Annual Energy Outlook 2006 with Projections to 2030 - Usinfo.org

Annual Energy Outlook 2006 with Projections to 2030 - Usinfo.org

Annual Energy Outlook 2006 with Projections to 2030 - Usinfo.org

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

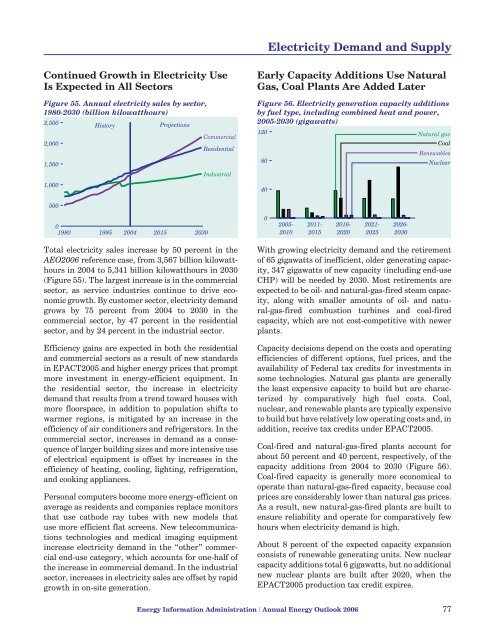

Electricity Demand and SupplyContinued Growth in Electricity UseIs Expected in All Sec<strong>to</strong>rsFigure 55. <strong>Annual</strong> electricity sales by sec<strong>to</strong>r,1980-<strong>2030</strong> (billion kilowatthours)2,5002,0001,5001,000His<strong>to</strong>ry<strong>Projections</strong>CommercialResidentialIndustrialEarly Capacity Additions Use NaturalGas, Coal Plants Are Added LaterFigure 56. Electricity generation capacity additionsby fuel type, including combined heat and power,2005-<strong>2030</strong> (gigawatts)120 Natural gasCoalRenewables80Nuclear4050001980 1995 2004 2015 <strong>2030</strong>02005-20102011-20152016-20202021-20252026-<strong>2030</strong>Total electricity sales increase by 50 percent in theAEO<strong>2006</strong> reference case, from 3,567 billion kilowatthoursin 2004 <strong>to</strong> 5,341 billion kilowatthours in <strong>2030</strong>(Figure 55). The largest increase is in the commercialsec<strong>to</strong>r, as service industries continue <strong>to</strong> drive economicgrowth. By cus<strong>to</strong>mer sec<strong>to</strong>r, electricity demandgrows by 75 percent from 2004 <strong>to</strong> <strong>2030</strong> in thecommercial sec<strong>to</strong>r, by 47 percent in the residentialsec<strong>to</strong>r, and by 24 percent in the industrial sec<strong>to</strong>r.Efficiency gains are expected in both the residentialand commercial sec<strong>to</strong>rs as a result of new standardsin EPACT2005 and higher energy prices that promptmore investment in energy-efficient equipment. Inthe residential sec<strong>to</strong>r, the increase in electricitydemand that results from a trend <strong>to</strong>ward houses <strong>with</strong>more floorspace, in addition <strong>to</strong> population shifts <strong>to</strong>warmer regions, is mitigated by an increase in theefficiency of air conditioners and refrigera<strong>to</strong>rs. In thecommercial sec<strong>to</strong>r, increases in demand as a consequenceof larger building sizes and more intensive useof electrical equipment is offset by increases in theefficiency of heating, cooling, lighting, refrigeration,and cooking appliances.Personal computers become more energy-efficient onaverage as residents and companies replace moni<strong>to</strong>rsthat use cathode ray tubes <strong>with</strong> new models thatuse more efficient flat screens. New telecommunicationstechnologies and medical imaging equipmentincrease electricity demand in the “other” commercialend-use category, which accounts for one-half ofthe increase in commercial demand. In the industrialsec<strong>to</strong>r, increases in electricity sales are offset by rapidgrowth in on-site generation.With growing electricity demand and the retiremen<strong>to</strong>f 65 gigawatts of inefficient, older generating capacity,347 gigawatts of new capacity (including end-useCHP) will be needed by <strong>2030</strong>. Most retirements areexpected <strong>to</strong> be oil- and natural-gas-fired steam capacity,along <strong>with</strong> smaller amounts of oil- and natural-gas-firedcombustion turbines and coal-firedcapacity, which are not cost-competitive <strong>with</strong> newerplants.Capacity decisions depend on the costs and operatingefficiencies of different options, fuel prices, and theavailability of Federal tax credits for investments insome technologies. Natural gas plants are generallythe least expensive capacity <strong>to</strong> build but are characterizedby comparatively high fuel costs. Coal,nuclear, and renewable plants are typically expensive<strong>to</strong> build but have relatively low operating costs and, inaddition, receive tax credits under EPACT2005.Coal-fired and natural-gas-fired plants account forabout 50 percent and 40 percent, respectively, of thecapacity additions from 2004 <strong>to</strong> <strong>2030</strong> (Figure 56).Coal-fired capacity is generally more economical <strong>to</strong>operate than natural-gas-fired capacity, because coalprices are considerably lower than natural gas prices.As a result, new natural-gas-fired plants are built <strong>to</strong>ensure reliability and operate for comparatively fewhours when electricity demand is high.About 8 percent of the expected capacity expansionconsists of renewable generating units. New nuclearcapacity additions <strong>to</strong>tal 6 gigawatts, but no additionalnew nuclear plants are built after 2020, when theEPACT2005 production tax credit expires.<strong>Energy</strong> Information Administration / <strong>Annual</strong> <strong>Energy</strong> <strong>Outlook</strong> <strong>2006</strong> 77