THE CALCULATION OF REVENUESReferring <strong>to</strong> a base years, the revenue predicted has been calculated as follows:- civil purification service (in the current situation ‘without the intervention’ no purification charge is applied): 50.3 Mm 3 /year* €0.283 per m 3 * 0.950 = 13,523,000€/y 89 ;- industrial supply in the reservoir: 12.1 Mm 3 /year * €0.480 per m 3 * 0.995= 5,779,000€/y;- irrigation supply: 15.75 Mm 3 /year * €0.030 per m 3 * 0.87 = 411,000€/y;- <strong>to</strong> take in<strong>to</strong> account the certain expected level <strong>of</strong> evasion <strong>of</strong> the payment <strong>of</strong> service bills the following ‘dispersion fac<strong>to</strong>rs’have been applied cautiously before revenue calculating: municipal services: 5%, industrial water supply service: 0.5%,irrigating water supply service: 13%.- at the end, in calculating the performance indices, the values <strong>of</strong> the revenues in each year are obtained starting from theabove baseline values and taking in<strong>to</strong> account the growth in the water demands (see above) and the dynamics <strong>of</strong> currentprices.In addition <strong>to</strong> the above mentioned revenues, the residual value, over the 27 years <strong>of</strong> life <strong>of</strong> theinfrastructures 90 , is set <strong>to</strong> be 4.0% <strong>of</strong> the initial costs <strong>of</strong> the long life parts <strong>of</strong> the <strong>investment</strong> plus 3.8% <strong>of</strong>the costs <strong>of</strong> the replaced components (short life parts). The <strong>to</strong>tal residual value (€6,030,000, expressed atconstant prices and not discounted) is allocated in the last year (30 th ) <strong>of</strong> the <strong>investment</strong> period.The financial performance indica<strong>to</strong>rs are:- Financial Net Present Value (<strong>investment</strong>) FNPV(C) €–29,083,911- Financial Rate <strong>of</strong> Return (<strong>investment</strong>) FRR(C) 1.9%- Financial Net Present Value (capital) FNPV(K) €–8,357,812 91- Financial Rate <strong>of</strong> Return (capital) FRR(K) 3.7%As for the financial sustainability <strong>of</strong> the project, the cumulative cash flow <strong>of</strong> the project is always positivewith a minimum value <strong>of</strong> about €788,000, occurring in the fifth year.Moreover, if the service fee is set at €0.02 per cubic metre <strong>of</strong> treated water, the separate analysis <strong>of</strong> thefinancial pr<strong>of</strong>itability <strong>of</strong> the local public capital (Municipal funds, i.e.: FNPV(K g ) and FRR(K g )) and thefinancial pr<strong>of</strong>itability <strong>of</strong> the private capital (equity and loan <strong>to</strong> finance the <strong>investment</strong> and replacementcosts and the cash deficit in the early years <strong>of</strong> operation, i.e.: FNPV(K p ) and FRR(K p )) – net <strong>of</strong> EU grant– gives the following results:- Public partner <strong>of</strong> the PPP (municipality) FNPV(K g ) €3,491,008 92FRR(K g ) 7.8%- Private partner <strong>of</strong> the PPP (opera<strong>to</strong>r firm) FNPV(K p ) €5,139,536FRR(K p ) 6.5%For this project, the maximum amount <strong>to</strong> which the co-financing rate <strong>of</strong> the priority axis applies is€32,467,727. This is determined by multiplying the project eligible cost (in this case €100,831,451 atcurrent price) by the funding-gap rate (32.2%). Assuming the co-financing rate for the priority axis is equal<strong>to</strong> 80%, then the maximum EU contribution is €25,974,182.89Note that the rate <strong>of</strong> the purification service is applied <strong>to</strong> the volume <strong>of</strong> water delivered <strong>to</strong> users, as measured by the water meters.90At the end <strong>of</strong> the horizon time, the operative life <strong>of</strong> the plants and other equipments is equal <strong>to</strong> the analysis horizon minus the constructiontime: 30 – 3 = 27 years.91In the table 3.32, the functioning financial costs are financed by short-term loans with an average interest <strong>of</strong> 8%.92The sum <strong>of</strong> FNPV(Kg) and FNPV(Kp) is not equal <strong>to</strong> FNPV(K), because the amount <strong>of</strong> capital expenditures incurred separately by thepartners does not include the national contribution, that instead is considered, in addition <strong>to</strong> above mentioned contributions, in the calculation <strong>of</strong>FNPV(K). A similar reasoning applies <strong>to</strong> the values <strong>of</strong> FRR(K).172

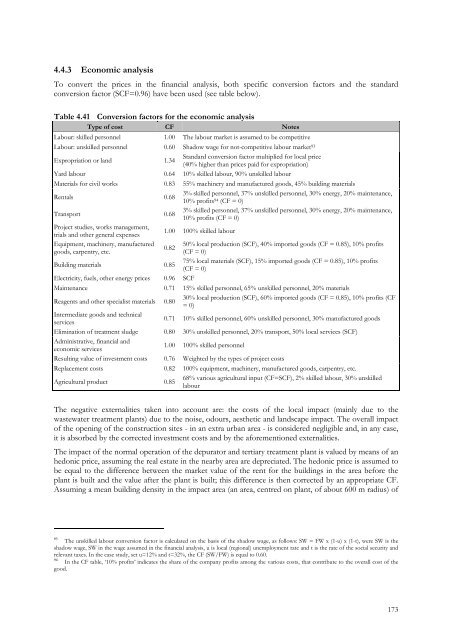

4.4.3 Economic analysisTo convert the prices in the financial analysis, both specific conversion fac<strong>to</strong>rs and the standardconversion fac<strong>to</strong>r (SCF=0.96) have been used (see table below).Table 4.41 Conversion fac<strong>to</strong>rs for the economic analysisType <strong>of</strong> cost CF NotesLabour: skilled personnel 1.00 The labour market is assumed <strong>to</strong> be competitiveLabour: unskilled personnel 0.60 Shadow wage for not-competitive labour market 93Expropriation or land 1.34Standard conversion fac<strong>to</strong>r multiplied for local price(40% higher than prices paid for expropriation)Yard labour 0.64 10% skilled labour, 90% unskilled labourMaterials for civil works 0.83 55% machinery and manufactured goods, 45% building materialsRentals 0.683% skilled personnel, 37% unskilled personnel, 30% energy, 20% maintenance,10% pr<strong>of</strong>its 94 (CF = 0)Transport 0.683% skilled personnel, 37% unskilled personnel, 30% energy, 20% maintenance,10% pr<strong>of</strong>its (CF = 0)Project studies, works management,trials and other general expenses1.00 100% skilled labourEquipment, machinery, manufactured 50% local production (SCF), 40% imported goods (CF = 0.85), 10% pr<strong>of</strong>its0.82goods, carpentry, etc.(CF = 0)Building materials 0.8575% local materials (SCF), 15% imported goods (CF = 0.85), 10% pr<strong>of</strong>its(CF = 0)Electricity, fuels, other energy prices 0.96 SCFMaintenance 0.71 15% skilled personnel, 65% unskilled personnel, 20% materialsReagents and other specialist materials 0.8030% local production (SCF), 60% imported goods (CF = 0.85), 10% pr<strong>of</strong>its (CF= 0)Intermediate goods and technicalservices0.71 10% skilled personnel, 60% unskilled personnel, 30% manufactured goodsElimination <strong>of</strong> treatment sludge 0.80 30% unskilled personnel, 20% transport, 50% local services (SCF)Administrative, financial andeconomic services1.00 100% skilled personnelResulting value <strong>of</strong> <strong>investment</strong> costs 0.76 Weighted by the types <strong>of</strong> project costsReplacement costs 0.82 100% equipment, machinery, manufactured goods, carpentry, etc.Agricultural product 0.8568% various agricultural input (CF=SCF), 2% skilled labour, 30% unskilledlabourThe negative externalities taken in<strong>to</strong> account are: the costs <strong>of</strong> the local impact (mainly due <strong>to</strong> thewastewater treatment plants) due <strong>to</strong> the noise, odours, aesthetic and landscape impact. The overall impac<strong>to</strong>f the opening <strong>of</strong> the construction sites - in an extra urban area - is considered negligible and, in any case,it is absorbed by the corrected <strong>investment</strong> costs and by the aforementioned externalities.The impact <strong>of</strong> the normal operation <strong>of</strong> the depura<strong>to</strong>r and tertiary treatment plant is valued by means <strong>of</strong> anhedonic price, assuming the real estate in the nearby area are depreciated. The hedonic price is assumed <strong>to</strong>be equal <strong>to</strong> the difference between the market value <strong>of</strong> the rent for the buildings in the area before theplant is built and the value after the plant is built; this difference is then corrected by an appropriate CF.Assuming a mean building density in the impact area (an area, centred on plant, <strong>of</strong> about 600 m radius) <strong>of</strong>93The unskilled labour conversion fac<strong>to</strong>r is calculated on the basis <strong>of</strong> the shadow wage, as follows: SW = FW x (1-u) x (1-t), were SW is theshadow wage, SW in the wage assumed in the financial analysis, u is local (regional) unemployment rate and t is the rate <strong>of</strong> the social security andrelevant taxes. In the case study, set u=12% and t=32%, the CF (SW/FW) is equal <strong>to</strong> 0.60.94In the CF table, ‘10% pr<strong>of</strong>its’ indicates the share <strong>of</strong> the company pr<strong>of</strong>its among the various costs, that contribute <strong>to</strong> the overall cost <strong>of</strong> thegood.173

- Page 3:

ACRONYMS AND ABBREVIATIONSBAUB/CCBA

- Page 7 and 8:

TABLESTable 2.1 Financial analysis

- Page 9:

FIGURESFigure 1.1 Project cost spre

- Page 12 and 13:

Cohesion Fund, and through the leve

- Page 14 and 15:

or the plant will not reveal excess

- Page 17 and 18:

CHAPTER ONEPROJECT APPRAISAL IN THE

- Page 19 and 20:

Some specifications for financial t

- Page 21 and 22:

FOCUS: INFORMATION REQUIREDGeneral

- Page 23 and 24:

In particular, CBA results should p

- Page 25 and 26:

CHAPTER TWOAN AGENDA FOR THE PROJEC

- Page 27 and 28:

objectives, are, as far as possible

- Page 29 and 30:

considered the appropriate shadow p

- Page 31 and 32:

2.3.2 Feasibility analysisFeasibili

- Page 34 and 35:

This approach will be presented in

- Page 36 and 37:

Current assets include:- receivable

- Page 38 and 39:

The following items are usually not

- Page 40 and 41:

Mainly, the examiner uses the FRR(C

- Page 42 and 43:

The dynamics of the incoming flows

- Page 44 and 45:

eturn on their own capital (Kp). Th

- Page 46 and 47:

While the approach presented in thi

- Page 48 and 49:

2.5.1 Conversion of market to accou

- Page 50 and 51:

Table 2.9 Electricity price dispers

- Page 52 and 53:

2.5.1.2 Fiscal correctionsSome item

- Page 54 and 55:

previously estimated in projects wi

- Page 56 and 57:

FOCUS: ENPV VS. FNPVThe difference

- Page 58 and 59:

2.6 Risk assessmentProject appraisa

- Page 60 and 61:

Table 2.14 Impact analysis of criti

- Page 62 and 63:

Figure 2.6 Probability distribution

- Page 64 and 65:

eneficiary. The project proposer sh

- Page 66 and 67:

There are many ways to design an MC

- Page 68 and 69:

PROJECT APPRAISAL CHECK-LISTCONTEXT

- Page 70 and 71:

- reduction of congestion by elimin

- Page 72 and 73:

- the methods applied to estimate e

- Page 74 and 75:

- the marginal external costs: cong

- Page 76 and 77:

- the benefits for the existing tra

- Page 78 and 79:

The following tables show some refe

- Page 80 and 81:

3.1.1.6 Risk assessmentDue to their

- Page 82 and 83:

As shown in Figure 3.1, only under

- Page 84 and 85:

3.1.3.7 Other project evaluation ap

- Page 87 and 88:

- Waste Management Hierarchy rules

- Page 89 and 90:

The time horizon for a project anal

- Page 91 and 92:

3.2.1.7 Other project evaluation ap

- Page 93 and 94:

every user support the total costs

- Page 95 and 96:

Territorial reference frameworkIf t

- Page 97 and 98:

Cycle and phases of the projectGrea

- Page 99 and 100:

One of the most important aims of t

- Page 101 and 102:

projects, as in other sectors in wh

- Page 103 and 104:

3.2.3.2 Project identificationBasic

- Page 105 and 106:

3.2.3.7 Other project evaluation ap

- Page 107 and 108:

In order to evaluate the overall im

- Page 109 and 110:

for regassification plants, number

- Page 111 and 112:

Examples of objectives are:- change

- Page 113 and 114:

decontamination if any;- the techni

- Page 115 and 116:

3.3.3.6 Risk AnalysisCritical facto

- Page 117 and 118:

3.3.4.6 Risk assessmentCritical fac

- Page 119 and 120:

3.4.1.5 Economic analysisThe follow

- Page 121 and 122: Financial inflows• Admission fees

- Page 123 and 124: expectancy suitably adjusted by the

- Page 125 and 126: The time horizon for project analys

- Page 127 and 128: A Cost-Benefit Analysis should cons

- Page 129 and 130: CHAPTER FOURCASE STUDIESOverviewThi

- Page 131 and 132: - finally, there is the traffic tha

- Page 134 and 135: c) Road users producer’s surplus:

- Page 136 and 137: 4.1.5 Scenario analysisTwo scenario

- Page 138 and 139: The financial performance indicator

- Page 140 and 141: Table 4.10 Economic analysis (Milli

- Page 142 and 143: Table 4.12 Financial return on capi

- Page 144 and 145: 4.2 Case Study: investment in a rai

- Page 146 and 147: 4.2.4 Economic analysisThe benefits

- Page 148 and 149: Financial investment costs have bee

- Page 150 and 151: Figure 4.6 Results of the risk anal

- Page 152 and 153: Table 4.22 Economic analysis (Milli

- Page 154 and 155: Table 4.24 Financial return on capi

- Page 156 and 157: 4.3 Case Study: investment in an in

- Page 158 and 159: ate of 0.6% per year is assumed for

- Page 160 and 161: The shadow price of the CO 2 avoide

- Page 162 and 163: As a result, the probability distri

- Page 164 and 165: Table 4.36 Financial return on capi

- Page 166 and 167: 16 17 18 19 20 21 22 23 24 25 26 27

- Page 168 and 169: 4.4 Case Study: investment in a was

- Page 170 and 171: 4.4.2 Financial analysisAlthough in

- Page 174 and 175: 0.15 m 3 /m 2 a depreciation of 20%

- Page 176 and 177: As result, the probability distribu

- Page 178 and 179: Figure 4.13 Probability distributio

- Page 180 and 181: Table 4.48 Financial return on nati

- Page 182 and 183: Table 4.50 Financial return on priv

- Page 184 and 185: 16 17 18 19 20 21 22 23 24 25 26 27

- Page 186 and 187: 4.5 Case Study: industrial investme

- Page 188 and 189: 4.5.4.1 Investment costsThe total i

- Page 190 and 191: Finally, a residual value was estim

- Page 192 and 193: This analysis shows the need to pay

- Page 194 and 195: Table 4.62 Financial return on inve

- Page 196 and 197: Table 4.64 Return on private equity

- Page 198 and 199: Table 4.66 Economic analysis (thous

- Page 200 and 201: ANNEX ADEMAND ANALYSISDemand foreca

- Page 202 and 203: The method applied for the forecast

- Page 204 and 205: Furthermore, travel demand depends

- Page 206 and 207: This Guide supports a unique refere

- Page 208 and 209: A higher discount rate for countrie

- Page 210 and 211: Figure C.1 Project ranking by NPV v

- Page 212 and 213: The main problems with this indicat

- Page 214 and 215: EXAMPLE OF SHADOW WAGE IN DUAL MARK

- Page 216 and 217: Another exhaustive way to include d

- Page 218 and 219: Figure E.2 Percentage of low income

- Page 220 and 221: ANNEX FEVALUATION OF HEALTH &ENVIRO

- Page 222 and 223:

Figure F.1 Main evaluation methodsS

- Page 224 and 225:

- expenditure on capital equipment

- Page 226 and 227:

due to air pollution or water conta

- Page 228 and 229:

BENEFIT TRANSFER - SELECTED REFEREN

- Page 230 and 231:

ANNEX GEVALUATION OF PPP PROJECTSIt

- Page 232 and 233:

adjustments for Competitive Neutral

- Page 234 and 235:

ANNEX HRISK ASSESSMENTIn ex-ante pr

- Page 236 and 237:

Reference ForecastingThe question o

- Page 238 and 239:

Figure H.5 Levels of risks in diffe

- Page 240 and 241:

ANNEX IDETERMINATION OF THE EU GRAN

- Page 242 and 243:

A.4. Technological Alternatives and

- Page 244 and 245:

GLOSSARYAccounting period: the inte

- Page 246 and 247:

Market price: the price at which a

- Page 248 and 249:

BIBLIOGRAPHY1. ReferencesBelli, P.,

- Page 250 and 251:

Ray, A. 1984, Cost-benefit analysis

- Page 252 and 253:

EnvironmentGeneralAtkinson, G., 200

- Page 254 and 255:

European Commission, DG Tren, 2003,