- Page 1 and 2:

State of south african cities Repor

- Page 4 and 5:

The cities covered in the SoCR Limp

- Page 6 and 7:

FOREWORD by the Chairperson of the

- Page 8 and 9:

Buffalo city ekurhuleni ethekwini J

- Page 10 and 11:

Overview: State of South African Ci

- Page 12 and 13:

CH3 PRODUCTIVE CITIES Spatial trans

- Page 15 and 16:

INTRODUCTION Our cities: status quo

- Page 17 and 18:

State of Cities Reporting Over the

- Page 19 and 20:

Figure 1.2 shows the projected grow

- Page 21 and 22:

The consequence of this rapid urban

- Page 23 and 24:

LEARNING ACROSS BRICS: from city-re

- Page 25 and 26:

Addressing these challenges require

- Page 27 and 28:

TRANSFORMING OUR WORLD: THE 2030 AG

- Page 29 and 30:

Key issues for South African cities

- Page 31 and 32:

! ! ! ! ! ! ! ! ! ! ! ! Cities and

- Page 33 and 34:

Figure 1.8: Population change total

- Page 35 and 36:

Figure 1.10 shows that, while popul

- Page 37 and 38:

Significant densification through b

- Page 39 and 40:

Increased densities and demand have

- Page 41 and 42:

Global networks versus domestic res

- Page 43:

Informed by five years of research

- Page 46 and 47:

Key Messages 1 2 3 4 5 Spatial tran

- Page 48 and 49:

In cities, economic and social ineq

- Page 50 and 51:

Undesirable current spatial configu

- Page 52 and 53:

neighbouring municipalities are not

- Page 54 and 55:

! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! ! !

- Page 56 and 57:

Built environment investments not s

- Page 58 and 59:

The cost of fragmentation In additi

- Page 60 and 61:

associated land uses benefit all, n

- Page 62 and 63:

Local government is best placed to

- Page 64 and 65:

Competing land interests need to be

- Page 66 and 67:

PRE-1994 building POLICY 1994-2003

- Page 68 and 69:

The 2011 State of South African Cit

- Page 70 and 71:

The most recent National Household

- Page 72 and 73:

Figure 2.6: Alternate transport-urb

- Page 74 and 75:

SPATIAL TRANSFORMATION: Tracking tr

- Page 76 and 77:

Spatial transformation needs respon

- Page 78 and 79:

What is Required to Transform South

- Page 80 and 81:

Transformation of management and ca

- Page 83 and 84:

PRODUCTIVE CITIES Spatial transform

- Page 85 and 86:

Introduction South Africa is headin

- Page 87 and 88:

Congestion and pressure on resource

- Page 89 and 90:

transportation networks. Land-use p

- Page 91 and 92:

strategies in separate silos, with

- Page 93 and 94:

The Economic Role and Performance o

- Page 95 and 96:

• Johannesburg is South Africa’

- Page 97 and 98:

Nevertheless, recent economic fores

- Page 99 and 100:

• In the last five years, Tshwane

- Page 101 and 102:

Figure 3.7 shows the average labour

- Page 103 and 104:

Over the last 10 years, at a sector

- Page 105 and 106:

There is a marked correlation betwe

- Page 107 and 108:

Figure 3.13: Estimated city share o

- Page 109 and 110:

Figure 3.15: City gross fixed-capit

- Page 111 and 112:

development role set out in the 199

- Page 113 and 114:

Table 3.3: Key economic development

- Page 115 and 116:

• eThekwini has an active economi

- Page 117 and 118:

Both types of township are low-inco

- Page 119 and 120:

Informal economy and self-employmen

- Page 121 and 122:

South Africa’s Expanded Public Wo

- Page 123:

PRODUCTIVE CITIES 123 3

- Page 126 and 127:

Key Messages 1 2 3 4 5 6 Cities sti

- Page 128 and 129:

Andile’s story This is based on a

- Page 130 and 131:

of that ward participate in making

- Page 132 and 133:

Cape Town metro Mangaung Mamre Pell

- Page 134 and 135:

These service delivery gains have c

- Page 136 and 137:

YOUTH STUDY: Youth potential and vu

- Page 138 and 139:

However, when the NWAC is superimpo

- Page 140 and 141:

Tshwane, Figure 4.7: Johannesburg C

- Page 142 and 143:

As mentioned, urban integration is

- Page 144 and 145:

Table 4.2: Change in lowest income

- Page 146 and 147:

Ethekwini metro Northdale Hambanath

- Page 148 and 149:

Urban safety South Africa’s citie

- Page 150 and 151:

City’s unemployment rate is about

- Page 152 and 153:

Collective violence 7 Two main dime

- Page 154 and 155:

Towards More Inclusive Cities Citiz

- Page 156 and 157:

Furthermore, citizen education and

- Page 158 and 159:

South Africa requires a spatial pol

- Page 161 and 162:

SUSTAINABLE CITIES Leveraging the t

- Page 163 and 164:

Introduction Since 1994, the govern

- Page 165 and 166:

will need to have low-emissions gro

- Page 167 and 168:

Most of South Africa’s energy con

- Page 169 and 170:

Figure 5.3: Average baseline energy

- Page 171 and 172:

• Tshwane initiated its A Re Yeng

- Page 173 and 174:

WASTE: legislation, policies and pl

- Page 175 and 176:

500 0 400 200 0 2011 2013 2015 2017

- Page 177 and 178:

facility (i.e. waste is sorted manu

- Page 179 and 180:

Figure 5.10: Depiction of in- and o

- Page 181 and 182:

As Figure 5.12 shows, Cape Town and

- Page 183 and 184:

Accelerating the transition to sust

- Page 185 and 186:

disadvantaged groups, through facil

- Page 187 and 188:

Accelerating the transition to food

- Page 189 and 190:

Biodiversity South Africa is the th

- Page 191 and 192:

Open spaces Ecological and social o

- Page 193 and 194:

in the city and in their homes then

- Page 195 and 196:

Emissions reduction to mitigate cli

- Page 197 and 198:

Principles of a Sustainable City Ur

- Page 199:

Recommendations Develop and embed a

- Page 202 and 203:

Key Messages 1 2 3 4 5 Cities have

- Page 204 and 205:

informal political and social cultu

- Page 206 and 207:

Section 51 of the Municipal Systems

- Page 208 and 209:

While these dynamics are critical a

- Page 210 and 211:

Blurred intergovernmental responsib

- Page 212 and 213: Access to information As many ward

- Page 214 and 215: Figure 6.5: Turnout for national an

- Page 216 and 217: COMMUNITY-BASED PLANNING: Strengthe

- Page 218 and 219: The right people are not necessaril

- Page 220 and 221: Local government will require new k

- Page 222 and 223: All the cities have performance man

- Page 224 and 225: Unethical behaviour is one of the r

- Page 226 and 227: Figure 6.9: Municipal audit consist

- Page 228 and 229: Service Delivery and Development As

- Page 230 and 231: Still playing catch-up on basic ser

- Page 232 and 233: knew anything about the city’s ID

- Page 234 and 235: The established routines need to ch

- Page 237 and 238: FINANCE and INNOVATION Sustainable

- Page 239 and 240: Introduction With total expenditure

- Page 241 and 242: In 2013/14, unauthorised, irregular

- Page 243 and 244: Figure 7.2: Nelson Mandela Bay Muni

- Page 245 and 246: The challenge is that the interface

- Page 247 and 248: Phase 3: City autonomy and accounta

- Page 249 and 250: National Treasury uses Uniform Fina

- Page 251 and 252: As Figures 7.5 and 7.6 show, Johann

- Page 253 and 254: In the case of property development

- Page 255 and 256: distribution. Johannesburg’s capi

- Page 257 and 258: • Despite this, the overwhelming

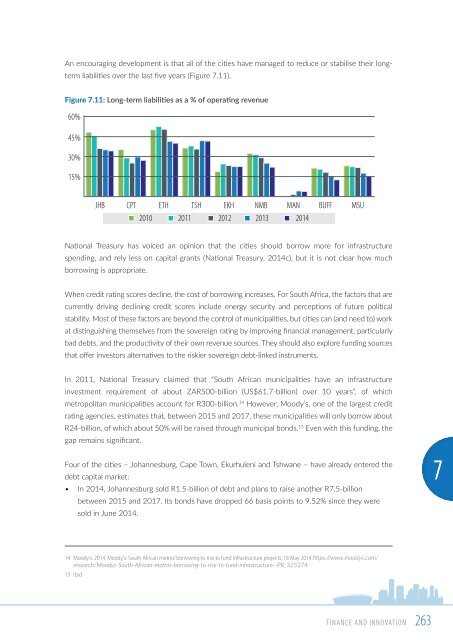

- Page 259 and 260: Effectiveness of spending and servi

- Page 261: cities have low capital expenditure

- Page 265 and 266: 3. Political interventions • Some

- Page 267 and 268: Smart city strategies Smart city st

- Page 269 and 270: encourage non-compliance. If priced

- Page 271 and 272: • Municipalities could rightfully

- Page 273 and 274: Recommendations If spatial transfor

- Page 275: Finance and Innovation 275 7

- Page 278 and 279: Key Messages 1 2 3 4 5 A Call to Ac

- Page 280 and 281: 1. The Spatial Transformation chapt

- Page 282 and 283: Statements of intent in the SOCR St

- Page 284 and 285: WARWICK TRIANGLE: A fragile public-

- Page 286 and 287: Arguably, the primary constraint pr

- Page 288 and 289: Figure 8.1: The quadruple helix - t

- Page 290 and 291: • Completing the National Framewo

- Page 292 and 293: development agency) that took place

- Page 294 and 295: MILE’s strategic objectives are:

- Page 296 and 297: Public participation should be the

- Page 298 and 299: The implementation of CBP through t

- Page 300 and 301: According to Cloete (2015) a partne

- Page 302 and 303: The chapters in this State of Citie

- Page 304 and 305: Overall Recommendations Urban space

- Page 306 and 307: Ensuring city transformation throug

- Page 308 and 309: Roadmap to the city dashboards All

- Page 311 and 312: Buffalo City @refinedrevolt

- Page 313 and 314:

CITY FINANCE economy Municipal reve

- Page 315 and 316:

Overview of flagship programme The

- Page 317:

Reflections While the development o

- Page 320 and 321:

People and Households Size of city

- Page 322 and 323:

Design Capital Introduction Cities

- Page 324 and 325:

Manenberg Contact centre Source: P.

- Page 327 and 328:

City of Ekurhuleni @moography

- Page 329 and 330:

100% 80% 60% 40% 20% 0% CITY FINANC

- Page 331 and 332:

Overview of flagship programme Situ

- Page 333:

the corporate structure and governa

- Page 336 and 337:

People and Households Size of city

- Page 338 and 339:

Go!Durban Introduction Integrated p

- Page 340 and 341:

Go!Durban will include new railways

- Page 343 and 344:

City of JOHANNESBURG @jayjay_gregor

- Page 345 and 346:

100% 80% 60% 40% 20% 0% CITY FINANC

- Page 347 and 348:

Overview of flagship programme The

- Page 349:

However, the success of the Corrido

- Page 352 and 353:

People and Households Size of city

- Page 354 and 355:

Naval Hill Introduction Heritage is

- Page 356 and 357:

In December 2012, the redevelopment

- Page 359 and 360:

Msunduzi @natesvw

- Page 361 and 362:

100% 80% 60% 40% 20% CITY FINANCE e

- Page 363 and 364:

important tourist sites, there have

- Page 365:

In addition, the PURP includes the

- Page 368 and 369:

People and Households Size of city

- Page 370 and 371:

Safety and Peace through Urban Upgr

- Page 372 and 373:

A number of other projects have tak

- Page 375 and 376:

City of Tshwane @drae_savvides

- Page 377 and 378:

100% 80% 60% 40% 20% 0% CITY FINANC

- Page 379 and 380:

Wi-Fi is a significant enabler that

- Page 381:

The coverage map below shows the pl

- Page 384 and 385:

Introduction A key part of the deve

- Page 386 and 387:

These indicators were evaluated on

- Page 388 and 389:

SCODA is a partnership between citi

- Page 390 and 391:

Indicator PRODUCTIVE CITIES Definit

- Page 392 and 393:

Indicator SUSTAINABLE CITIES Defini

- Page 394 and 395:

2016 State of Cities Report Spatial

- Page 396 and 397:

Acronyms ACSA Airports Company Sout

- Page 398 and 399:

FIGURES Figure 1.1 State of South A

- Page 400 and 401:

. . . Figure 6.7 Percentage of seni

- Page 402 and 403:

References for Chapter 1 AfDB (Afri

- Page 404 and 405:

FFC (Financial Fiscal Commission).

- Page 406 and 407:

Cameron B. 2009. Integrated Rapid P

- Page 408 and 409:

References for Chapter 4 Balbo M. a

- Page 410 and 411:

Venter C and Cross C. 2014. Access

- Page 412 and 413:

DPME (Department of Planning and Mo

- Page 414 and 415:

National Treasury. 2006. Local Gove

- Page 416:

Tel: + 27 11 407 6471 • Fax: + 27