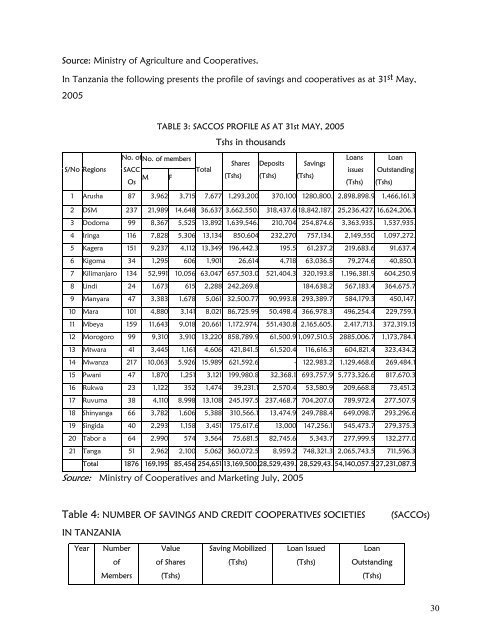

Source: M<strong>in</strong>istry <strong>of</strong> Agriculture and Cooperatives. In Tanzania the follow<strong>in</strong>g presents the pr<strong>of</strong>ile <strong>of</strong> sav<strong>in</strong>gs and cooperatives as at 31st May, 2005 S/No Regions No. <strong>of</strong>No. <strong>of</strong> members SACC M F Os TABLE 3: SACCOS PROFILE AS AT 31st MAY, 2005 Total Tshs <strong>in</strong> thousands Shares (Tshs) Deposits (Tshs) Sav<strong>in</strong>gs (Tshs) Loans issues (Tshs) Loan Outstand<strong>in</strong>g (Tshs) 1 Arusha 87 3,962 3,715 7,677 1,293,200 370,100 1280,800. 2,898,898.9 1,466,161.3 2 DSM 237 21,989 14,648 36,637 3,662,550. 318,437.6 18,842,187. 25,236,427. 16,624,206.1 3 Dodoma 99 8,367 5,525 13,892 1,639,546. 210,704 254,874.6 3,363,935. 1,537,935. 4 Ir<strong>in</strong>ga 116 7,828 5,306 13,134 850,604 232,270 757,134. 2,149,550 1,097,272. 5 Kagera 151 9,237 4,112 13,349 196,442.3 195.5 61,237.2 219,683.6 91,637.4 6 Kigoma 34 1,295 606 1,901 26,614 4,718 63,036.5 79,274.6 40,850.1 7 Kilimanjaro 134 52,991 10,056 63,047 657,503.0 521,404.3 320,193.8 1,196,381.9 604,250.9 8 L<strong>in</strong>di 24 1,673 615 2,288 242,269.8 184,638.2 567,183.4 364,675.7 9 Manyara 47 3,383 1,678 5,061 32,500.77 90,993.8 293,389.7 584,179.3 450,147. 10 Mara 101 4,880 3,141 8,021 86,725.99 50,498.4 366,978.3 496,254.4 229,759.1 11 Mbeya 159 11,643 9,018 20,661 1,172,974. 551,430.8 2,165,605. 2,417,713. 372,319.15 12 Morogoro 99 9,310 3,910 13,220 858,789.9 61,500.9 1,097,510.5 2885,006.7 1,173,784.1 13 Mtwara 41 3,445 1,161 4,606 421,841.5 61,520.4 116,616.3 604,821.4 323,434.2 14 Mwanza 217 10,063 5,926 15,989 621,592.6 - 122,983.2 1,129,468.6 269,484.1 15 Pwani 47 1,870 1,251 3,121 199,980.8 32,368.1 693,757.9 5,773,326.6 817,670.3 16 Rukwa 23 1,122 352 1,474 39,231.1 2,570.4 53,580.9 209,668.8 73,451.2 17 Ruvuma 38 4,110 8,998 13,108 245,197.5 237,468.7 704,207.0 789,972.4 277,507.9 18 Sh<strong>in</strong>yanga 66 3,782 1,606 5,388 310,566.1 13,474.9 249,788.4 649,098.7 293,296.6 19 S<strong>in</strong>gida 40 2,293 1,158 3,451 175,617.6 13,000 147,256.1 545,473.7 279,375.3 20 Tabor a 64 2,990 574 3,564 75,681.5 82,745.6 5,343.7 277,999.9 132,277.0 21 Tanga 51 2,962 2,100 5,062 360,072.5 8,959.2 748,321.3 2,065,743.5 711,596.3 Total 1876 169,195 85,456 254,651 13,169,500.28,529,439. 28,529,43. 54,140,057.5 27,231,087.5 Source: M<strong>in</strong>istry <strong>of</strong> Cooperatives and Market<strong>in</strong>g July, 2005 Table 4: NUMBER OF SAVINGS AND CREDIT COOPERATIVES SOCIETIES (SACCOs) IN TANZANIA Year Number <strong>of</strong> Members Value <strong>of</strong> Shares (Tshs) Sav<strong>in</strong>g Mobilized (Tshs) Loan Issued (Tshs) Loan Outstand<strong>in</strong>g (Tshs) 30

Year Number <strong>of</strong> Members Value <strong>of</strong> Shares (Tshs) Sav<strong>in</strong>g Mobilized (Tshs) Loan Issued (Tshs) Loan Outstand<strong>in</strong>g (Tshs) 1998 769 3,416,287,150 15,110,306,195 2,189,676,458 7,525,734,886 1999 825 5,569,331,623 16,335,545,178 1 3,210,988,463 10,435,176,565 2000 803 5,618,112,584 18,225,778,112 11,524,329,388 13,330,113,198 2001 927 6,610,362,757 20,925,360,250 12,362,207,570 15,903,883,173 2002 987 6,853,113,256 21,533,441,775 12,789,115,620 16,111,987,412 2003 1,700 7,213,114,315 23,427,116,352 20,115,963,119 18,679,568,132 2004 1,760 11,567,507,110 26,345,947,252 30,112,570,630 20,635,446,127 2005 1,875 13,169,502,709 28,529,439,054 54,140,056,528 27,231,087,502 Source: M<strong>in</strong>istry <strong>of</strong> Agriculture and Cooperatives. Table 5: <strong>The</strong> Trend <strong>of</strong> Households Consumption and Disposable Income <strong>in</strong> Tanzania 1961 – 2002 Year Percentage <strong>of</strong> Consumption <strong>of</strong> lowest 20 Percent households Percentage <strong>of</strong> <strong>in</strong>come Received by lowest 20 Percent households Total Normal Household Consumption expenditure. (Mill TZS) Inflation Normal Households Disposable Income (Mill. TZS) Real Consumption Expenditure <strong>of</strong> lowest 20 Percent households (Mill. TZS) Real Private Disposable Income <strong>of</strong> lowest 20 Percent households (Mill. TZS) 1961 1.8 1.1 3617 1.0 3,439.2 65.1 38.2 1962 1.8 1.1 3987 1.1 4,503.2 65.2 45.5 1963 2.5 1.3 4126 1.5 5,367.6 68.3 45.1 1964 2.5 1.7 4785 1.9 5,422.6 63.5 48.9 31

- Page 1 and 2: THE ROLE OF INFORMAL MICROFINANCE I

- Page 3 and 4: DECRALATION I, Mwakajumilo, Stephen

- Page 5 and 6: DEDICATION To Almighty God, to whom

- Page 7 and 8: ACRONYMS AND ABBREVIATIONS AGOA = A

- Page 9 and 10: TABLE OF CONTENTS Title Page I Abst

- Page 11 and 12: 2.2.7 The prospects of SACCOs in Ta

- Page 13 and 14: CHAPTER 4 PRESENTATION AND DATA ANA

- Page 15 and 16: TABLE 18B: Value of loan from SACCO

- Page 17 and 18: To SACCOs, they (SACCOs) are also e

- Page 19 and 20: micro projects, general entrepreneu

- Page 21 and 22: which are viewed as not credit wort

- Page 23 and 24: parts of Tanzania. They are member

- Page 25 and 26: Cooperatives were introduced in Tan

- Page 27 and 28: 1.1.3: WHY IS THIS THESIS UNDERTAKE

- Page 29: Cumulative Number of Number of Year

- Page 33 and 34: Year Percentage of Consumption of l

- Page 35 and 36: • Bureaucratic constraints, lack

- Page 37 and 38: 6. To identify gaps/shortfalls (i.e

- Page 39 and 40: economy with respect to the unhealt

- Page 41 and 42: organizations, help members achieve

- Page 43 and 44: The cooperative formula was then co

- Page 45 and 46: savings and credit cooperatives tha

- Page 47 and 48: Cameroon in its English-speaking ar

- Page 49 and 50: Since they have appeared on the sce

- Page 51 and 52: Tanzania was the first country in A

- Page 53 and 54: Type / Name of institution Microfin

- Page 55 and 56: enhancing loan recovery and improvi

- Page 57 and 58: embarked on building links with Sac

- Page 59 and 60: • Encouraging and supporting, thr

- Page 61 and 62: This shows the true nature of a maj

- Page 63 and 64: Savings mobilization The potential

- Page 65 and 66: It has been argued that the formal

- Page 67 and 68: It is suggested that governments, i

- Page 69 and 70: Local Counterpart Local MF NGOs wor

- Page 71 and 72: Local Counterpart Small Industrial

- Page 73 and 74: Local Counterpart Program Amount Go

- Page 75 and 76: • PROMOTION AND ROLE MODELS. Help

- Page 77 and 78: (iii) The target group being foreig

- Page 79 and 80: (iv) Existence of pressure of the M

- Page 81 and 82:

(c) Government should honor stakeho

- Page 83 and 84:

1.1.16: INCOME DISTRIBUTION Policie

- Page 85 and 86:

TABLE 8: Formal Sector Distribution

- Page 87 and 88:

percent households decreased from a

- Page 89 and 90:

Also the significance of this study

- Page 91 and 92:

loans to their respective members i

- Page 93 and 94:

• Having adequate and timely secr

- Page 95 and 96:

LITERATURE REVIEW 2.1.0: INTRODUCTI

- Page 97 and 98:

It further defines savings and cred

- Page 99 and 100:

from being influenced by individual

- Page 101 and 102:

Investment Guarantee Agency (MIGA)

- Page 103 and 104:

2.1.7: THE ROLE OF STOCK MARKET IN

- Page 105 and 106:

isk{Solnik 1974}. As a consequence

- Page 107 and 108:

• Access for New Firms- The prest

- Page 109 and 110:

of financial systems. The success o

- Page 111 and 112:

Mkwizu (1992) points out that Tanza

- Page 113 and 114:

(1994) conclude that this conservat

- Page 115 and 116:

areas. However, repayment schedules

- Page 117 and 118:

plus services (Aghion and Murdoch 2

- Page 119 and 120:

� Lack of appropriate and adequat

- Page 121 and 122:

savings of the community. Community

- Page 123 and 124:

ingenious entrepreneurs behind them

- Page 125 and 126:

Reforming the national small busine

- Page 127 and 128:

linkages based on both market and n

- Page 129 and 130:

combinations: private sector, gover

- Page 131 and 132:

Tanzania and most of its neighborin

- Page 133 and 134:

favorable rates and help keep finan

- Page 135 and 136:

The SACCOs, is a complex organizati

- Page 137 and 138:

2.2.10.1: Advantages for the SACCOs

- Page 139 and 140:

2.2.10.3 THE COMPARATIVE ANALYSIS B

- Page 141 and 142:

2. The importance of savings in the

- Page 143 and 144:

Commercial Banks are like the other

- Page 145 and 146:

presence in carrying on the traditi

- Page 147 and 148:

A summary profile of selected NGOs

- Page 149 and 150:

(ii) Competitive Financial Environm

- Page 151 and 152:

� Likewise, these institutions wi

- Page 153 and 154:

METHODOLOGY OF THE STUDY CHAPTER TH

- Page 155 and 156:

among variables such as the support

- Page 157 and 158:

• Checklist response • Rating a

- Page 159 and 160:

• What are the roles of instituti

- Page 161 and 162:

In each Region, a total of 20 SACCO

- Page 163 and 164:

3.1.8: Data Processing The data res

- Page 165 and 166:

3.1.12: Limitations • Difficult i

- Page 167 and 168:

Those students who are to write a M

- Page 169 and 170:

V. Generalizations and interpretati

- Page 171 and 172:

The method of collecting Primary an

- Page 173 and 174:

characteristics of participants, th

- Page 175 and 176:

How? Through experiment approach /g

- Page 177 and 178:

which the problem has got to be stu

- Page 179 and 180:

4.1.2: Responses to Questionnaire.

- Page 181 and 182:

Outreach and Savings Mobilization

- Page 183 and 184:

iggest commercial city have more SA

- Page 185 and 186:

small farmers are most likely to sa

- Page 187 and 188:

15 TPB … 16 TGT … 17 IFAD-Mbeya

- Page 189 and 190:

and bank balances which have been o

- Page 191 and 192:

However, operating income per total

- Page 193 and 194:

The Research Institutions in Tanzan

- Page 195 and 196:

microfinance services in both rural

- Page 197 and 198:

(xi) Do you inform SACCOs about you

- Page 199 and 200:

• Provide modern facilities and i

- Page 201 and 202:

validate this observation by asking

- Page 203 and 204:

fact that their SACCOs serves all k

- Page 205 and 206:

What is more disturbing than the fa

- Page 207 and 208:

Year Real Private Disposable income

- Page 209 and 210:

Year Real Private Income Received b

- Page 211 and 212:

Model R R Squar e Adjusted R Square

- Page 213 and 214:

213

- Page 215 and 216:

215

- Page 217 and 218:

CONCLUSION The performance of micro

- Page 219 and 220:

5.14 Please list in the other impor

- Page 221 and 222:

Bank and other institutions engagin

- Page 223 and 224:

Table 18A: SITUATION FOR THE SACCOs

- Page 225 and 226:

Table 19: SITUATION FOR THE AUDITED

- Page 227 and 228:

(a) Specific Recommendations. The r

- Page 229 and 230:

APPENDIX E: QUESTIONNAIRES USED TO

- Page 231 and 232:

5.15 How have you been financing th

- Page 233 and 234:

Real Pinco RGD Rate Real GV Inv Dum

- Page 235 and 236:

In general, SACCOs in Tanzania have

- Page 237 and 238:

Finally, governments in Sub-Saharan

- Page 239 and 240:

5.3.11 If the answer to 10.0 is “

- Page 241 and 242:

5.3: RECOMMENDATIONS OF THE STUDY (

- Page 243 and 244:

REFERENCES: Ally M.Kimario, Marketi

- Page 245:

Working paper number 466, IDS, Univ