Annual Energy Outlook 2006 with Projections to 2030 - Usinfo.org

Annual Energy Outlook 2006 with Projections to 2030 - Usinfo.org

Annual Energy Outlook 2006 with Projections to 2030 - Usinfo.org

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

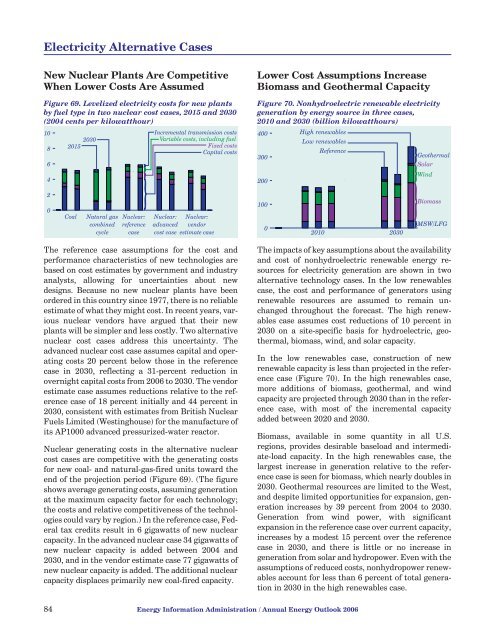

Electricity Alternative CasesNew Nuclear Plants Are CompetitiveWhen Lower Costs Are AssumedFigure 69. Levelized electricity costs for new plantsby fuel type in two nuclear cost cases, 2015 and <strong>2030</strong>(2004 cents per kilowatthour)108642015Incremental transmission costs<strong>2030</strong> Variable costs, including fuelFixed costsCapital costsLower Cost Assumptions IncreaseBiomass and Geothermal CapacityFigure 70. Nonhydroelectric renewable electricitygeneration by energy source in three cases,2010 and <strong>2030</strong> (billion kilowatthours)400 High renewablesLow renewables300200ReferenceGeothermalSolarWind20CoalNatural gascombinedcycleNuclear:referencecaseNuclear: Nuclear:advanced vendorcost case estimate case10002010 <strong>2030</strong>BiomassMSW/LFGThe reference case assumptions for the cost andperformance characteristics of new technologies arebased on cost estimates by government and industryanalysts, allowing for uncertainties about newdesigns. Because no new nuclear plants have beenordered in this country since 1977, there is no reliableestimate of what they might cost. In recent years, variousnuclear vendors have argued that their newplants will be simpler and less costly. Two alternativenuclear cost cases address this uncertainty. Theadvanced nuclear cost case assumes capital and operatingcosts 20 percent below those in the referencecase in <strong>2030</strong>, reflecting a 31-percent reduction inovernight capital costs from <strong>2006</strong> <strong>to</strong> <strong>2030</strong>. The vendorestimate case assumes reductions relative <strong>to</strong> the referencecase of 18 percent initially and 44 percent in<strong>2030</strong>, consistent <strong>with</strong> estimates from British NuclearFuels Limited (Westinghouse) for the manufacture ofits AP1000 advanced pressurized-water reac<strong>to</strong>r.Nuclear generating costs in the alternative nuclearcost cases are competitive <strong>with</strong> the generating costsfor new coal- and natural-gas-fired units <strong>to</strong>ward theend of the projection period (Figure 69). (The figureshows average generating costs, assuming generationat the maximum capacity fac<strong>to</strong>r for each technology;the costs and relative competitiveness of the technologiescould vary by region.) In the reference case, Federaltax credits result in 6 gigawatts of new nuclearcapacity. In the advanced nuclear case 34 gigawatts ofnew nuclear capacity is added between 2004 and<strong>2030</strong>, and in the vendor estimate case 77 gigawatts ofnew nuclear capacity is added. The additional nuclearcapacity displaces primarily new coal-fired capacity.The impacts of key assumptions about the availabilityand cost of nonhydroelectric renewable energy resourcesfor electricity generation are shown in twoalternative technology cases. In the low renewablescase, the cost and performance of genera<strong>to</strong>rs usingrenewable resources are assumed <strong>to</strong> remain unchangedthroughout the forecast. The high renewablescase assumes cost reductions of 10 percent in<strong>2030</strong> on a site-specific basis for hydroelectric, geothermal,biomass, wind, and solar capacity.In the low renewables case, construction of newrenewable capacity is less than projected in the referencecase (Figure 70). In the high renewables case,more additions of biomass, geothermal, and windcapacity are projected through <strong>2030</strong> than in the referencecase, <strong>with</strong> most of the incremental capacityadded between 2020 and <strong>2030</strong>.Biomass, available in some quantity in all U.S.regions, provides desirable baseload and intermediate-loadcapacity. In the high renewables case, thelargest increase in generation relative <strong>to</strong> the referencecase is seen for biomass, which nearly doubles in<strong>2030</strong>. Geothermal resources are limited <strong>to</strong> the West,and despite limited opportunities for expansion, generationincreases by 39 percent from 2004 <strong>to</strong> <strong>2030</strong>.Generation from wind power, <strong>with</strong> significantexpansion in the reference case over current capacity,increases by a modest 15 percent over the referencecase in <strong>2030</strong>, and there is little or no increase ingeneration from solar and hydropower. Even <strong>with</strong> theassumptions of reduced costs, nonhydropower renewablesaccount for less than 6 percent of <strong>to</strong>tal generationin <strong>2030</strong> in the high renewables case.84 <strong>Energy</strong> Information Administration / <strong>Annual</strong> <strong>Energy</strong> <strong>Outlook</strong> <strong>2006</strong>