Maritime Trade and Transport - HWWI

Maritime Trade and Transport - HWWI

Maritime Trade and Transport - HWWI

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

15%<br />

10%<br />

5%<br />

0%<br />

20%<br />

15%<br />

10%<br />

5%<br />

Annual capacity growth in the container ship fleet<br />

in the past 20 years in %<br />

1986 1991 1996 2001 2006<br />

Fig. 6<br />

Source: Clarkson Research Services (2006).<br />

Breakdown of the world container fleet by capacity (in dwt)<br />

14.6%<br />

8.9% 8.5%<br />

0%<br />

0 ≤ 1500 1500-<br />

1999<br />

2000-<br />

2499<br />

2500-<br />

2999<br />

3000-<br />

3499<br />

3500-<br />

3999<br />

4000-<br />

4499<br />

4500-<br />

4999<br />

5000-<br />

5999<br />

6000-<br />

6999<br />

7000-<br />

7999<br />

≥ 8000<br />

Fig. 7<br />

Source: ISL Bremen (2006b).<br />

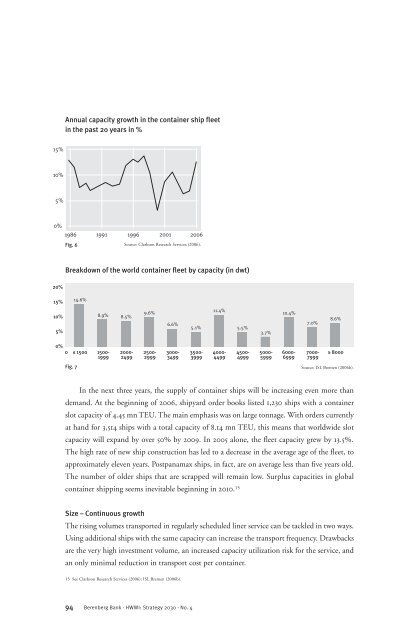

In the next three years, the supply of container ships will be increasing even more than<br />

dem<strong>and</strong>. At the beginning of 2006, shipyard order books listed 1,230 ships with a container<br />

slot capacity of 4.45 mn TEU. The main emphasis was on large tonnage. With orders currently<br />

at h<strong>and</strong> for 3,514 ships with a total capacity of 8.14 mn TEU, this means that worldwide slot<br />

capacity will exp<strong>and</strong> by over 50% by 2009. In 2005 alone, the fleet capacity grew by 13.5%.<br />

The high rate of new ship construction has led to a decrease in the average age of the fleet, to<br />

approximately eleven years. Postpanamax ships, in fact, are on average less than five years old.<br />

The number of older ships that are scrapped will remain low. Surplus capacities in global<br />

container shipping seems inevitable beginning in 2010. 15<br />

Size – Continuous growth<br />

9.6%<br />

6.6%<br />

The rising volumes transported in regularly scheduled liner service can be tackled in two ways.<br />

Using additional ships with the same capacity can increase the transport frequency. Drawbacks<br />

are the very high investment volume, an increased capacity utilization risk for the service, <strong>and</strong><br />

an only minimal reduction in transport cost per container.<br />

15 See Clarkson Research Services (2006); ISL Bremen (2006b).<br />

94 Berenberg Bank · <strong>HWWI</strong>: Strategy 2030 · No. 4<br />

5.1%<br />

11.4%<br />

5.5%<br />

3.7%<br />

10.4%<br />

7.0%<br />

8.6%