4.4.2 Financial analysisAlthough in this project the owner <strong>of</strong> the infrastructure (the Municipality) is different from the opera<strong>to</strong>r(the private partner <strong>of</strong> BOT assignment), a consolidated financial analysis is carried out. The time horizonfor the analysis is assumed <strong>to</strong> be 30 years, the same as for the BOT.In the analysis constant prices are used and corrections are entered for changes in the relative prices. Suchadjustments are undertaken by assuming an average annual inflation rate <strong>of</strong> 1.5% and also by taking in<strong>to</strong>account growth fac<strong>to</strong>rs, marginal decreases in the prices <strong>of</strong> some services and some operating costs (seebelow for details). Thus, only relative price changes are considered. The financial rate <strong>of</strong> discount is 5%,expressed in real terms.The cost <strong>of</strong> the <strong>investment</strong> includes the construction <strong>of</strong> the effluent and discharge mains, <strong>of</strong> the wastewater treatment plant, the water refining treatment plant and the aqueducts (including the pumpinghouses) <strong>to</strong> supply water resources <strong>to</strong> the industrial and irrigated areas. The cost <strong>of</strong> such an <strong>investment</strong>,excluding VAT, is set at €100,831,000 (at constant price) 82 and has been subdivided in<strong>to</strong> homogeneouscategories, whose values have been attributed <strong>to</strong> the first three periods, on the basis <strong>of</strong> the timeprogramme for the implementation <strong>of</strong> the project.Table 4.39 Distribution <strong>of</strong> <strong>investment</strong> cost in the time horizonInvestment costs at constant prices (Thousands <strong>of</strong> Euros) Total 1y 2y 3yFeasibility study, design, work management, licensing, etc. 9,259 7,363 0 1,896Land expropriation 1,094 726 368 0Labour 43,323 4,255 25,915 13,152Materials for civil works 12,900 990 7,031 4,078Rentals 3,238 26 1,607 1,604Transports 2,681 44 1,331 1,306Electro-mechanical components and equipment 29,138 0 11,551 17,587Total <strong>investment</strong> 100,831 13,404 47,804 39,623The start-up phase, lasting 5 months, will commence in the fourth year, in which the production isassumed <strong>to</strong> be at 70% <strong>of</strong> the regime production. The components <strong>of</strong> short lifetime 83 (60% <strong>of</strong> theequipment costs) will be replaced once during the <strong>investment</strong> horizon, at the end <strong>of</strong> their economic life(16 years 84 ). For the sake <strong>of</strong> simplicity, the calculation is made by introducing the whole cost <strong>of</strong> theaforementioned components in the twentieth year 85 .Keeping in mind the aforementioned PPP arrangement scheme, the <strong>investment</strong> is financed 86 by grant(ERDF and national or regional funds), by the fund provided by Municipality and by funds provided bythe private partner. The requested co-financing EU grant is €22,129,000 (21.9% <strong>of</strong> <strong>to</strong>tal <strong>investment</strong> costsat current prices without VAT). An amount <strong>of</strong> €19,029,000 (18.9% <strong>of</strong> <strong>investment</strong> costs) is provided by anational or regional fund. The Municipal fund is €10,263,000 (10.2% <strong>of</strong> <strong>investment</strong> costs). The privatefinancing (€49,410,000, the 49.0% <strong>of</strong> <strong>investment</strong> costs) is given by equity for 50% <strong>of</strong> the amount(€24,705,000) and by loan for the other 50% (€24,705,000). The loan has a 5.00% interest rate with anamortization period <strong>of</strong> 10 years.The financing for the replacement <strong>of</strong> the short life-time components is provided by the private partner(50% equity, 50% loan) in the 20 th year (€22,652,000).8283848586The cost <strong>of</strong> the <strong>investment</strong> at current prices is € 100,831,451.These are, basically, machines and other electromechanical equipment for the treatment and pumping plants.In accordance with the technical data from literature.The twentieth year has been determined taking in<strong>to</strong> account 3 years <strong>of</strong> plant construction plus 16 years <strong>of</strong> life.The sum <strong>to</strong> be financed is the cost <strong>of</strong> <strong>investment</strong> net <strong>of</strong> VAT.170

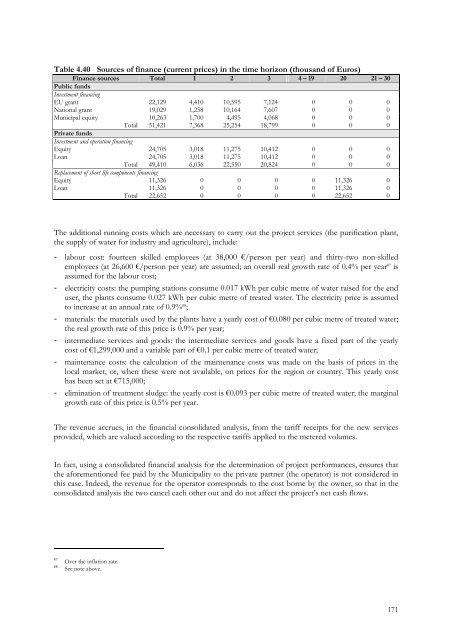

Table 4.40 Sources <strong>of</strong> finance (current prices) in the time horizon (thousand <strong>of</strong> Euros)Finance sources Total 1 2 3 4 – 19 20 21 – 30Public fundsInvestment financingEU grant 22,129 4,410 10,595 7,124 0 0 0National grant 19,029 1,258 10,164 7,607 0 0 0Municipal equity 10,263 1,700 4,495 4,068 0 0 0Total 51,421 7,368 25,254 18,799 0 0 0Private fundsInvestment and operation financingEquity 24,705 3,018 11,275 10,412 0 0 0Loan 24,705 3,018 11,275 10,412 0 0 0Total 49,410 6,036 22,550 20,824 0 0 0Replacement <strong>of</strong> short life components financingEquity 11,326 0 0 0 0 11,326 0Loan 11,326 0 0 0 0 11,326 0Total 22,652 0 0 0 0 22,652 0The additional running costs which are necessary <strong>to</strong> carry out the project services (the purification plant,the supply <strong>of</strong> water for industry and agriculture), include:- labour cost: fourteen skilled employees (at 38,000 €/person per year) and thirty-two non-skilledemployees (at 26,600 €/person per year) are assumed; an overall real growth rate <strong>of</strong> 0.4% per year 87 isassumed for the labour cost;- electricity costs: the pumping stations consume 0.017 kWh per cubic metre <strong>of</strong> water raised for the enduser, the plants consume 0.027 kWh per cubic metre <strong>of</strong> treated water. The electricity price is assumed<strong>to</strong> increase at an annual rate <strong>of</strong> 0.9% 88 ;- materials: the materials used by the plants have a yearly cost <strong>of</strong> €0.080 per cubic metre <strong>of</strong> treated water;the real growth rate <strong>of</strong> this price is 0.9% per year;- intermediate services and goods: the intermediate services and goods have a fixed part <strong>of</strong> the yearlycost <strong>of</strong> €1,299,000 and a variable part <strong>of</strong> €0.1 per cubic metre <strong>of</strong> treated water;- maintenance costs: the calculation <strong>of</strong> the maintenance costs was made on the basis <strong>of</strong> prices in thelocal market, or, when these were not available, on prices for the region or country. This yearly costhas been set at €715,000;- elimination <strong>of</strong> treatment sludge: the yearly cost is €0.093 per cubic metre <strong>of</strong> treated water; the marginalgrowth rate <strong>of</strong> this price is 0.5% per year.The revenue accrues, in the financial consolidated analysis, from the tariff receipts for the new servicesprovided, which are valued according <strong>to</strong> the respective tariffs applied <strong>to</strong> the metered volumes.In fact, using a consolidated financial analysis for the determination <strong>of</strong> project performances, ensures thatthe aforementioned fee paid by the Municipality <strong>to</strong> the private partner (the opera<strong>to</strong>r) is not considered inthis case. Indeed, the revenue for the opera<strong>to</strong>r corresponds <strong>to</strong> the cost borne by the owner, so that in theconsolidated analysis the two cancel each other out and do not affect the project’s net cash flows.8788Over the inflation rate.See note above.171

- Page 3:

ACRONYMS AND ABBREVIATIONSBAUB/CCBA

- Page 7 and 8:

TABLESTable 2.1 Financial analysis

- Page 9:

FIGURESFigure 1.1 Project cost spre

- Page 12 and 13:

Cohesion Fund, and through the leve

- Page 14 and 15:

or the plant will not reveal excess

- Page 17 and 18:

CHAPTER ONEPROJECT APPRAISAL IN THE

- Page 19 and 20:

Some specifications for financial t

- Page 21 and 22:

FOCUS: INFORMATION REQUIREDGeneral

- Page 23 and 24:

In particular, CBA results should p

- Page 25 and 26:

CHAPTER TWOAN AGENDA FOR THE PROJEC

- Page 27 and 28:

objectives, are, as far as possible

- Page 29 and 30:

considered the appropriate shadow p

- Page 31 and 32:

2.3.2 Feasibility analysisFeasibili

- Page 34 and 35:

This approach will be presented in

- Page 36 and 37:

Current assets include:- receivable

- Page 38 and 39:

The following items are usually not

- Page 40 and 41:

Mainly, the examiner uses the FRR(C

- Page 42 and 43:

The dynamics of the incoming flows

- Page 44 and 45:

eturn on their own capital (Kp). Th

- Page 46 and 47:

While the approach presented in thi

- Page 48 and 49:

2.5.1 Conversion of market to accou

- Page 50 and 51:

Table 2.9 Electricity price dispers

- Page 52 and 53:

2.5.1.2 Fiscal correctionsSome item

- Page 54 and 55:

previously estimated in projects wi

- Page 56 and 57:

FOCUS: ENPV VS. FNPVThe difference

- Page 58 and 59:

2.6 Risk assessmentProject appraisa

- Page 60 and 61:

Table 2.14 Impact analysis of criti

- Page 62 and 63:

Figure 2.6 Probability distribution

- Page 64 and 65:

eneficiary. The project proposer sh

- Page 66 and 67:

There are many ways to design an MC

- Page 68 and 69:

PROJECT APPRAISAL CHECK-LISTCONTEXT

- Page 70 and 71:

- reduction of congestion by elimin

- Page 72 and 73:

- the methods applied to estimate e

- Page 74 and 75:

- the marginal external costs: cong

- Page 76 and 77:

- the benefits for the existing tra

- Page 78 and 79:

The following tables show some refe

- Page 80 and 81:

3.1.1.6 Risk assessmentDue to their

- Page 82 and 83:

As shown in Figure 3.1, only under

- Page 84 and 85:

3.1.3.7 Other project evaluation ap

- Page 87 and 88:

- Waste Management Hierarchy rules

- Page 89 and 90:

The time horizon for a project anal

- Page 91 and 92:

3.2.1.7 Other project evaluation ap

- Page 93 and 94:

every user support the total costs

- Page 95 and 96:

Territorial reference frameworkIf t

- Page 97 and 98:

Cycle and phases of the projectGrea

- Page 99 and 100:

One of the most important aims of t

- Page 101 and 102:

projects, as in other sectors in wh

- Page 103 and 104:

3.2.3.2 Project identificationBasic

- Page 105 and 106:

3.2.3.7 Other project evaluation ap

- Page 107 and 108:

In order to evaluate the overall im

- Page 109 and 110:

for regassification plants, number

- Page 111 and 112:

Examples of objectives are:- change

- Page 113 and 114:

decontamination if any;- the techni

- Page 115 and 116:

3.3.3.6 Risk AnalysisCritical facto

- Page 117 and 118:

3.3.4.6 Risk assessmentCritical fac

- Page 119 and 120: 3.4.1.5 Economic analysisThe follow

- Page 121 and 122: Financial inflows• Admission fees

- Page 123 and 124: expectancy suitably adjusted by the

- Page 125 and 126: The time horizon for project analys

- Page 127 and 128: A Cost-Benefit Analysis should cons

- Page 129 and 130: CHAPTER FOURCASE STUDIESOverviewThi

- Page 131 and 132: - finally, there is the traffic tha

- Page 134 and 135: c) Road users producer’s surplus:

- Page 136 and 137: 4.1.5 Scenario analysisTwo scenario

- Page 138 and 139: The financial performance indicator

- Page 140 and 141: Table 4.10 Economic analysis (Milli

- Page 142 and 143: Table 4.12 Financial return on capi

- Page 144 and 145: 4.2 Case Study: investment in a rai

- Page 146 and 147: 4.2.4 Economic analysisThe benefits

- Page 148 and 149: Financial investment costs have bee

- Page 150 and 151: Figure 4.6 Results of the risk anal

- Page 152 and 153: Table 4.22 Economic analysis (Milli

- Page 154 and 155: Table 4.24 Financial return on capi

- Page 156 and 157: 4.3 Case Study: investment in an in

- Page 158 and 159: ate of 0.6% per year is assumed for

- Page 160 and 161: The shadow price of the CO 2 avoide

- Page 162 and 163: As a result, the probability distri

- Page 164 and 165: Table 4.36 Financial return on capi

- Page 166 and 167: 16 17 18 19 20 21 22 23 24 25 26 27

- Page 168 and 169: 4.4 Case Study: investment in a was

- Page 172 and 173: THE CALCULATION OF REVENUESReferrin

- Page 174 and 175: 0.15 m 3 /m 2 a depreciation of 20%

- Page 176 and 177: As result, the probability distribu

- Page 178 and 179: Figure 4.13 Probability distributio

- Page 180 and 181: Table 4.48 Financial return on nati

- Page 182 and 183: Table 4.50 Financial return on priv

- Page 184 and 185: 16 17 18 19 20 21 22 23 24 25 26 27

- Page 186 and 187: 4.5 Case Study: industrial investme

- Page 188 and 189: 4.5.4.1 Investment costsThe total i

- Page 190 and 191: Finally, a residual value was estim

- Page 192 and 193: This analysis shows the need to pay

- Page 194 and 195: Table 4.62 Financial return on inve

- Page 196 and 197: Table 4.64 Return on private equity

- Page 198 and 199: Table 4.66 Economic analysis (thous

- Page 200 and 201: ANNEX ADEMAND ANALYSISDemand foreca

- Page 202 and 203: The method applied for the forecast

- Page 204 and 205: Furthermore, travel demand depends

- Page 206 and 207: This Guide supports a unique refere

- Page 208 and 209: A higher discount rate for countrie

- Page 210 and 211: Figure C.1 Project ranking by NPV v

- Page 212 and 213: The main problems with this indicat

- Page 214 and 215: EXAMPLE OF SHADOW WAGE IN DUAL MARK

- Page 216 and 217: Another exhaustive way to include d

- Page 218 and 219: Figure E.2 Percentage of low income

- Page 220 and 221:

ANNEX FEVALUATION OF HEALTH &ENVIRO

- Page 222 and 223:

Figure F.1 Main evaluation methodsS

- Page 224 and 225:

- expenditure on capital equipment

- Page 226 and 227:

due to air pollution or water conta

- Page 228 and 229:

BENEFIT TRANSFER - SELECTED REFEREN

- Page 230 and 231:

ANNEX GEVALUATION OF PPP PROJECTSIt

- Page 232 and 233:

adjustments for Competitive Neutral

- Page 234 and 235:

ANNEX HRISK ASSESSMENTIn ex-ante pr

- Page 236 and 237:

Reference ForecastingThe question o

- Page 238 and 239:

Figure H.5 Levels of risks in diffe

- Page 240 and 241:

ANNEX IDETERMINATION OF THE EU GRAN

- Page 242 and 243:

A.4. Technological Alternatives and

- Page 244 and 245:

GLOSSARYAccounting period: the inte

- Page 246 and 247:

Market price: the price at which a

- Page 248 and 249:

BIBLIOGRAPHY1. ReferencesBelli, P.,

- Page 250 and 251:

Ray, A. 1984, Cost-benefit analysis

- Page 252 and 253:

EnvironmentGeneralAtkinson, G., 200

- Page 254 and 255:

European Commission, DG Tren, 2003,