Para West, and Andrews Farm. Only residentially zoned<br />

allotments less than 1000 square metres in area have been included. It is evident that the majority<br />

<strong>of</strong> lots sold were courtyard, conventional and traditional lots, with an area exceeding 375 square<br />

metres.<br />

These figures are very much a guide and indicate what proportion <strong>of</strong> products have been delivered<br />

to the market. It does not necessarily follow that the proportion <strong>of</strong> products sold reflect actual<br />

underlying demand or preferences. The <strong>Development</strong> <strong>Plan</strong> is one factor that significantly<br />

influences the configuration <strong>of</strong> allotments created, with the emphasis on traditional allotment<br />

products potentially reflective <strong>of</strong> the existing traditional zoning regime that applies to these suburbs,<br />

with policy seeking detached dwelling sites on 300 square metres or greater.<br />

In master planned communities, the potential for smaller allotment sizes is increased, particularly<br />

when amenable and well connected services and open space is provided, in order to support more<br />

compact household types and housing forms.<br />

Table 2.10:<br />

Vacant Land Sales for Residential Sites <strong>of</strong> Less Than 1000 m 2 in Selected<br />

Suburbs for 12 Months to 31 December 2006<br />

Allotment Type Sales Average Sale Price<br />

Townhouse/Cottage - 100-300sqm 15 $59,279<br />

Villa - 301-375sqm 49 $70,178<br />

Courtyard - 376-500sqm 153 $75,915<br />

Conventional - 501-620sqm 120 $76,660<br />

Traditional - 621-1000sqm 47 $84,636<br />

<strong>Playford</strong> North DPA -16-<br />

Jul 08<br />

Final DPA 20 August 08.doc Version 3