Allowance for Loan Losses (continued)The following table details information on Citi‘s allowance for loan losses, loans and coverage ratios as of March 31, 2012:March 31, 2012In <strong>billion</strong>s of dollarsAllowance forloan lossesLoans, net ofunearned incomeAllowance as apercentage of loans (1)North America cards (2) $ 9.2 $110.8 8.3%North America residential mortgages 9.6 136.2 7.0North America other 1.5 22.3 7.1International cards 2.9 39.5 <strong>7.3</strong>International other (3) 2.7 10<strong>7.3</strong> 2.5Total Consumer $25.9 $416.1 6.2%Total Corporate $ 3.1 $231.9 1.3%Total <strong>Citigroup</strong> $29.0 $648.0 4.5%(1) Allowance as a percentage of loans excludes loans that are carried at fair value.(2) Includes both Citi-branded cards and Citi retail services.(3) Includes mortgages and other retail loans.Non-Accrual Loans and Assets, and Renegotiated LoansThe following pages include information on Citi‘s ―Non-Accrual Loans and Assets‖ and ―Renegotiated Loans.‖ There isa certain amount of overlap among these categories. Thefollowing general summary provides a basic description of eachcategory:Non-Accrual Loans and Assets:Corporate and Consumer (commercial market) non-accrualstatus is based on the determination that payment of interestor principal is doubtful.Consumer non-accrual status is based on aging, i.e., theborrower has fallen behind in payments.North America Citi-branded cards and Citi retail servicesare not included as, under industry standards, they accrueinterest until charge-off.Renegotiated Loans:Both Corporate and Consumer loans whose terms have beenmodified in a TDR.Includes both accrual and non-accrual TDRs.Non-Accrual Loans and AssetsThe table below summarizes <strong>Citigroup</strong>‘s non-accrual loans as ofthe periods indicated. Non-accrual loans are loans in which theborrower has fallen behind in interest payments or, forCorporate and Consumer (commercial market) loans, where Citihas determined that the payment of interest or principal isdoubtful and which are therefore considered impaired. Insituations where Citi reasonably expects that only a portion ofthe principal owed will ultimately be collected, all paymentsreceived are reflected as a reduction of principal and not asinterest income. There is no industry-wide definition of nonaccrualassets, however, and as such, analysis across theindustry is not always comparable.Corporate and Consumer (commercial markets) non-accrualloans may still be current on interest payments but areconsidered non-accrual as Citi has determined that the futurepayment of interest and/or principal is doubtful. Consistent withindustry convention, Citi generally accrues interest on creditcard loans until such loans are charged-off, which typicallyoccurs at 180 days contractual delinquency. As such, the nonaccrualloan disclosures in this section do not include NorthAmerica credit card loans.45CITIGROUP – 2012 FIRST QUARTER 10-Q

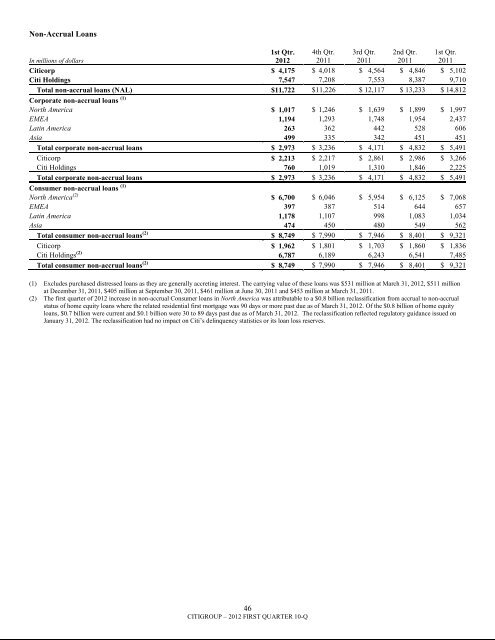

Non-Accrual LoansIn millions of dollars1st Qtr.20124th Qtr.20113rd Qtr.20112nd Qtr.20111st Qtr.2011Citicorp $ 4,175 $ 4,018 $ 4,564 $ 4,846 $ 5,102Citi Holdings 7,547 7,208 7,553 8,387 9,710Total non-accrual loans (NAL) $11,722 $11,226 $ 12,117 $ 13,233 $ 14,812Corporate non-accrual loans (1)North America $ 1,017 $ 1,246 $ 1,639 $ 1,899 $ 1,997EMEA 1,194 1,293 1,748 1,954 2,437Latin America 263 362 442 528 606Asia 499 335 342 451 451Total corporate non-accrual loans $ 2,973 $ 3,236 $ 4,171 $ 4,832 $ 5,491Citicorp $ 2,213 $ 2,217 $ 2,861 $ 2,986 $ 3,266Citi Holdings 760 1,019 1,310 1,846 2,225Total corporate non-accrual loans $ 2,973 $ 3,236 $ 4,171 $ 4,832 $ 5,491Consumer non-accrual loans (1)North America (2) $ 6,700 $ 6,046 $ 5,954 $ 6,125 $ 7,068EMEA 397 387 514 644 657Latin America 1,178 1,107 998 1,083 1,034Asia 474 450 480 549 562Total consumer non-accrual loans (2) $ 8,749 $ 7,990 $ 7,946 $ 8,401 $ 9,321Citicorp $ 1,962 $ 1,801 $ 1,703 $ 1,860 $ 1,836Citi Holdings (2) 6,787 6,189 6,243 6,541 7,485Total consumer non-accrual loans (2) $ 8,749 $ 7,990 $ 7,946 $ 8,401 $ 9,321(1) Excludes purchased distressed loans as they are generally accreting interest. The carrying value of these loans was $531 million at March 31, 2012, $511 millionat December 31, 2011, $405 million at September 30, 2011, $461 million at June 30, 2011 and $453 million at March 31, 2011.(2) The first quarter of 2012 increase in non-accrual Consumer loans in North America was attributable to a $0.8 <strong>billion</strong> reclassification from accrual to non-accrualstatus of home equity loans where the related residential first mortgage was 90 days or more past due as of March 31, 2012. Of the $0.8 <strong>billion</strong> of home equityloans, $0.7 <strong>billion</strong> were current and $0.1 <strong>billion</strong> were 30 to 89 days past due as of March 31, 2012. The reclassification reflected regulatory guidance issued onJanuary 31, 2012. The reclassification had no impact on Citi‘s delinquency statistics or its loan loss reserves.46CITIGROUP – 2012 FIRST QUARTER 10-Q