chapter viii wool & wollen textiles industry - Ministry of Textiles

chapter viii wool & wollen textiles industry - Ministry of Textiles

chapter viii wool & wollen textiles industry - Ministry of Textiles

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

ministry <strong>of</strong> <strong>textiles</strong><br />

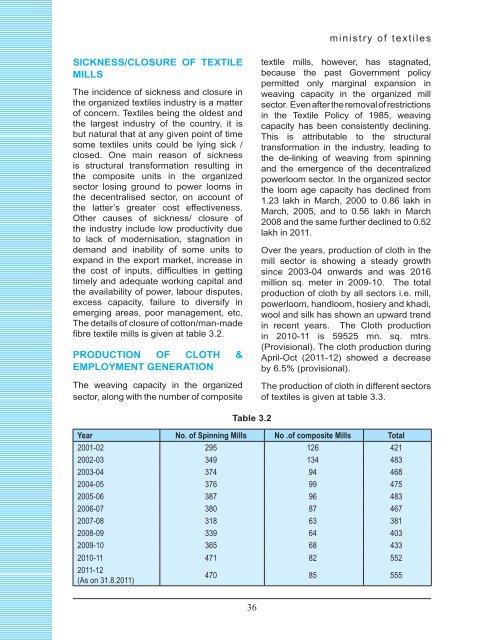

SICKNESS/CLOSURE OF TEXTILE<br />

MILLS<br />

The incidence <strong>of</strong> sickness and closure in<br />

the organized <strong>textiles</strong> <strong>industry</strong> is a matter<br />

<strong>of</strong> concern. <strong>Textiles</strong> being the oldest and<br />

the largest <strong>industry</strong> <strong>of</strong> the country, it is<br />

but natural that at any given point <strong>of</strong> time<br />

some <strong>textiles</strong> units could be lying sick /<br />

closed. One main reason <strong>of</strong> sickness<br />

is structural transformation resulting in<br />

the composite units in the organized<br />

sector losing ground to power looms in<br />

the decentralised sector, on account <strong>of</strong><br />

the latter’s greater cost effectiveness.<br />

Other causes <strong>of</strong> sickness/ closure <strong>of</strong><br />

the <strong>industry</strong> include low productivity due<br />

to lack <strong>of</strong> modernisation, stagnation in<br />

demand and inability <strong>of</strong> some units to<br />

expand in the export market, increase in<br />

the cost <strong>of</strong> inputs, difficulties in getting<br />

timely and adequate working capital and<br />

the availability <strong>of</strong> power, labour disputes,<br />

excess capacity, failure to diversify in<br />

emerging areas, poor management, etc.<br />

The details <strong>of</strong> closure <strong>of</strong> cotton/man-made<br />

fibre textile mills is given at table 3.2.<br />

PRODUCTION OF CLOTH &<br />

EMPLOYMENT GENERATION<br />

The weaving capacity in the organized<br />

sector, along with the number <strong>of</strong> composite<br />

textile mills, however, has stagnated,<br />

because the past Government policy<br />

permitted only marginal expansion in<br />

weaving capacity in the organized mill<br />

sector. Even after the removal <strong>of</strong> restrictions<br />

in the Textile Policy <strong>of</strong> 1985, weaving<br />

capacity has been consistently declining.<br />

This is attributable to the structural<br />

transformation in the <strong>industry</strong>, leading to<br />

the de-linking <strong>of</strong> weaving from spinning<br />

and the emergence <strong>of</strong> the decentralized<br />

powerloom sector. In the organized sector<br />

the loom age capacity has declined from<br />

1.23 lakh in March, 2000 to 0.86 lakh in<br />

March, 2005, and to 0.56 lakh in March<br />

2008 and the same further declined to 0.52<br />

lakh in 2011.<br />

Over the years, production <strong>of</strong> cloth in the<br />

mill sector is showing a steady growth<br />

since 2003-04 onwards and was 2016<br />

million sq. meter in 2009-10. The total<br />

production <strong>of</strong> cloth by all sectors i.e. mill,<br />

powerloom, handloom, hosiery and khadi,<br />

<strong>wool</strong> and silk has shown an upward trend<br />

in recent years. The Cloth production<br />

in 2010-11 is 59525 mn. sq. mtrs.<br />

(Provisional). The cloth production during<br />

April-Oct (2011-12) showed a decrease<br />

by 6.5% (provisional).<br />

The production <strong>of</strong> cloth in different sectors<br />

<strong>of</strong> <strong>textiles</strong> is given at table 3.3.<br />

Table 3.2<br />

Year No. <strong>of</strong> Spinning Mills No .<strong>of</strong> composite Mills Total<br />

2001-02 295 126 421<br />

2002-03 349 134 483<br />

2003-04 374 94 468<br />

2004-05 376 99 475<br />

2005-06 387 96 483<br />

2006-07 380 87 467<br />

2007-08 318 63 381<br />

2008-09 339 64 403<br />

2009-10 365 68 433<br />

2010-11 471 82 552<br />

2011-12<br />

(As on 31.8.2011)<br />

470 85 555<br />

36