pdf (22.8 MB) - METRO Group

pdf (22.8 MB) - METRO Group

pdf (22.8 MB) - METRO Group

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>METRO</strong> gROUP : ANNUAL REPORT 2011 : BUsiNEss<br />

→ noTes : oTHeR noTes<br />

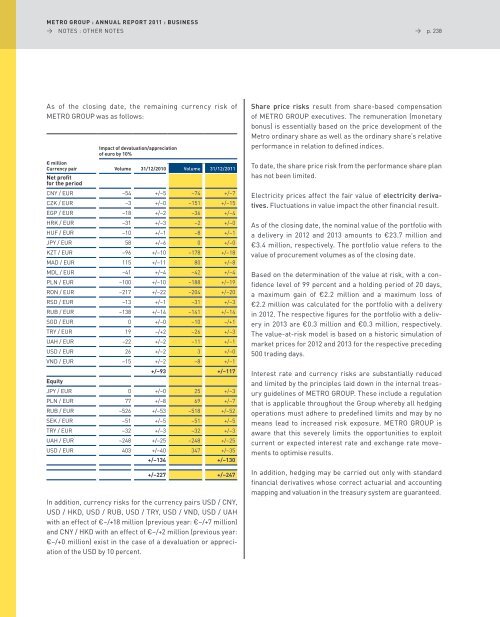

as of the closing date, the remaining currency risk of<br />

MeTRo GRoUp was as follows:<br />

impact of devaluation/appreciation<br />

of euro by 10%<br />

€ million<br />

Currency pair<br />

Net profit<br />

for the period<br />

Volume 31/12/2010 Volume 31/12/2011<br />

CnY / eUR –54 +/–5 –74 +/–7<br />

CZK / eUR –3 +/–0 –151 +/–15<br />

eGp / eUR –18 +/–2 –36 +/–4<br />

HRK / eUR –31 +/–3 –2 +/–0<br />

HUF / eUR –10 +/–1 –8 +/–1<br />

JpY / eUR 58 +/–6 0 +/–0<br />

KZT / eUR –96 +/–10 –178 +/–18<br />

MaD / eUR 115 +/–11 80 +/–8<br />

MDl / eUR –41 +/–4 –42 +/–4<br />

pln / eUR –100 +/–10 –188 +/–19<br />

Ron / eUR –217 +/–22 –204 +/–20<br />

RsD / eUR –13 +/–1 –31 +/–3<br />

RUB / eUR –138 +/–14 –141 +/–14<br />

sGD / eUR 0 +/–0 –10 –/+1<br />

TRY / eUR 19 –/+2 –26 +/–3<br />

UaH / eUR –22 +/–2 –11 +/–1<br />

UsD / eUR 26 +/–2 3 +/–0<br />

vnD / eUR –15 +/–2 –8 +/–1<br />

Equity<br />

+/–93 +/–117<br />

JpY / eUR 0 +/–0 25 +/–3<br />

pln / eUR 77 +/–8 69 +/–7<br />

RUB / eUR –526 +/–53 –518 +/–52<br />

seK / eUR –51 +/–5 –51 +/–5<br />

TRY / eUR –32 +/–3 –32 +/–3<br />

UaH / eUR –248 +/–25 –248 +/–25<br />

UsD / eUR 403 +/–40 347 +/–35<br />

+/–134 +/–130<br />

+/–227 +/–247<br />

In addition, currency risks for the currency pairs UsD / CnY,<br />

UsD / HKD, UsD / RUB, UsD / TRY, UsD / vnD, UsD / UaH<br />

with an effect of €–/+18 million (previous year: €–/+7 million)<br />

and CnY / HKD with an effect of €–/+2 million (previous year:<br />

€–/+0 million) exist in the case of a devaluation or appreciation<br />

of the UsD by 10 percent.<br />

→ p. 238<br />

Share price risks result from share-based compensation<br />

of MeTRo GRoUp executives. The remuneration (monetary<br />

bonus) is essentially based on the price development of the<br />

Metro ordinary share as well as the ordinary share’s relative<br />

performance in relation to defined indices.<br />

To date, the share price risk from the performance share plan<br />

has not been limited.<br />

electricity prices affect the fair value of electricity derivatives.<br />

Fluctuations in value impact the other financial result.<br />

as of the closing date, the nominal value of the portfolio with<br />

a delivery in 2012 and 2013 amounts to €23.7 million and<br />

€3.4 million, respectively. The portfolio value refers to the<br />

value of procurement volumes as of the closing date.<br />

Based on the determination of the value at risk, with a confidence<br />

level of 99 percent and a holding period of 20 days,<br />

a maximum gain of €2.2 million and a maximum loss of<br />

€2.2 million was calculated for the portfolio with a delivery<br />

in 2012. The respective figures for the portfolio with a delivery<br />

in 2013 are €0.3 million and €0.3 million, respectively.<br />

The value-at-risk model is based on a historic simulation of<br />

market prices for 2012 and 2013 for the respective preceding<br />

500 trading days.<br />

Interest rate and currency risks are substantially reduced<br />

and limited by the principles laid down in the internal treasury<br />

guidelines of MeTRo GRoUp. These include a regulation<br />

that is applicable throughout the <strong>Group</strong> whereby all hedging<br />

operations must adhere to predefined limits and may by no<br />

means lead to increased risk exposure. MeTRo GRoUp is<br />

aware that this severely limits the opportunities to exploit<br />

current or expected interest rate and exchange rate movements<br />

to optimise results.<br />

In addition, hedging may be carried out only with standard<br />

financial derivatives whose correct actuarial and accounting<br />

mapping and valuation in the treasury system are guaranteed.