Review of 2010 â USD version - Skanska

Review of 2010 â USD version - Skanska

Review of 2010 â USD version - Skanska

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

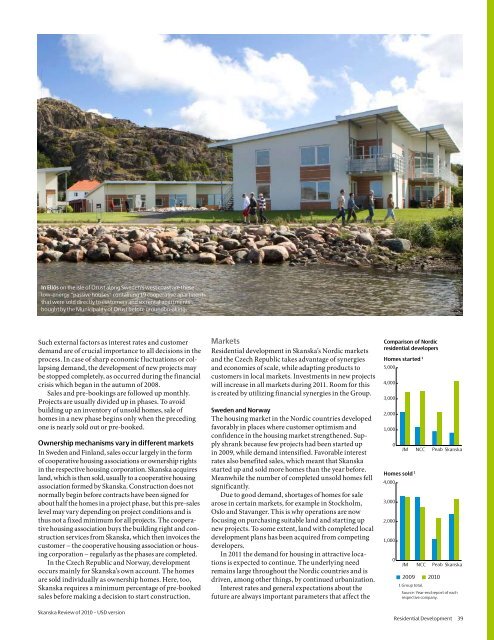

In Ellös on the isle <strong>of</strong> Orust along Sweden’s west coast are these<br />

low-energy “passive houses” containing 19 cooperative apartments<br />

that were sold directly to customers and six rental apartments<br />

bought by the Municipality <strong>of</strong> Orust before groundbreaking.<br />

Such external factors as interest rates and customer<br />

demand are <strong>of</strong> crucial importance to all decisions in the<br />

process. In case <strong>of</strong> sharp economic fluctuations or collapsing<br />

demand, the development <strong>of</strong> new projects may<br />

be stopped completely, as occurred during the financial<br />

crisis which began in the autumn <strong>of</strong> 2008.<br />

Sales and pre-bookings are followed up monthly.<br />

Projects are usually divided up in phases. To avoid<br />

building up an inventory <strong>of</strong> unsold homes, sale <strong>of</strong><br />

homes in a new phase begins only when the preceding<br />

one is nearly sold out or pre-booked.<br />

Ownership mechanisms vary in different markets<br />

In Sweden and Finland, sales occur largely in the form<br />

<strong>of</strong> cooperative housing associations or ownership rights<br />

in the respective housing corporation. <strong>Skanska</strong> acquires<br />

land, which is then sold, usually to a cooperative housing<br />

association formed by <strong>Skanska</strong>. Construction does not<br />

normally begin before contracts have been signed for<br />

about half the homes in a project phase, but this pre-sales<br />

level may vary depending on project conditions and is<br />

thus not a fixed minimum for all projects. The cooperative<br />

housing association buys the building right and construction<br />

services from <strong>Skanska</strong>, which then invoices the<br />

customer − the cooperative housing association or housing<br />

corporation − regularly as the phases are completed.<br />

In the Czech Republic and Norway, development<br />

occurs mainly for <strong>Skanska</strong>’s own account. The homes<br />

are sold individually as ownership homes. Here, too,<br />

<strong>Skanska</strong> requires a minimum percentage <strong>of</strong> pre-booked<br />

sales before making a decision to start construction.<br />

<strong>Skanska</strong> <strong>Review</strong> <strong>of</strong> <strong>2010</strong> – <strong>USD</strong> <strong>version</strong><br />

Markets Jämförelse nordiska bostadsutvecklare<br />

development in <strong>Skanska</strong>’s Nordic markets<br />

Residential<br />

and Startade the Czech bostäder Republic 1) takes advantage <strong>of</strong> synergies<br />

and 5 economies 000 <strong>of</strong> scale, while adapting products to<br />

customers in local markets. Investments in new projects<br />

4 000<br />

will increase in all markets during 2011. Room for this<br />

is created by utilizing financial synergies in the Group.<br />

3 000<br />

Sweden and Norway<br />

2 000<br />

The housing market in the Nordic countries developed<br />

favorably 1 000 in places where customer optimism and<br />

confidence in the housing market strengthened. Supply<br />

shrank 0 because few projects had been started up<br />

JM NCC Peab <strong>Skanska</strong><br />

in 2009, while demand intensified. Favorable interest<br />

rates Sålda also bostäder benefited sales, which meant that <strong>Skanska</strong><br />

1)<br />

started up and sold more homes than the year before.<br />

4 000<br />

Meanwhile the number <strong>of</strong> completed unsold homes fell<br />

significantly.<br />

3 000<br />

Due to good demand, shortages <strong>of</strong> homes for sale<br />

arose in certain markets, for example in Stockholm,<br />

Oslo 2 and 000 Stavanger. This is why operations are now<br />

focusing on purchasing suitable land and starting up<br />

new 1 projects. 000 To some extent, land with completed local<br />

development plans has been acquired from competing<br />

developers.<br />

0<br />

In 2011 JMthe demand NCC Peabfor <strong>Skanska</strong> housing in attractive locations<br />

is expected to continue. The underlying need<br />

remains large throughout the Nordic countries and is<br />

1) Totalt i respektive koncern.<br />

driven, among other things, by continued urbanization.<br />

Källa: Respektive bolags<br />

Interest Bokslutskommuniké.<br />

rates and general expectations about the<br />

future are always important parameters that affect the<br />

Comparison <strong>of</strong> Nordic<br />

residential developers<br />

Homes started 1<br />

5,000<br />

4,000<br />

3,000<br />

2,000<br />

1,000<br />

• 2009 • <strong>2010</strong> • 2009 • <strong>2010</strong><br />

0<br />

Homes sold 1<br />

4,000<br />

3,000<br />

2,000<br />

1,000<br />

0<br />

JM NCC Peab <strong>Skanska</strong><br />

JM NCC Peab <strong>Skanska</strong><br />

1 Group total.<br />

Source: Year-end report <strong>of</strong> each<br />

respective company.<br />

Residential Development 39