SEEU Review vol. 5 Nr. 2 (pdf) - South East European University

SEEU Review vol. 5 Nr. 2 (pdf) - South East European University

SEEU Review vol. 5 Nr. 2 (pdf) - South East European University

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>SEEU</strong> <strong>Review</strong> Volume 5, No. 2, 2009<br />

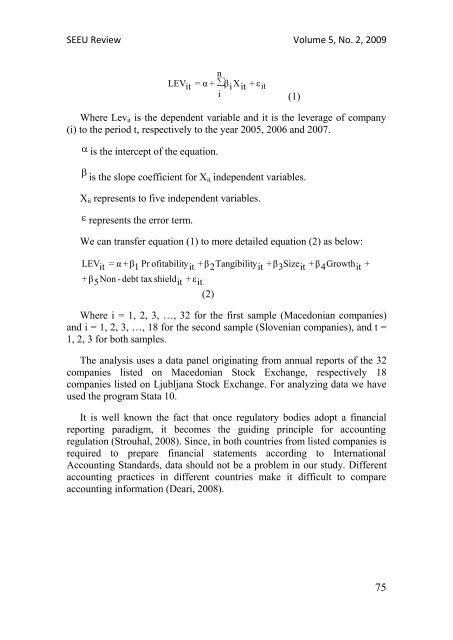

LEV it<br />

∑ n = α + β i X it + ε it<br />

i<br />

(1)<br />

Where Lev it is the dependent variable and it is the leverage of company<br />

(i) to the period t, respectively to the year 2005, 2006 and 2007.<br />

is the intercept of the equation.<br />

is the slope coefficient for Xit independent variables.<br />

X it represents to five independent variables.<br />

represents the error term.<br />

We can transfer equation (1) to more detailed equation (2) as below:<br />

LEV it = α +β 1 Pr ofitability it<br />

+ β 5 Non - debt tax shield it + ε it<br />

(2)<br />

+β 2 Tangibility it +β 3 Size it +β 4 Growth it +<br />

Where i = 1, 2, 3, …, 32 for the first sample (Macedonian companies)<br />

and i = 1, 2, 3, …, 18 for the second sample (Slovenian companies), and t =<br />

1, 2, 3 for both samples.<br />

The analysis uses a data panel originating from annual reports of the 32<br />

companies listed on Macedonian Stock Exchange, respectively 18<br />

companies listed on Ljubljana Stock Exchange. For analyzing data we have<br />

used the program Stata 10.<br />

It is well known the fact that once regulatory bodies adopt a financial<br />

reporting paradigm, it becomes the guiding principle for accounting<br />

regulation (Strouhal, 2008). Since, in both countries from listed companies is<br />

required to prepare financial statements according to International<br />

Accounting Standards, data should not be a problem in our study. Different<br />

accounting practices in different countries make it difficult to compare<br />

accounting information (Deari, 2008).<br />

75