Review of 2010 â USD version - Skanska

Review of 2010 â USD version - Skanska

Review of 2010 â USD version - Skanska

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Business streams<br />

Appraisal methodology<br />

<strong>Skanska</strong> conducts an annual market appraisal <strong>of</strong> its project<br />

portfolio. Estimated future cash flows are discounted<br />

at an interest rate equivalent to a yield requirement on<br />

equity. The level <strong>of</strong> this requirement is based on country<br />

risk, risk model and project phase for the various projects.<br />

The appraisal is not primarily intended to establish a<br />

specific value for the investments in the project portfolio,<br />

but above all to use a consistent methodology to provide<br />

an indication <strong>of</strong> movements in underlying values, while<br />

clarifying the impact <strong>of</strong> the transactions carried out during<br />

the period. The appraisal covers 15 projects that have<br />

reached financial close and have thus been started up.<br />

The <strong>2010</strong> appraisal<br />

At year-end <strong>2010</strong>, the estimated gross present value<br />

<strong>of</strong> cash flows from projects, excluding the Autopista<br />

Central highway, totaled <strong>USD</strong> 0.7 (1.6) billion. Unrealized<br />

development gains before taxes amounted to about<br />

<strong>USD</strong> 258 M (1.2 bn) at year-end. During <strong>2010</strong> the figure<br />

was reduced mainly due to the divestment <strong>of</strong> <strong>Skanska</strong>’s<br />

stake in the concession for the Autopista Central,<br />

which is expected to generate an after-tax gain <strong>of</strong> about<br />

<strong>USD</strong> 0.73 billion. The weighted discount rate used in the<br />

appraisal was 10.4 (11.0) percent.<br />

The appraisal carried out at the end <strong>of</strong> <strong>2010</strong> encompassed<br />

an update <strong>of</strong> financial models and a review <strong>of</strong> the<br />

yield requirements applied. The assessment <strong>of</strong> market<br />

value was made in cooperation with external appraisal<br />

expertise.<br />

Earnings<br />

Revenue in <strong>Skanska</strong> Infrastructure comes mainly from<br />

<strong>Skanska</strong>’s share <strong>of</strong> income in the companies that own<br />

assets in project portfolios and from divestments <strong>of</strong><br />

these companies. Expenses consist mainly <strong>of</strong> bidding<br />

costs and the cost <strong>of</strong> <strong>Skanska</strong>’s own employees.<br />

Starting from <strong>2010</strong>, <strong>Skanska</strong> is applying IFRIC 12,<br />

which means that earnings in project companies are<br />

accounted for in relation to value <strong>of</strong> services provided.<br />

This will result in earlier and higher income from participations<br />

in consortia as well as lower unrealized development<br />

gain.<br />

Its business model is based on investing in projects<br />

that increase in value upon being completed, thereby<br />

enabling <strong>Skanska</strong> to sell them to investors that have<br />

lower return requirements.<br />

<strong>Skanska</strong> intends to expand its operations in the public-private<br />

partnership sector. The Company prioritizes<br />

projects with reasonable returns that meet the Group’s<br />

yield requirements.<br />

For some time, the United Kingdom has been the<br />

biggest market for PPP solutions but is now affected by<br />

cutbacks in the British government budget. However,<br />

opportunities are expected in the fields <strong>of</strong> street lighting<br />

networks and waste-to-energy facilities. <strong>Skanska</strong> is<br />

working on project opportunities in the latter segment,<br />

which is expected to grow as a consequence <strong>of</strong> EU legislation<br />

that will not permit waste landfills.<br />

In Sweden, opportunities are expected to increase,<br />

for example in the construction <strong>of</strong> wind power facilities.<br />

North America continues to <strong>of</strong>fer attractive expansion<br />

potential, but the market is developing slowly.<br />

A number <strong>of</strong> U.S. states are planning public-private<br />

partnerships related to road projects, but the timetable<br />

remains uncertain.<br />

In Latin America, there is a large potential PPP market<br />

for hospital projects. New hospital projects are expected<br />

to be put out for tender competitions during 2011.<br />

In the Czech Republic and Poland, a future market<br />

for PPP solutions is expected mainly when it comes to<br />

new highway projects and waste to energy power plants.<br />

The strained public budget situation in many countries<br />

is adversely affecting the supply <strong>of</strong> new projects.<br />

In the U.K., for example, the large-scale program for<br />

constructing new, modern schools − Building Schools<br />

for the Future − may be slowed down or cut back. Meanwhile<br />

the more stable financial market situation means<br />

that the prerequisites for new PPP projects will improve.<br />

At 188 km (117 mi.) , London’s M25<br />

orbital motorway is one <strong>of</strong> the<br />

longest ring roads in the world.<br />

Widening is currently under way<br />

on two sections in the northeast<br />

and northwest, and extra lanes<br />

totaling 58 km (36 mi.) will be<br />

added. Road-widening activities,<br />

which began in 2009, are expected<br />

to be completed before the<br />

opening <strong>of</strong> the London Games<br />

in summer 2012. <strong>Skanska</strong>’s assignment<br />

includes operation and<br />

maintenance <strong>of</strong> a total <strong>of</strong> 400 km<br />

(250 mi.) <strong>of</strong> road links.<br />

Markets<br />

Operations focus on three segments – highways, social<br />

infrastructure and such facilities as bridges, tunnels and<br />

power generation stations. <strong>Skanska</strong> is involved in the<br />

entire value chain from project design to operation and<br />

maintenance, which implies a gradual reduction in the<br />

risk level <strong>of</strong> projects.<br />

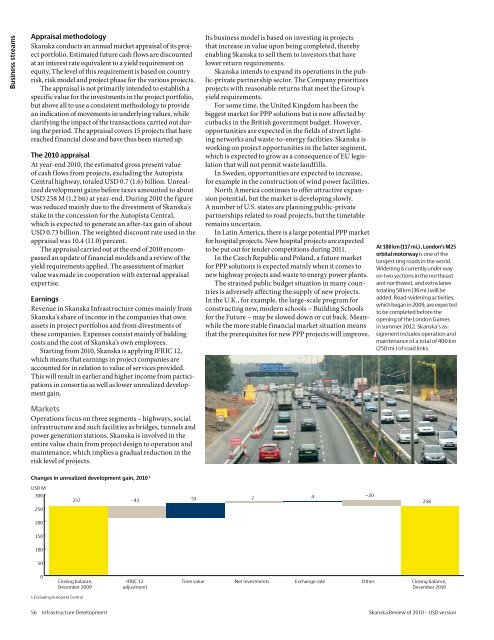

Changes in unrealized development gain, <strong>2010</strong> 1<br />

<strong>USD</strong> M<br />

300<br />

250<br />

4 −20<br />

257 –43 53 7<br />

258<br />

200<br />

150<br />

100<br />

50<br />

0<br />

Closing balance,<br />

December 2009<br />

IFRIC 12<br />

adjustment<br />

Time value Net investments<br />

Exchange rate Other Closing balance,<br />

December <strong>2010</strong><br />

1 Excluding Autopista Central<br />

56 Infrastructure Development <strong>Skanska</strong> <strong>Review</strong> <strong>of</strong> <strong>2010</strong> – <strong>USD</strong> <strong>version</strong>