Processus de Lévy en Finance - Laboratoire de Probabilités et ...

Processus de Lévy en Finance - Laboratoire de Probabilités et ...

Processus de Lévy en Finance - Laboratoire de Probabilités et ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

172 CHAPTER 5. APPLICATIONS OF LEVY COPULAS<br />

2.5<br />

2.5<br />

2<br />

2<br />

1.5<br />

1.5<br />

1<br />

1<br />

0.5<br />

0.5<br />

0<br />

0<br />

−0.5<br />

−0.5<br />

−1<br />

−1<br />

−1.5<br />

−1.5<br />

−2<br />

−2<br />

−2.5<br />

−2.5 −2 −1.5 −1 −0.5 0 0.5 1 1.5 2 2.5<br />

2.5<br />

−2.5<br />

−2.5 −2 −1.5 −1 −0.5 0 0.5 1 1.5 2 2.5<br />

2.5<br />

2<br />

2<br />

1.5<br />

1.5<br />

1<br />

1<br />

0.5<br />

0.5<br />

0<br />

0<br />

−0.5<br />

−0.5<br />

−1<br />

−1<br />

−1.5<br />

−1.5<br />

−2<br />

−2<br />

−2.5<br />

−2.5 −2 −1.5 −1 −0.5 0 0.5 1 1.5 2 2.5<br />

−2.5<br />

−2.5 −2 −1.5 −1 −0.5 0 0.5 1 1.5 2 2.5<br />

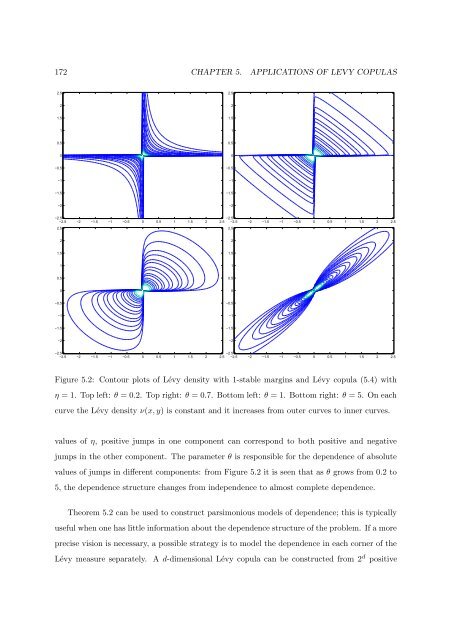

Figure 5.2: Contour plots of Lévy <strong>de</strong>nsity with 1-stable margins and Lévy copula (5.4) with<br />

η = 1. Top left: θ = 0.2. Top right: θ = 0.7. Bottom left: θ = 1. Bottom right: θ = 5. On each<br />

curve the Lévy <strong>de</strong>nsity ν(x, y) is constant and it increases from outer curves to inner curves.<br />

values of η, positive jumps in one compon<strong>en</strong>t can correspond to both positive and negative<br />

jumps in the other compon<strong>en</strong>t. The param<strong>et</strong>er θ is responsible for the <strong>de</strong>p<strong>en</strong><strong>de</strong>nce of absolute<br />

values of jumps in differ<strong>en</strong>t compon<strong>en</strong>ts: from Figure 5.2 it is se<strong>en</strong> that as θ grows from 0.2 to<br />

5, the <strong>de</strong>p<strong>en</strong><strong>de</strong>nce structure changes from in<strong>de</strong>p<strong>en</strong><strong>de</strong>nce to almost compl<strong>et</strong>e <strong>de</strong>p<strong>en</strong><strong>de</strong>nce.<br />

Theorem 5.2 can be used to construct parsimonious mo<strong>de</strong>ls of <strong>de</strong>p<strong>en</strong><strong>de</strong>nce; this is typically<br />

useful wh<strong>en</strong> one has little information about the <strong>de</strong>p<strong>en</strong><strong>de</strong>nce structure of the problem. If a more<br />

precise vision is necessary, a possible strategy is to mo<strong>de</strong>l the <strong>de</strong>p<strong>en</strong><strong>de</strong>nce in each corner of the<br />

Lévy measure separately. A d-dim<strong>en</strong>sional Lévy copula can be constructed from 2 d positive