Engineering

Engineering

Engineering

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

2.7 Management report on the Group Expected developments and and associated opportunities and and risks risks<br />

Implementing the Strategic Way Forward<br />

and improving our financial situation are are<br />

our main goals for 2011/2012.<br />

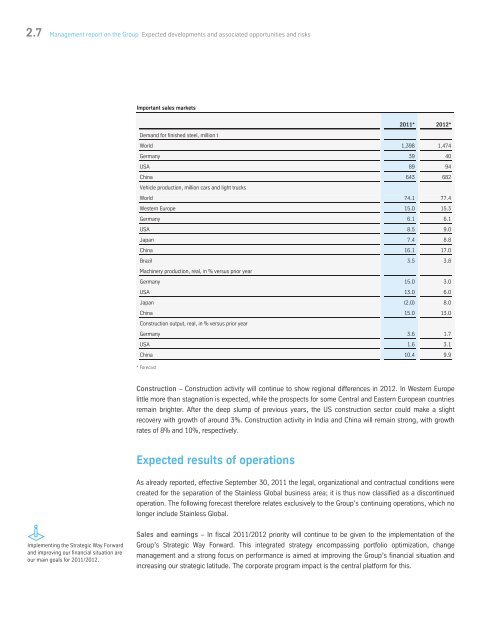

Important sales markets<br />

Demand for finished steel, million t<br />

104<br />

2011* 2012*<br />

World 1,398 1,474<br />

Germany 39 40<br />

USA 89 94<br />

China 643 682<br />

Vehicle production, million cars and light trucks<br />

World 74.1 77.4<br />

Western Europe 15.0 15.3<br />

Germany 6.1 6.1<br />

USA 8.5 9.0<br />

Japan 7.4 8.8<br />

China 16.1 17.0<br />

Brazil 3.5 3.8<br />

Machinery production, real, in % versus prior year<br />

Germany 15.0 3.0<br />

USA 13.0 6.0<br />

Japan (2.0) 8.0<br />

China 15.0 13.0<br />

Construction output, real, in % versus prior year<br />

Germany 3.6 1.7<br />

USA 1.6 3.1<br />

China 10.4 9.9<br />

* Forecast<br />

Construction – Construction activity will continue to show regional differences in 2012. In Western Europe<br />

little more than stagnation is expected, while the prospects for some Central and Eastern European countries<br />

remain brighter. After the deep slump of previous years, the US construction sector could make a slight<br />

recovery with growth of around 3%. Construction activity in India and China will remain strong, with growth<br />

rates of 8% and 10%, respectively.<br />

Expected results of operations<br />

As already reported, effective September 30, 2011 the legal, organizational and contractual conditions were<br />

created for the separation of the Stainless Global business area; it is thus now classified as a discontinued<br />

operation. The following forecast therefore relates exclusively to the Group’s continuing operations, which no<br />

longer include Stainless Global.<br />

Sales and earnings – In fiscal 2011/2012 priority will continue to be given to the implementation of the<br />

Group’s Strategic Way Forward. This integrated strategy encompassing portfolio optimization, change<br />

management and a strong focus on performance is aimed at improving the Group’s financial situation and<br />

increasing our strategic latitude. The corporate program impact is the central platform for this.