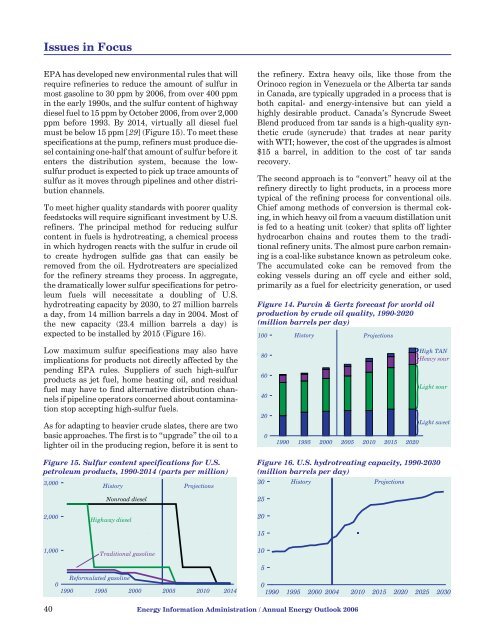

Issues in FocusEPA has developed new environmental rules that willrequire refineries <strong>to</strong> reduce the amount of sulfur inmost gasoline <strong>to</strong> 30 ppm by <strong>2006</strong>, from over 400 ppmin the early 1990s, and the sulfur content of highwaydiesel fuel <strong>to</strong> 15 ppm by Oc<strong>to</strong>ber <strong>2006</strong>, from over 2,000ppm before 1993. By 2014, virtually all diesel fuelmust be below 15 ppm [29] (Figure 15). To meet thesespecifications at the pump, refiners must produce dieselcontaining one-half that amount of sulfur before itenters the distribution system, because the lowsulfurproduct is expected <strong>to</strong> pick up trace amounts ofsulfur as it moves through pipelines and other distributionchannels.To meet higher quality standards <strong>with</strong> poorer qualityfeeds<strong>to</strong>cks will require significant investment by U.S.refiners. The principal method for reducing sulfurcontent in fuels is hydrotreating, a chemical processin which hydrogen reacts <strong>with</strong> the sulfur in crude oil<strong>to</strong> create hydrogen sulfide gas that can easily beremoved from the oil. Hydrotreaters are specializedfor the refinery streams they process. In aggregate,the dramatically lower sulfur specifications for petroleumfuels will necessitate a doubling of U.S.hydrotreating capacity by <strong>2030</strong>, <strong>to</strong> 27 million barrelsa day, from 14 million barrels a day in 2004. Most ofthe new capacity (23.4 million barrels a day) isexpected <strong>to</strong> be installed by 2015 (Figure 16).the refinery. Extra heavy oils, like those from theOrinoco region in Venezuela or the Alberta tar sandsin Canada, are typically upgraded in a process that isboth capital- and energy-intensive but can yield ahighly desirable product. Canada’s Syncrude SweetBlend produced from tar sands is a high-quality syntheticcrude (syncrude) that trades at near parity<strong>with</strong> WTI; however, the cost of the upgrades is almost$15 a barrel, in addition <strong>to</strong> the cost of tar sandsrecovery.The second approach is <strong>to</strong> “convert” heavy oil at therefinery directly <strong>to</strong> light products, in a process moretypical of the refining process for conventional oils.Chief among methods of conversion is thermal coking,in which heavy oil from a vacuum distillation unitis fed <strong>to</strong> a heating unit (coker) that splits off lighterhydrocarbon chains and routes them <strong>to</strong> the traditionalrefinery units. The almost pure carbon remainingis a coal-like substance known as petroleum coke.The accumulated coke can be removed from thecoking vessels during an off cycle and either sold,primarily as a fuel for electricity generation, or usedFigure 14. Purvin & Gertz forecast for world oilproduction by crude oil quality, 1990-2020(million barrels per day)100His<strong>to</strong>ry<strong>Projections</strong>Low maximum sulfur specifications may also haveimplications for products not directly affected by thepending EPA rules. Suppliers of such high-sulfurproducts as jet fuel, home heating oil, and residualfuel may have <strong>to</strong> find alternative distribution channelsif pipeline opera<strong>to</strong>rs concerned about contaminations<strong>to</strong>p accepting high-sulfur fuels.As for adapting <strong>to</strong> heavier crude slates, there are twobasic approaches. The first is <strong>to</strong> “upgrade” the oil <strong>to</strong> alighter oil in the producing region, before it is sent <strong>to</strong>8060402001990 1995 2000 2005 2010 2015 2020High TANHeavy sourLight sourLight sweetFigure 15. Sulfur content specifications for U.S.petroleum products, 1990-2014 (parts per million)3,000His<strong>to</strong>ryNonroad diesel<strong>Projections</strong>Figure 16. U.S. hydrotreating capacity, 1990-<strong>2030</strong>(million barrels per day)30 His<strong>to</strong>ry <strong>Projections</strong>252,000Highway diesel20151,000Traditional gasoline10Reformulated gasoline01990 1995 2000 2005 2010 2014501990 1995 2000 2004 2010 2015 2020 2025 <strong>2030</strong>40 <strong>Energy</strong> Information Administration / <strong>Annual</strong> <strong>Energy</strong> <strong>Outlook</strong> <strong>2006</strong>

Issues in Focusin gasification units <strong>to</strong> provide power, steam, and/orhydrogen for the refinery.U.S. refineries are among the most advanced in theworld, and their technological lead will undoubtedlyleave U.S. refiners uniquely prepared <strong>to</strong> adapt andtake advantage of discounts available for processinginferior crudes. Adaptation will require extensivefuture investments, however, and may take sometime <strong>to</strong> achieve.<strong>Energy</strong> Technologies on the HorizonA key issue in mid-term forecasting is the representationof changing and developing technologies. Howexisting technologies will evolve, and what new technologiesmight emerge, cannot be known <strong>with</strong> certainty.The issue is of particular importance inAEO<strong>2006</strong>, the first AEO <strong>with</strong> projections out <strong>to</strong> <strong>2030</strong>.For each of the energy supply and demand sec<strong>to</strong>rsrepresented in NEMS, there are key technologiesthat, while they may not be important in the market<strong>to</strong>day, could play a role in the U.S. energy economy by<strong>2030</strong> if their cost and/or performance characteristicsimprove <strong>with</strong> successful R&D. Moreover, it is possible,if not likely, that technologies not yet conceivedcould be important 20 <strong>to</strong> 30 years from now. Althoughthe direction and pace of change are unpredictable,technological progress is certain <strong>to</strong> continue.Buildings Sec<strong>to</strong>rA variety of new technologies could influence futureenergy use in residential and commercial buildingsbeyond the levels projected in AEO<strong>2006</strong>. Two suchtechnologies are solid-state lighting and “zeroenergy” homes.Solid-state lighting. Solid-state lighting (SSL) is anemerging technology for general lighting applicationsin buildings. Two types of SSL currently under developmentare semiconduc<strong>to</strong>r-based light-emitting diode(LED) and <strong>org</strong>anic light-emitting diode (OLED) technologies.Both are commercially available for specializedlighting applications. Consumers are likely <strong>to</strong> befamiliar <strong>with</strong> the use of LEDs in traffic signals, exitsigns and similar displays, vehicle tail lights, andflashlights. They are less likely <strong>to</strong> be familiar <strong>with</strong>OLEDs, used in high-resolution display panels forcomputers and other electronic devices.Lighting accounted for 16 percent of <strong>to</strong>tal primaryenergy consumption in buildings in 2004, second only<strong>to</strong> space heating at 20 percent. Thus, changes in theassumptions made about development and enhancemen<strong>to</strong>f SSL technologies could have a significantimpact on projected <strong>to</strong>tal energy consumption in residentialand commercial buildings through <strong>2030</strong>.Beginning <strong>with</strong> AEO2005, SSL based on LED technologyhas been included as an option in the NEMSCommercial Module, based on currently availableproducts. Those products are more than four times asexpensive as comparable incandescent lighting, <strong>with</strong>only slightly greater efficiency (called “efficacy” andmeasured in lumens per watt), and so have virtuallyno impact in the AEO<strong>2006</strong> projections. In order forLEDs and OLEDs <strong>to</strong> compete successfully in generallighting applications, several R&D hurdles must beovercome: costs must be reduced, efficacy must beincreased, and improved techniques must be developedfor generating light <strong>with</strong> a high color renderingindex (CRI) that more closely approximates the spectrumof natural light and is needed for many buildingapplications.DOE’s R&D goals call for SSL costs <strong>to</strong> fall dramaticallyby <strong>2030</strong>. The real promise for LED lighting isthat efficacies could approach 150 <strong>to</strong> 200 lumens perwatt—more than twice the efficacy of current fluorescenttechnologies and roughly 10 times the efficacy ofincandescent lighting [30]. An additional goal is <strong>to</strong>increase LED operating lifetimes from 30,000 hours<strong>to</strong> 100,000 hours or more, which would far exceed theuseful lifetimes of conventional technologies (generally,between 1,000 and 20,000 hours). Longer usefuloperating lives are particularly valuable in commercialapplications where lamp replacement representsa major element of lighting costs.For general illumination applications, OLED technologylags behind LED technology. If research goals arerealized, the advantages of OLED technology will belower production costs than LEDs, similar theoreticalefficacies (200 lumens per watt for white light), andthe flexibility <strong>to</strong> serve as a source of distributed lighting,as is currently provided by fluorescent lamps.Zero energy homes. DOE’s Zero <strong>Energy</strong> Homes (ZEH)program encompasses several existing technologiesrather than a single emerging technology. The ZEHprogram takes a “whole house” approach <strong>to</strong> reducingnonrenewable energy consumption in residentialbuildings by integrating energy-efficient technologiesfor building shells and appliances <strong>with</strong> solar waterheating and PV technologies <strong>to</strong> reduce annual netconsumption of energy from nonrenewable sources <strong>to</strong>zero [31]. This is an emerging integrated technology;the ZEH concept is novel for conventional housingunits [32]. ZEH pro<strong>to</strong>types have been shown <strong>to</strong> generatemore electric energy than they consume during<strong>Energy</strong> Information Administration / <strong>Annual</strong> <strong>Energy</strong> <strong>Outlook</strong> <strong>2006</strong> 41