pdf (22.8 MB) - METRO Group

pdf (22.8 MB) - METRO Group

pdf (22.8 MB) - METRO Group

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>METRO</strong> gROUP : ANNUAL REPORT 2011 : BUsiNEss<br />

→ noTes : oTHeR noTes<br />

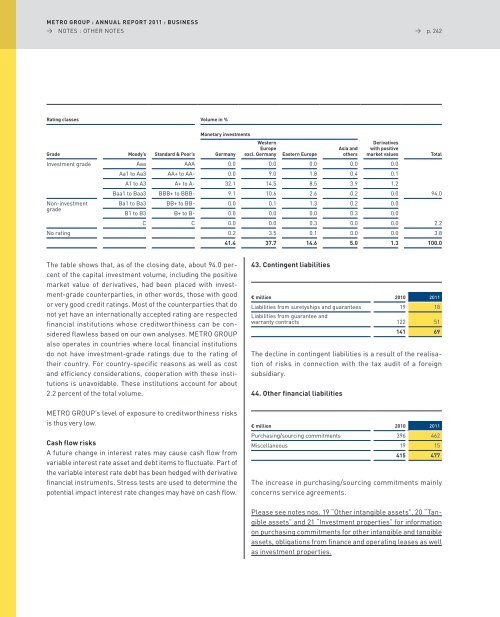

Rating classes Volume in %<br />

Monetary investments<br />

grade Moody’s standard & Poor’s germany<br />

western<br />

Europe<br />

excl. germany Eastern Europe<br />

The table shows that, as of the closing date, about 94.0 percent<br />

of the capital investment volume, including the positive<br />

market value of derivatives, had been placed with investment-grade<br />

counterparties, in other words, those with good<br />

or very good credit ratings. Most of the counterparties that do<br />

not yet have an internationally accepted rating are respected<br />

financial institutions whose creditworthiness can be considered<br />

flawless based on our own analyses. MeTRo GRoUp<br />

also operates in countries where local financial institutions<br />

do not have investment-grade ratings due to the rating of<br />

their country. For country-specific reasons as well as cost<br />

and efficiency considerations, cooperation with these institutions<br />

is unavoidable. These institutions account for about<br />

2.2 percent of the total volume.<br />

MeTRo GRoUp’s level of exposure to creditworthiness risks<br />

is thus very low.<br />

Cash flow risks<br />

a future change in interest rates may cause cash flow from<br />

variable interest rate asset and debt items to fluctuate. part of<br />

the variable interest rate debt has been hedged with deriva tive<br />

financial instruments. stress tests are used to determine the<br />

potential impact interest rate changes may have on cash flow.<br />

43. Contingent liabilities<br />

→ p. 242<br />

€ million 2010 2011<br />

liabilities from suretyships and guarantees<br />

liabilities from guarantee and<br />

19 18<br />

warranty contracts 122 51<br />

141 69<br />

The decline in contingent liabilities is a result of the realisation<br />

of risks in connection with the tax audit of a foreign<br />

subsidiary.<br />

44. Other financial liabilities<br />

Asia and<br />

others<br />

Derivatives<br />

with positive<br />

market values Total<br />

Investment grade aaa aaa 0.0 0.0 0.0 0.0 0.0<br />

aa1 to aa3 aa+ to aa- 0.0 9.0 1.8 0.4 0.1<br />

a1 to a3 a+ to a- 32.1 14.5 8.5 3.9 1.2<br />

Baa1 to Baa3 BBB+ to BBB- 9.1 10.6 2.6 0.2 0.0<br />

94.0<br />

non-investment<br />

Ba1 to Ba3 BB+ to BB- 0.0 0.1 1.3 0.2 0.0<br />

grade<br />

B1 to B3 B+ to B- 0.0 0.0 0.0 0.3 0.0<br />

C C 0.0 0.0 0.3 0.0 0.0<br />

2.2<br />

no rating 0.2 3.5 0.1 0.0 0.0 3.8<br />

41.4 37.7 14.6 5.0 1.3 100.0<br />

€ million 2010 2011<br />

purchasing/sourcing commitments 396 462<br />

Miscellaneous 19 15<br />

415 477<br />

The increase in purchasing/sourcing commitments mainly<br />

concerns service agreements.<br />

please see notes nos. 19 “other intangible assets”, 20 “Tangible<br />

assets” and 21 “Investment properties” for information<br />

on purchasing commitments for other intangible and tangible<br />

assets, obligations from finance and operating leases as well<br />

as investment properties.