Processus de Lévy en Finance - Laboratoire de Probabilités et ...

Processus de Lévy en Finance - Laboratoire de Probabilités et ...

Processus de Lévy en Finance - Laboratoire de Probabilités et ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

5.2. SIMULATION OF DEPENDENT LEVY PROCESSES 181<br />

8<br />

1<br />

7<br />

0.5<br />

6<br />

0<br />

5<br />

−0.5<br />

4<br />

−1<br />

3<br />

−1.5<br />

2<br />

−2<br />

1<br />

−2.5<br />

0<br />

−3<br />

−1<br />

−3.5<br />

−2<br />

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1<br />

−4<br />

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1<br />

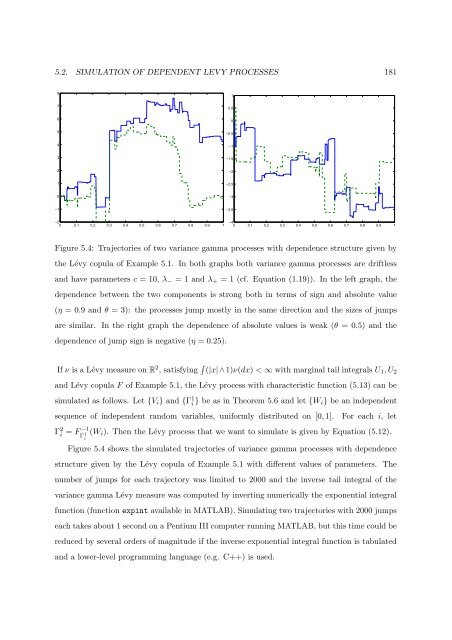

Figure 5.4: Trajectories of two variance gamma processes with <strong>de</strong>p<strong>en</strong><strong>de</strong>nce structure giv<strong>en</strong> by<br />

the Lévy copula of Example 5.1. In both graphs both variance gamma processes are driftless<br />

and have param<strong>et</strong>ers c = 10, λ − = 1 and λ + = 1 (cf. Equation (1.19)). In the left graph, the<br />

<strong>de</strong>p<strong>en</strong><strong>de</strong>nce b<strong>et</strong>we<strong>en</strong> the two compon<strong>en</strong>ts is strong both in terms of sign and absolute value<br />

(η = 0.9 and θ = 3): the processes jump mostly in the same direction and the sizes of jumps<br />

are similar. In the right graph the <strong>de</strong>p<strong>en</strong><strong>de</strong>nce of absolute values is weak (θ = 0.5) and the<br />

<strong>de</strong>p<strong>en</strong><strong>de</strong>nce of jump sign is negative (η = 0.25).<br />

If ν is a Lévy measure on R 2 , satisfying ∫ (|x|∧1)ν(dx) < ∞ with marginal tail integrals U 1 , U 2<br />

and Lévy copula F of Example 5.1, the Lévy process with characteristic function (5.13) can be<br />

simulated as follows. L<strong>et</strong> {V i } and {Γ 1 i } be as in Theorem 5.6 and l<strong>et</strong> {W i} be an in<strong>de</strong>p<strong>en</strong><strong>de</strong>nt<br />

sequ<strong>en</strong>ce of in<strong>de</strong>p<strong>en</strong><strong>de</strong>nt random variables, uniformly distributed on [0, 1].<br />

For each i, l<strong>et</strong><br />

Γ 2 i = F −1 (W<br />

Γ 1 i ). Th<strong>en</strong> the Lévy process that we want to simulate is giv<strong>en</strong> by Equation (5.12).<br />

i<br />

Figure 5.4 shows the simulated trajectories of variance gamma processes with <strong>de</strong>p<strong>en</strong><strong>de</strong>nce<br />

structure giv<strong>en</strong> by the Lévy copula of Example 5.1 with differ<strong>en</strong>t values of param<strong>et</strong>ers. The<br />

number of jumps for each trajectory was limited to 2000 and the inverse tail integral of the<br />

variance gamma Lévy measure was computed by inverting numerically the expon<strong>en</strong>tial integral<br />

function (function expint available in MATLAB). Simulating two trajectories with 2000 jumps<br />

each takes about 1 second on a P<strong>en</strong>tium III computer running MATLAB, but this time could be<br />

reduced by several or<strong>de</strong>rs of magnitu<strong>de</strong> if the inverse expon<strong>en</strong>tial integral function is tabulated<br />

and a lower-level programming language (e.g. C++) is used.